There margins could improve on account of premiumization and category creation!

2 Likes

Q1FY25 - Transcript - Good to see company reducing the debt. Company has paid 22.3Cr in Q1FY25 and prepaid 20 Cr of Kotak term loan in Q2 (current running quarter) due to strong cash flows. I hope the management spends the future cash flows,

- increase the dividend

- Distribution, Advertising and Marketing

- Enter to new geographies

- New product launches in adjacent verticals.

Disc: Invested. No transaction in the last 6 months.

4 Likes

Can someone help me understand why company PL shows not taxes despite making profit?

They are setting off the losses that happened in previous years. This benefit will go away from FY26 onwards.

cc: @Sridharj

3 Likes

Thesis:

Andhra Pradesh and Tamilnadu expected to reduce excise duty and create more conducive policy for alcohol sector. This could boost volumes by 20+%.

More focus on premiumization, resulting in increased margin

Company has reduced debt drastically and will be debt free by Q2FY25. All profits will become cash flow and help company expand distribution network, marketing reach with the cash in hand.

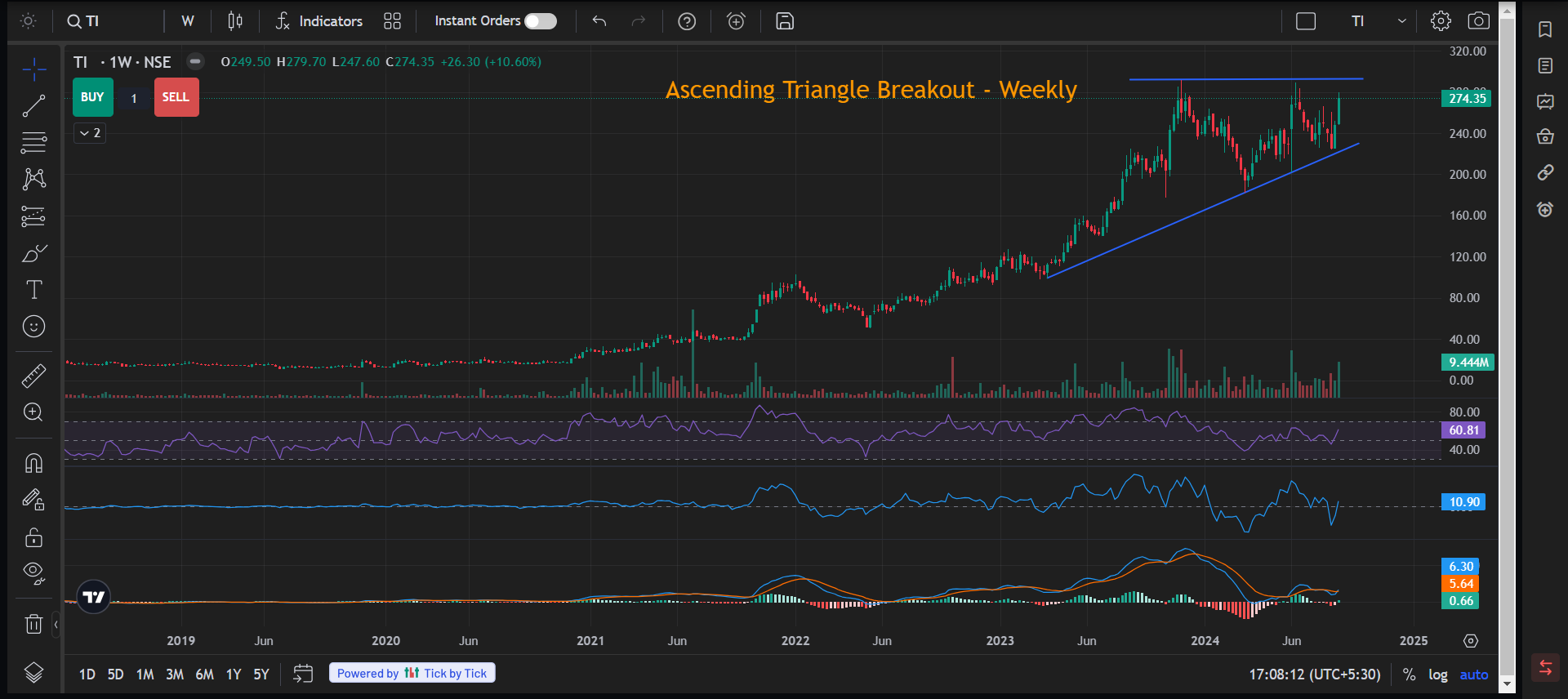

Technically about to break ATH with long 18 month consolidation.

3 Likes

Management seems to be confident on double digit growth in FY25.

Disc: Invested. No transactions in last 1 year.

cc: @Sridharj

5 Likes

Good news in recent times for Tilaknagar Industries due to future increase in FCF

-

Co. has approved an investment of Rs. 8.03 Crores in Round the Cocktails Private Limited (“Bartisans”), acquiring 36.17% of the share capital. Bartisans specializes in non-alcoholic cocktail. This company was featured on Shark Tank season-3.

-

Tilaknagar Industries has increased its stake in Spaceman Spirits Lab, producer of Samsara Gin.

-

Andhra Cabinet approves new excise policy. Company says they will have double digit volume growth on account of this policy.

5 Likes

Andhra Pradesh cabinet come with new policy, which will allow private sector to open 3396 retail shops through e auction. Shops will be operational from October 12. It was one important monitorable for Tilaknagar Industries.

D: Invested

1 Like

3 Likes

Q2 FY2025 Concall Highlights

Financial performance:

![]() Achieved highest ever quarterly EBITDA in Q2 at Rs. 66 crs, YoY growth of 39.1%

Achieved highest ever quarterly EBITDA in Q2 at Rs. 66 crs, YoY growth of 39.1%

![]() EBITDA margin at 17.6%, 422 bps expansion YoY. Industrial Promotion Incentive by Maharashtra, Q1 was 5.56 cr, Q2 was 10.36 cr. Margin Expansion mainly due to cost optimization, premiumization not impacted improvement.

EBITDA margin at 17.6%, 422 bps expansion YoY. Industrial Promotion Incentive by Maharashtra, Q1 was 5.56 cr, Q2 was 10.36 cr. Margin Expansion mainly due to cost optimization, premiumization not impacted improvement.

![]() Profit after tax at Rs. 58 crs, YoY growth of 82%; driven by reduction in finance costs

Profit after tax at Rs. 58 crs, YoY growth of 82%; driven by reduction in finance costs

![]() Net debt free as of September 2024, with net cash Rs. 25 crs.

Net debt free as of September 2024, with net cash Rs. 25 crs.

Guidance:

12 to 15% volume guidance on steady state basis.

Andhra Pradesh

AP has significant brandy drinking population.

Degrowth due to policy change.

Expect volume to grow significantly, as TI is leading player in state. 30 lakh cases industry, can be in 2 to 3 years, it can be 40 lakh cases.

AP is currently 30% of sales.

Retail going private makes market consumer driven. It benefits TI as company have good franchise. Industry will increase and company will take bigger pie. 10% shops will increase. Private players will make sure they are stocked, customers are satisfied etc. Expect overall improvement that will help to grow.

Telangana:

Overdue position is now 10 weeks. Normal is 8 to 9 weeks. Highest was 18 to 19 weeks.

IMFL Pricing committee will soon decide pricing.

Total receivable is 130 cr. Overdue is 80 cr.

Karnataka

Reduce duty, increase in volume. MRP goes down have impact positive impact.

Assam & North East:

Assam is very receptive to new product that is why Mansion House Whisky is launched in Assam. It is semi premium segment, comparable brands Royal Stage, Royal Challenge. It is priced at 560 rs. For 750ml bottle. Assam is having large market for this segment.

Upfront investment, working capital is lower compared to others.

Others:

Luxury foray is few week away. It will have incremental margin expansion, which we are not guiding as of now. One more launch after 6 months.

Easing of raw material and packaging cost.

Expect further expansion of margin.

Green Apple Flandy have very good response. It will not be millionaire brand this year. Flavoured spirts is fastest growing category in IMFL.

Tax can be back from Q1 FY2026.

Brandy is more than 90% of sales. Visio is to have 20% from Non Brandy by 2030.

CAPEX:

Maintenance CAPEX of 15 to 20 cr/year.

Distillery CAPEX not yet decided, recommission 100KLPD plant, which will cost 45 cr. If new distillery build it may cost 100 to 120 cr.

Strategic Investments:

Spaceman Spirits Lab Pvt. Ltd., the makers of ‘Samsara Gin’ and ‘Sitara Rum’.

Will start selling their brand in select state and internationally.

FY 2024 Revenue only 20 cr. It can be 100% for next two years.

TI will manufacture and sell in agreed state, where revenue and cost will come to TI books and will pay royalty to Spaceman spirits.

Samsara Gin and Sitara Gin goes along with TI’s luxury brand gives opportunity as alcoholic beverages is distribution driven market.

Round the Cocktails Pvt. Ltd., the makers of ‘Bartisans’, a ‘Ready to Pour’ cocktail mixers brand.

High brand recall, strong unit economics. Company is in non-alcoholic beverages.

80% sale online, they are digital fist company.

Expect significant growth.

It has no restriction on marketing due to non-alcoholic beverages.

There will be collaboration between Bartisans and Tilaknagar Industries.

Incredible spirits: It was small investment at 1cr. Sell this stake at cost in October.

Investor Presentation:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0f22af78-57a7-40d1-8c67-f926584c0c9c.pdf

Disclosure: Invested

4 Likes

Tilaknagar Industries showing strength in this weak market. High relative strength (RS) will lead to momentum whenever market sentiment changes.

To learn more about Tilaknagar Industries - SOIC video from 15:42

1 Like

Good report on liquor industry:

5 Likes

good comparison amongst the industry players and Tilaknagar Indusries EBIDTA margins appear to be better compared with others in the list.

2 Likes

As said in the last concall, a premium brandy product is launched.

One more product to be launched in the next 6 months ![]()

Management commentary:

5 Likes

Interesting insights

They increased their revenue guidance!!

With 1600-1700 crore revenue in this FY, they can easily clock 200 crore PAT while maintaining 15% EBITA margin. Also, they have export orders for the premium brandy that was launched.

Do you have any information regarding the performance of recently launched whiskey in Assam?

3 Likes

I dont have any info. I feel its too early to evaluate newly launched products… at least directionally company is doing all the right things.

While calculating the future EPS of the company, one should keep in mind that company had accumulated losses due to which it was not paying any taxes, but from FY26 onwards they will be paying taxes so deduct those 25% EBT.

6 Likes

The company is well-poised to grow from here with the guidance for mid-teens volume growth in H2 and even higher revenue growth. Also the margin expansion is likely to continue with focus on premiumization. Lastly, AP market has finally opened for business with the change of govt.

But can somebody share thoughts on their PE Rerating. Historically, the company has traded at a median PE of 35-40x but I see the market leaders such as United Spirits trading at a much higher valuation. Is it because of their revenue concentration in Brandy’s or some other reason?

2 Likes