PharmEasy’s parent API Holdings announces acquisition of a 66.1% stake in Thyrocare for 4,546 crore.

This currently values the company at ~6875 crore and will likely trigger an open offer, once the regulatory and competition approvals are in place

PharmEasy’s parent API Holdings announces acquisition of a 66.1% stake in Thyrocare for 4,546 crore.

This currently values the company at ~6875 crore and will likely trigger an open offer, once the regulatory and competition approvals are in place

Mind elaborating the following given the current market cap is 7,662 Cr.

will likely trigger an open offer

In India, an open offer is generally activated when an entity acquires a listed company by at least up to 15% shares. In such cases, the existing stakeholders will be given an open offer to purchase an additional 20% of the company shares.

Existing shareholders of the acquired company are also given the benefit of an exit option, in case they expect potential risks due to change in the management and business.

Source: cleartax

The 66.1% stake is being acquired from promoters at the agreed price of 1300 per share. The acquiring company may choose to offer a higher price to the minority shareholders depending on the stake it wants to acquire.

Found it at the bottom of the annual report - https://www.bseindia.com/xml-data/corpfiling/AttachHis/a6154a90-4b1c-4455-bb47-c0ba94e82e81.pdf

Got a couple of questions here…

Dr V has sold 66.1%. New promoters have made open offer for 26% at 1300. If they manage to get 26% they will own 92% and almost certainly thyrocare will be delisted. Minority shareholders will have a tough time being in an unlisted company…

New promoters are not offering for 100% of the company, they want only 92% - why is that? - this is very important. They are playing a game and their target is obviously retail investors who only have 6% stake - they want all retail investors to either sell on market or subscribe to the open offer.

What will those 8% who are not bought out do? They might get diluted if the company is delisted?

FIIs hold 20.5% and mutual funds hold 7.1% - these guys hold the power. I am not selling in a panic - the floor price is 1300. We might even see the share price trending up similar to what happened in the case of vedanta…

Dr V has left retail share holders in a lurch…disappointed with his decision…He sold it too cheaply.

Approx figures - 100 crore profit making company growing at 20% sold for 7000 crores (less if you take out 8% shares they are not going to pay),PE multiple of 70 or less…

Discl - not selling, might add more…

I have few thoughts and doubts, open offer trigger may just be a formality and may never go through. Most of the times when open offer in such cases is below or near the trading price, it just means a formality and becomes history. If any promoter is serious about it he should do this at somewhat higher than trading price. Why would MF or FII or even retail investors do tender at lower than trading price?

So although I cannot comment for sureity and I don’t hold significant percentage so can maybe think calmly over it without bias and with past history of say ABB power products recently…where I got purturbed by open offer and did not buy it at lower prices only to buy later when open offer became history later…I do not feel open offer is a risk…I maybe wrong…

The bigger risk I sense here from recent comment of Dr V in ET now when he was asked something about why would a unicorn/PE look at thyrocare in terms of growth, profits etc. And his answer was surprising to me…instead of mentioning good growth and profit in diagnostic, he mentioned that thyrocare maybe a tool for API to acquire customers and real profits may come from the medicine part of their other business…seems suddenly he is more bullish of the other part of pharmeasy and hence the exit and buying stake in pharmeasy…what I as a begining shareholder of thyrocare was uncomfortable about was instead of showing confidence in this piece of business which he built and sold, he only looked at it from customer acquisition for the main business angle…now is that true? Will thyrocare just be used for customer acquisition for pharm easy or will it grow in revenues and profits better than the existing pharmeasy piece or benifit from the other pharmeasy business piece after buyout and that’s also why API looked at it? I am confused now.

Disc. Hold tracking position and biased. Not a buy/sell recom.

Fair points…

Regarding growth in diagnostics business - I have no doubt that it will grow 10-20% for the next 10-20 years. I can’t comment on pharmeasy’s other businesses…

My previous post was the worst case scenario for thyrocare’s non-promoter shareholders.

What about the best scenario for us…

1, The promoter does not get the required 90% to delist the company, and thyrocare remains listed

2, Pharmeasy might bring even more business to thyrocare which will enable thyrocare to grow even faster

3, Change in the promoter is probably what thyrocare needs for the next phase of its life

4, The new promoters might sell Nueclear (good riddance if they do that) - which will increase the profitability of thyrocare even more

Discl - hold a significant parcel, I am not selling

Agree on the growth rate of diagnostic business unless pharmeasy further squeeze the margins by using thyrocare as customer acquisition tool and make profit in their other business instead…I am not sure if that they will do that but with dr V completely exiting thyrocare and investing in the other piece and sounding more bullish on other piece and moreover talking thyrocare as a customer acquisition value add to pharmeasy made me think if at all we want to be part of thyrocare story , is it better to be in it or now in pharmeasy when it lists…and for pure play diagnostic look at metropolis or dr lal instead?

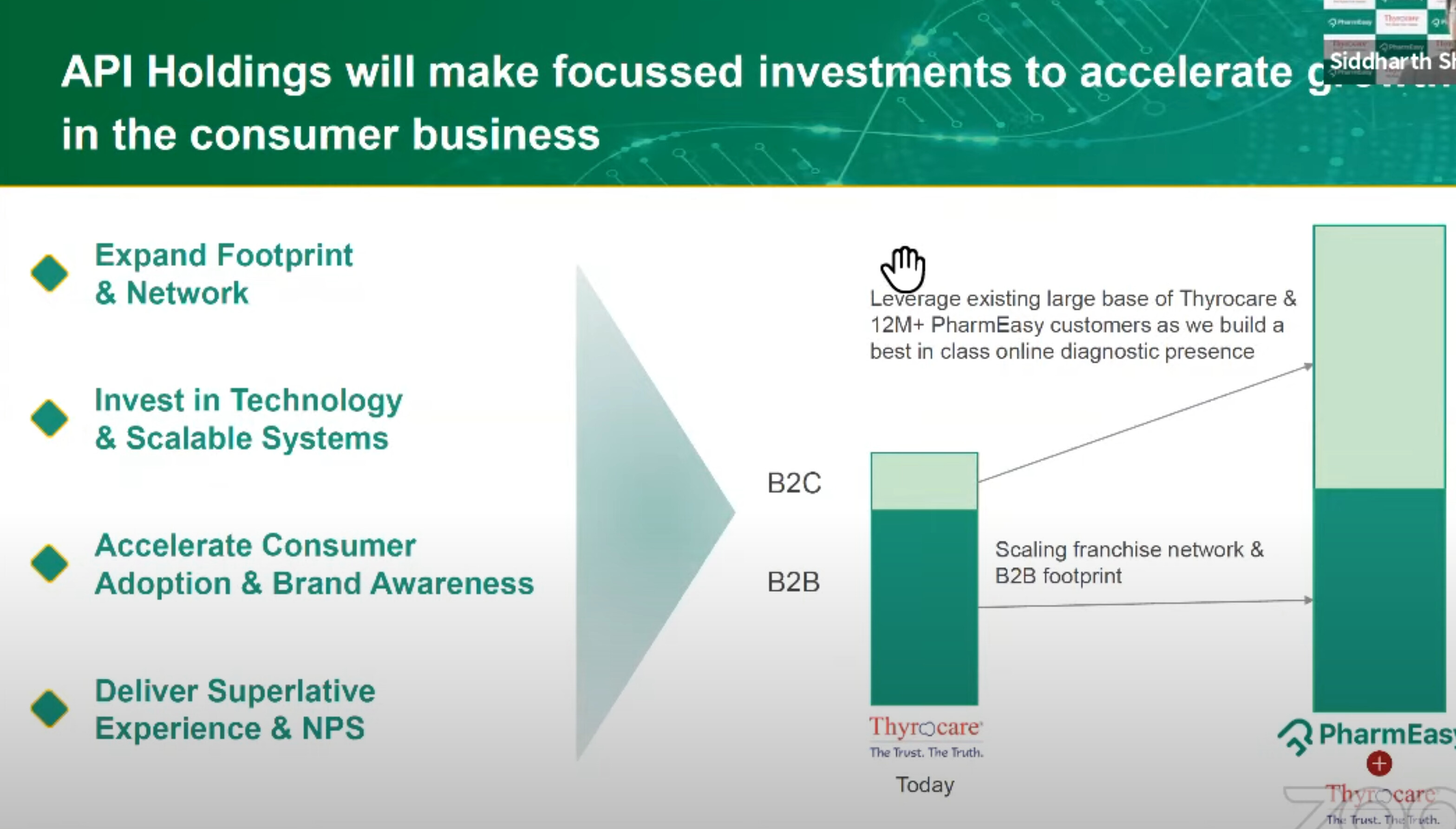

You need to watch the interview video from ET now and will answer many of your questions. Sidharth Shah, CEO of pharmeasy is so bullish on thyrocare!

Pharmeasy thyrocare acquisition analyst meet video.

Pharmeasy wouldn’t want this to run as a separate public company as it will cause lots of problems to them in terms of ensuring that all transactions between them and Thyrocare needs to be at arm’s length. So delisting is certain imo. Open offer at 1300 is a joke. Why would anyone sell below the market rate? I think delisting will happen atleast x% above current price. Made a mistake in Vedanta spl. situation by not being patient and realizing the gains… this is one not to let go…

What is the value of x in your understanding? Is it anyone’s guess ?

I agree to your points, but nothing can be certain here… obviously they would have some limits beyond which they would not want to pay for delist…also I don’t think there will be any material transactions between thyrocare and their other business other than synergies…what transactions do you foresee?

PharmEasy has tremendous vision and hunger its not hard to see why Dr.V decided to send his baby where it belonged. I have been disappointed with quality of growth shown by Thyrocare which is primarily driven by B2B volumes (by cutting EBITDA margins pre-Covid and then with the Covid volumes) and the ad spends on branding done sporadically with no intent to go all in with B2C diagnostics. I think this is where PharmEasy has found the perfect fit in Thyrocare because they will now invest in B2C diagnostics frontend for Thyrocare that is integrated with the rest of their vision in digital consultations, digital diagnostics and digital pharmacy. They want to build a Uber/Swiggy sort of interface for healthcare with the patient and it is this sort of vision and hunger that has been missing in the company.

They will most likely mine the patient diagnostic data in the long-run having this info in the cloud acquiring lifelong Customers with knowledge on their specific healthcare needs.

As for what happens to business being listed/delisted, or the open offer (or the floor price), is anybody’s guess. Around 20% is held by FPIs and 5% by MFs and less than 5% by small retail like us. We simply don’t have a say here. I am not sure if Nalanda and Arisaig (together hold 13%) will sell out after having made relatively very recent entries. I don’t think the open offer at 1300 will work and I don’t think the business will get delisted anytime soon.

There is however an intriguing play that may happen if PharmEasy chooses Thyrocare as a vehicle to list itself without an IPO - sort of like a reverse merger. I highly doubt if the high profile investors like Temasek and TPG will look to list without IPO fanfare so this is a remote possibility in my opinion.

Best case for us minority shareholders would be if the business continues to remain listed and PharmEasy management focuses on B2C tech and continues driving the business with hunger that I think they possess. There is still the possibility of Thyrocare getting shortchanged in related-party transactions with the parent (For eg. who owns the B2C platform being built) but at this stage its better to be hopeful. I intend to hold onto my shares and see where this goes.

I have tremendous respect for Dr.Velumani and I think he has done the right thing in both selling his stake (I don’t think he is the kind to let a professional management do its job on their own) as well as in investing 1500 Cr back in PharmEasy - this gives him a piece of the pie driven by a hungry management that probably reminds him of himself when he was young, in a broader healthcare space than in the narrow diagnostics space

Disc: Invested

@sahil_vi as @phreakv6 has mentioned thr delisting price depends on the institutional investors. But I hope they are smart enough to figure out that this is an Amazon/Flipkart for Healthcare in budding and not throwaway their leverage easily. I am going to initiate a position on Monday (one part through AMO order and another depending on Monday’s price action)

Hi all

A basic question on the business model. How is Thyrocare able to get away with having so few labs in comparison with Dr Lal Pathlabs and Metropolis?

What is the catch here? Is the testing time slightly longer because of the need to transport for longer distances (since they have fewer labs)? Is there a lot of concentration of volumes due to B2B business (i.e. significant volumes driven by large B2B customers like hospitals located closer to their regional labs which doesn’t impact their lead times)?

They are/were very B2B focused, atleast in the past. Most of the volumes are from small mom and pop labs that outsource not so easy tests to Thyrocare. Samples are collected by small lab in area on same day and shipped to larger processing lab(Mumbai in my case) by flight. Generally results are available the next morning or so. However, because of the pandemic Thyrocare has had to go more direct(because volumes that small labs would process have fallen off a cliff), which I felt was lacking(very poor online channel and CEO who was brought in to fix this exited). I sold recently just before this deal was announced to my misfortune for that same reason and because of valuations ex- Covid. PharmEasy deal should fix that issue.

Thank you.

So there are two cases - please correct if I am wrong.

Simple tests like say blood sugar test in which case the local lab will themselves analyse the samples. In this case the market is not addressable by Thyrocare?

Complex tests - is it possible that this could be directly processed in one of the 200+ labs that Dr Lal Pathlabs operates, whereas in case of Thyrocare, it has to be first collected by the local lab and then needs to be sent to Thyrocare’s regional or central lab. Hence if a customer reaches out to Dr Lal’s lab (not its collection centre), they would get the results faster than by sending to a local lab that is serviced by Thyrocare. So while B2B is better margins, B2C is critical for growth, and hence the acquisition by PharmEasy is vital for Thyrocare’s long term sustainabiliity.

I understand speed is not the only factor to consider while assessing B2B vs B2C.

I can’t comment on what Lal Path does as they aren’t in my state. You are completely right with #1 and #2 for Thyrocare and small labs. The speed is never a problem. Patients are OK with waiting a day(or even more if necessary). B2C has higher margin, but also higher marketing costs and more competition. Using online channel and smaller labs/personnel who can collect samples on fly/from home is a smart thing to do IMO. Keeps costs/capex low and can scale quickly with asset lite model.