Reduced IMFL prices in Karnatka helped the company to grow the volumes by 25% in the state.

4 Likes

If they take imperial blue…it will be a gamechanger…6k company doing a 5k cr acquistion…pe rerating can happen soon.

4 Likes

Feel like TI trying to bite more than it can chew. Given the over dependency on brandy segment and issue with brand ownership, they need diversification. But $600 million seems to be too big for its size.

Anyhow nothing is confirmed officially till now.

3 Likes

Agree and with earlier history of defaulting loans and company has just came out of loan resettlement issues . Apart from that management bandwidth is poor . Dhanukar family are known for mistreating their vendors and employees , holding on their final payments .Professional employees are scared to join them and TIL is not the first choice for employees /

2 Likes

News on tilaknagar plans to acquire imperial blue..

1 Like

This is old news published on 19th july, and latest news is they have difficulties in sourcing fund.

do you have any update on these lines sir?

2 Likes

Now i believe Suntory is leading race to acquire IB .Suntory has been trying to increase their presence through Oaksmith but they have achieved limited success and acquiring Imperial blue will suit their portfolio in India and they have deep pockets

2 Likes

Latest development

https://www.moneycontrol.com/news/business/tilaknagar-industries-enters-into-exclusive-talks-for-acquisition-of-pernod-ricard-s-imperial-blue-whiskey-13238629.html

2 Likes

5 Likes

Some risks highlighted in this Businessline article.

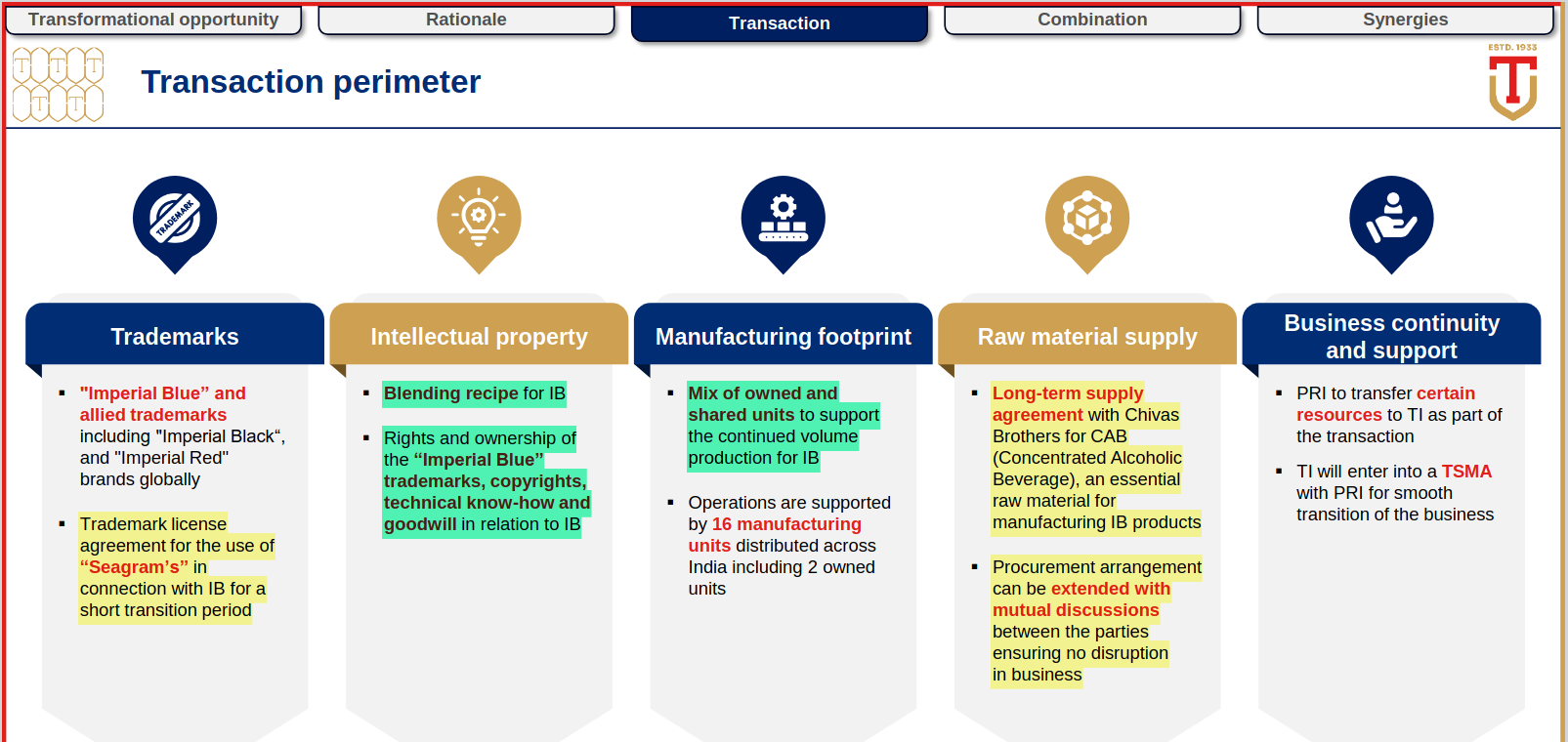

- IB’s revenue stayed around 3000Cr in the last 3 years indicating the PRs focus on premium products or pricing pressure in the mass whisky market

- Brand Identity - IB whisky is popularly known as “Seagrams Imperial Blue”. PRs license to use “Seagram’s” is only for short period of time and TI needs to reestablish without “Seagream’s” indentity

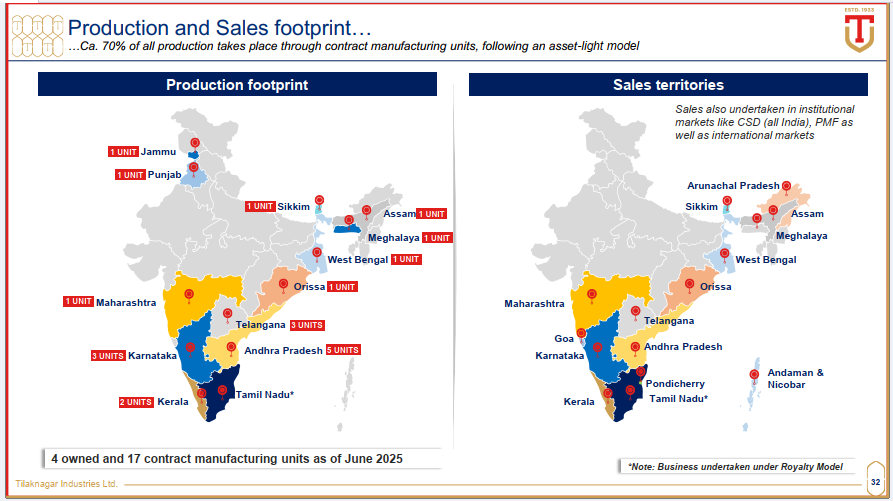

- Integration risk - TI need to integrate 16 units - of which 2 are owned

- Raw material dependency - on Chivas Brothers

Same is highlighted in the presentation.

Disc: Invested and no transaction in last 6 months.

8 Likes

Tilaknagar Industries Increases Stake in Spaceman Spirits Lab (Samsara Gin Maker) – Now Holds 21.36%

Tilaknagar Industries (TI) has made a follow-on investment of ₹10.66 crore in Spaceman Spirits Lab Pvt Ltd (SSL), the maker of premium craft spirits including Samsara Gin, Sitara Rum, and Amara Vodka.

Out of this, ₹9.15 crore was part of a previously agreed ₹13.15 crore investment announced in Sep 2024. An additional ₹1.51 crore was used to buy shares from early shareholders. As a result, TI’s stake has risen from 12.98% to 21.36% (fully diluted basis).

![]() Key Points:

Key Points:

**Strategic Bet on Premium Craft Spirits: TI seems bullish on the premiumization trend in the alco-bev space.

Future Option for Higher Stake: The agreement allows TI to increase its stake further, depending on SSL meeting certain milestones.

Synergy through Distribution: Business under the Usership Agreement between TI and SSL started in May 2025. TI will leverage its wide distribution network to sell SSL products across select Indian states and globally.

Growth Outlook for SSL: The company is targeting ~70% revenue growth and ~60% volume growth in FY26 and is expanding into whisky, heritage liqueurs, and tequila.

This development strengthens TI’s premium product portfolio and opens new long-term value creation possibilities. A company with legacy brand strength making serious moves in the new-age alco-bev segment

1f7ce971-af29-40e5-9b6b-7edf7a7f9248.pdf (545.8 KB)

6165fa0b-6e98-4123-922a-1d930aaf3fe3.pdf (640.6 KB)

5 Likes

Amazing ![]() Results By TILAKNAGAR INDUSTRIES

Results By TILAKNAGAR INDUSTRIES

Tilaknagar Industries Q1 FY26 Results Summary

Tilaknagar Industries Limited

-

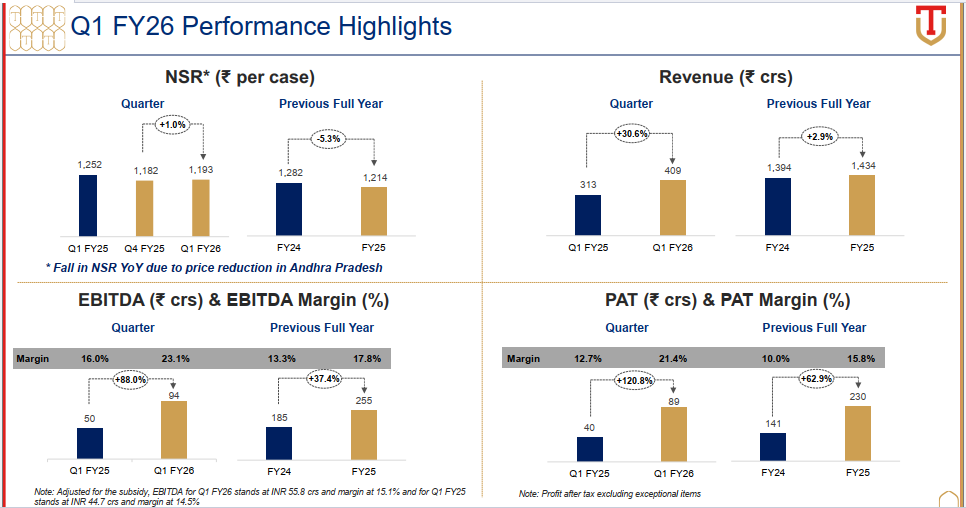

Net Profit: Consolidated net profit surged by 121.25% year-on-year (YoY) to ₹88.5 crore, compared to ₹40 crore in Q1 FY25, driven by robust revenue and improved operational efficiency.

-

Revenue: Net revenue from operations increased by 30.6% YoY to ₹409 crore, up from ₹313 crore in the same quarter last year. Excluding subsidies, revenue growth was 20.5% YoY. Total income was ₹863.87 crore, reflecting a 29.9% YoY increase but a slight 2% quarter-on-quarter (QoQ) decline.

-

EBITDA: The company achieved its highest-ever quarterly EBITDA at ₹94.5 crore, an 88% YoY increase from ₹50 crore in Q1 FY25. The EBITDA margin expanded by 700 basis points to 23.1% from 16% in the prior year, driven by cost optimization and a growing share of premium products. Excluding subsidies, the EBITDA margin was 15.1%, up 60 basis points.

-

Volume Growth: Sales volume grew by 26.5% YoY to 32.1 lakh cases, reflecting strong demand for its alcoholic beverage portfolio, particularly its flagship brandy brands.

-

Earnings Per Share (EPS): EPS for the quarter stood at ₹4.57, compared to ₹2.08 in Q1 FY25, reflecting significant profitability growth.

-

Strategic Developments:

- Capacity Expansion: The board approved a ₹25 crore capital expenditure for its wholly-owned subsidiary, Prag Distillery, to increase bottling capacity from 6 lakh cases per annum to 36 lakh cases per annum. The expansion, aimed at meeting growing demand in Andhra Pradesh, is expected to be completed within 12 months and will be funded through financial assistance from the holding company.

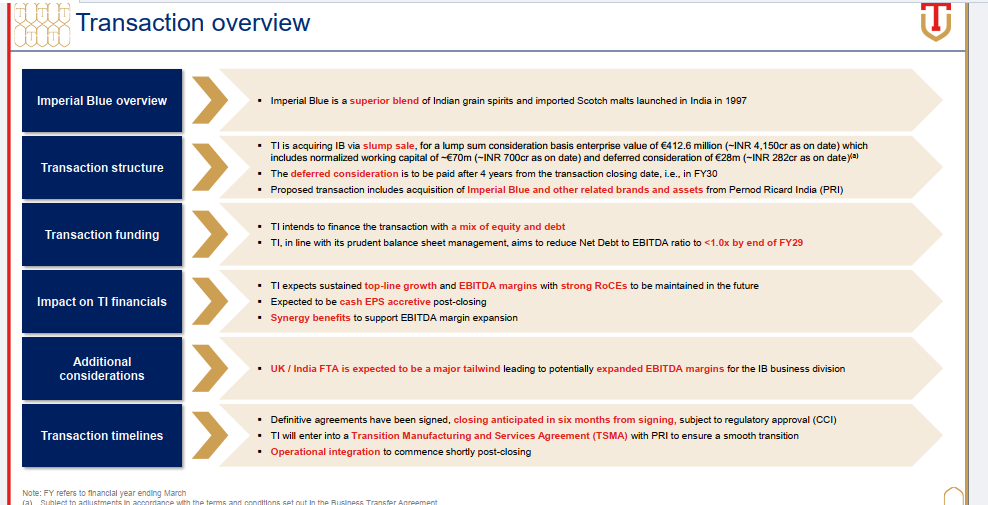

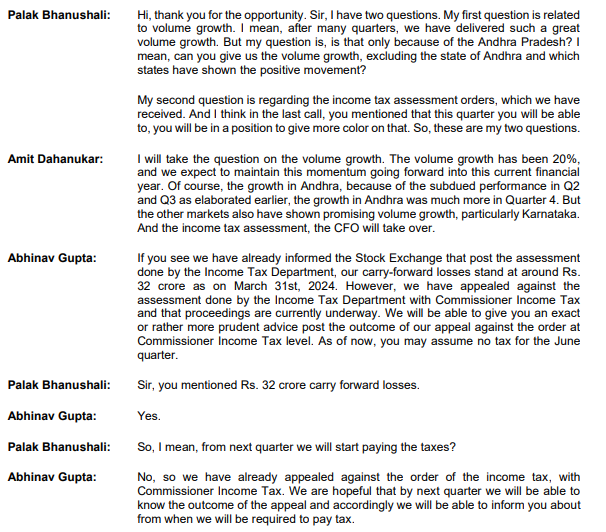

- Acquisition: The company is reportedly a front-runner to acquire the Imperial Blue brand for approximately ₹4,150 crore, which could further strengthen its market position.

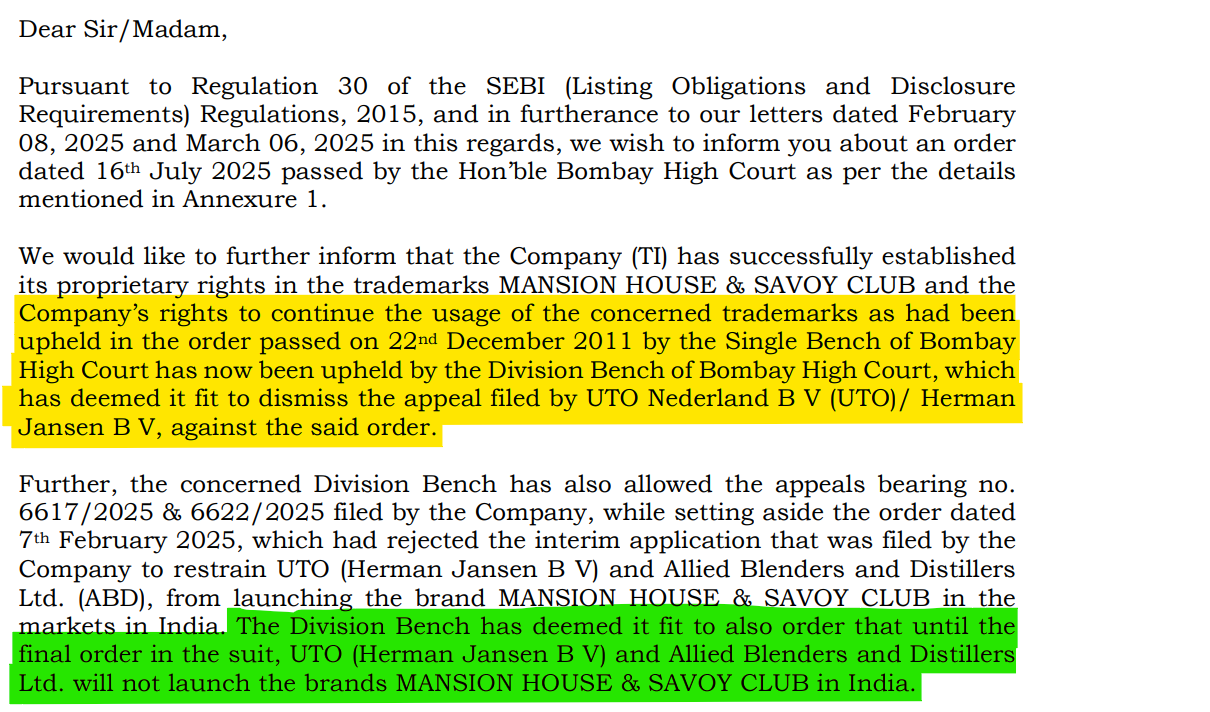

- Legal Resolution: A legal matter related to its brands was resolved, providing operational clarity.

4cc43f4e-0c98-4522-8bc5-d9ee17421cbf.pdf (2.6 MB)

No Recommendation Buy/Sell

Open for other’s opinions

4 Likes

But the financials include 38 crores in subsidy.

Thanks for highlighting that.

Even after removing the subsidy effect, Tilaknagar still shows strong double-digit growth in revenue and volumes, plus margin expansion due to higher premium product share. However, the subsidy does boost profitability this quarter

1 Like

And he is also not paying tax.

Highlights From Investor Presentation

Management on Results

Performance, Balance Sheet and Acquisition

Results

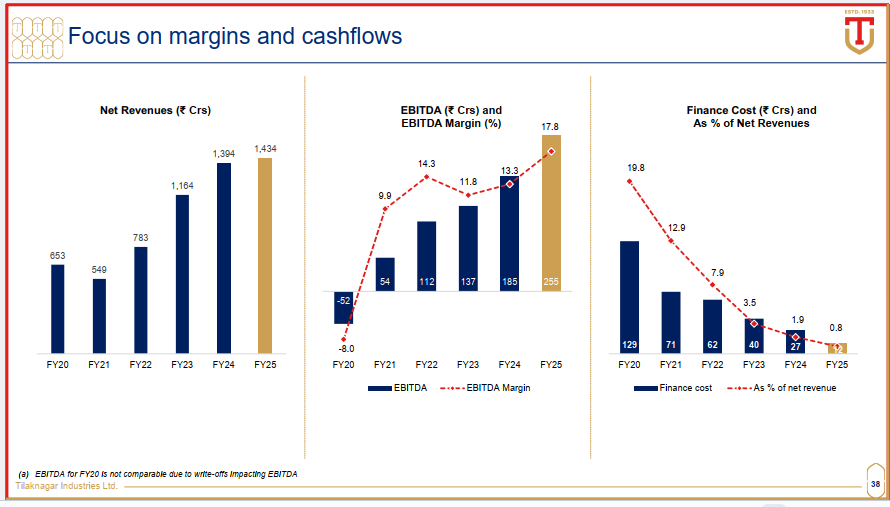

Margins Are Improving

Imperial Blue Acq.

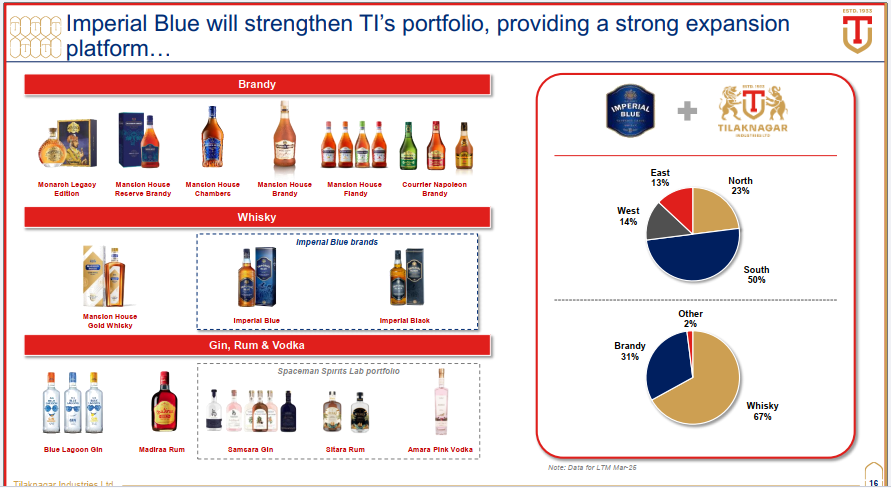

Brand Portfolio

Transformation

Growing Products

Production And Sales

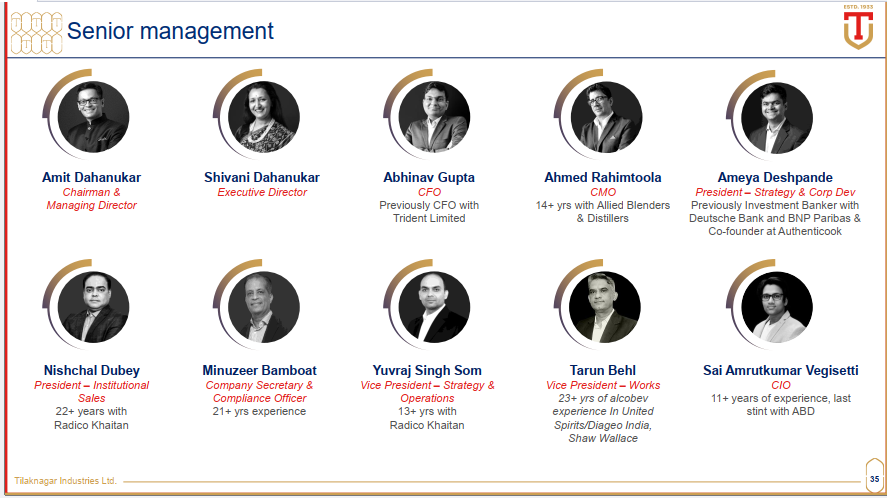

Management

Source: Q1 FY26 Investor Presentation by Tilaknagar Industries.

Key highlights and visuals as shared by the management.

Waiting For Other’s Opinion

Exactly from next qtr no tax benefits.