A ) Company Overview:

•Thyrocare is one of the leading pan-India diagnostic chains and conduct an array of medical diagnostic tests and profiles of tests that center on early detection and management of disorders and diseases.

•As of 29th February 2016, Thyrocare offers 198 tests and 59 profiles of tests to detect a number of disorders, including Thyroid disorders, Growth disorders, Metabolism disorders, Auto-Immunity, Diabetes, Anemia, Cardiovascular disorders, Infertility and various infectious diseases.

•The profiles of tests include 16 profiles of tests administered under the “Aarogyam” brand, which offers patients a suite of wellness and preventive health care tests.

•The company primarily operates their testing services through a fully automated CPL (Central Processing Laboratory) which is located in Navi Mumbai and through the network of Regional Processing Laboratories (RPLs) located at New Delhi, Coimbatore, Hyderabad, Kolkata and Bhopal.

•Thyrocare has nationwide network of 1,041 authorized service providers comprised of 687 TAGs (Thyrocare Aggregators) and 354 TSPs (Thyrocare Service Provider) spread across 466 cities and 24 states and 1 union territory as of 29th February 2016.

•Nueclear Healthcare Limited (NHL, Thyrocare’s wholly owned subsidiary) operates a network of molecular imaging centers in New Delhi, Navi Mumbai and Hyderabad, focused on early and effective cancer monitoring.

B)Scalability Scope of Industry and Company:

The domestic diagnostic market is highly fragmented and has a current size of ~US$6.2bn. The industry is expected to grow at 16‐18% CAGR to ~US$9.3-$9.8bn by FY2018 as per CRISIL estimates.Diagnostic centres in India can be classified as hospital‐based, diagnostic chains and standalone centres. Standalone centres form the majority share (48%) followed by hospital based (37%) centres, while diagnostic chains account for the balance (15%). The absence of stringent regulations and low entry barriers has led to the evolution of standalone centres, while hospitals tend to have their own pathology labs. Within diagnostic chains, large pan‐India chains form 35‐40% and regional chains form 60‐65%.

Specialized tests require expensive infrastructure, which has led to the formation of diagnostic chains in India. These follow the hub and spoke model and enable economies of scale. However, the fragmented nature of the industry indicates lowpricing power for service providers in the near term.The key drivers for the industry are- increase in evidence-based treatments, huge demand-supply gap, increase in health insurance coverage, need for greater health coverage as population and life expectancy increase, rising income levels making quality healthcare services affordable, and growing demand for lifestyle diseases-related healthcare services.

Does Company Hold a Scalable model ?

TTL has a portfolio of specialized tests with an emphasis on wellness and preventive healthcare. Wellness and preventive healthcare industry is expected to grow at a CAGR of close to 25% over the next three years. Currently, organized pan india diagnostics chain have 35-40% market share which presents a huge opportunity to grow in future TTL’s multi-lab model is comprised of a fully automated CPL supported by its network of RPLs that conduct routine tests conducive to high volume testing. Where logistically feasible, the authorized service providers direct samples requiring such tests to the RPLs. By routing these tests to the RPLs, the resources of the CPL can be utilized to process and test the additional samples generated by its pan-India network of authorized service providers that are not proximate to an RPL.

What is the Expansion Plan?

TTL intends to expand its diagnostics test offerings through the acquisition of new technologies, including both instruments and processes. It is planning to strengthen and grow its coverage of regions across India through the network of RPLs and authorized service providers. The company is targeting network of 25 RPLs from current 5. The expansion could increase its customer base, generate higher volumes of samples for processing, improving turnaround time and optimize company’s logistics costs.

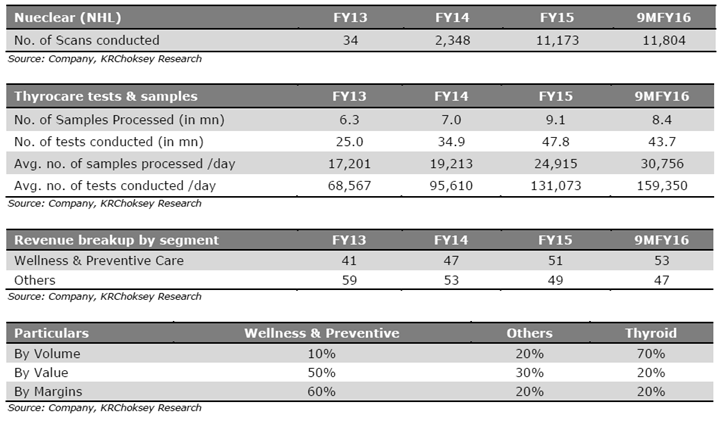

TTL is also developing a network of molecular imaging centers (radiology) for cancer diagnosis through NHL. It currently has three imaging centers operating five PET-CT scanners. TTL is aiming 40 PET-CT scanners in addition to 5 cyclotrons from current 1.

C)Business Model: (Asset Light, Debt Free, High Cash Flow , ROCE Best in Class)

Thyrocare’s multi-lab model is comprised of a fully automated Central Lab (Navi Mumbai )supported by a network of Regional Labs that conduct routine tests (high volume). The authorized service providers direct samples requiring such tests to the RPLs. By routing these tests to Regional Labs, the resources of CPL can be utilized to process and test the additional samples generated by pan-India network of authorized service providers that are not close to any Regional Labs. As number of tests grow, Thyrocare will achieve economies of scale and witness a lower cost per samples and tests. It could pass on these cost efficiencies to customers thereby offering tests at affordable rates. Offering tests at competitive prices is conducive to the expansion of customer base, which may in turn increase the number of samples and tests it processes.

Business Operation Overview : TTL has built a nation-wide network of ASPs that source samples for processing and testing by the RPLs and CPL. As of November 30, 2015, it has a network of 1,122 ASPs(Authorized Service Provider), comprised of 878 Thyrocare Aggregators (TAGs) and 244 Thyrocare Service Providers (TSPs) spread across 483 cities and 27 states and 1 union territory. ASPs have helped the company to penetrate the Indian market and increase the volume of samples it processes, as they collect samples from hospitals, clinics and potential patients located across India. In order to optimize the logistics costs, TTL established RPLs in regions with close proximity to rail or roads network. If the location of an ASP is such that it is not feasible to send the samples to an RPL, or the sample requires non-routine tests, the ASPs send these tests to the CPL via air cargo, rail or road networks and/ or courier services. RPLs have thereby assisted TTL in optimising logistics costs. Additionally, the time involved in delivering the samples to the RPLs is less than that required to deliver samples to the CPL, thereby enabling TTL to provide test results to patients relatively faster. TTL’s information technology infrastructure supports the ASPs’ network. The operations of the ASPs, RPLs and CPL are seamlessly facilitated on the virtual network through TTL’s internal software “Charbi” and “Thyrosoft”, which were developed by third party software developers. ASPs enter work order data on Charbi, which is accessed by the CPL through Charbi or by the relevant RPL through Thyrosoft for local processing. Once received, the test results are uploaded onto Charbi, which can be accessed by ASPs. Test results are also made available to ASPs on TTL’s website.

Why the operation Require Minimum Capex and Working Capital ?

It’s a B2B model as Thyrocare services laboratory partners rather than consumers directly. This differentiated Model enables Higher Margins: Unlike other organized Player , which operate more on a B2C Model. From B2B segment for Thyrocare 85% of its revenue coming through the channel( as against 30-40% for its peers).This enable the company to keep its other expenditure lower vis a vis it’s peers , which spend higher on promotional expense. In term of services , the company is more focused on the preventive and wellness which is 6% of the Industry but less competitive , and the non preventive segments, while its peers follow a portfolio model of providing a full range of tests and services , which reasons higher manpower costs.

The company’s volumes and strong ties with its vendors has enabled it to develop an equipment leasing model for the CPL that has resulted in minimal capex for its otherwise expensive diagnostic equipments. The model entails leasing of equipments and instruments for the CPL in exchange for a commitment to purchase reagents and consumables from these vendors for a specified period of time. The RPLs conduct routine tests which do not require complex equipments; Hence, the capex required for equipments is minimal and the same are purchased outright by the company. Additionally, the premises required to set up these RPLs are leased, thus resulting in lower capital outlay to set up these RPLs (2-3cr required for set up a RPL). As a result, the company has been able to expand its operations without relying on debt. The company as of 9MFY2016 has no debt on its books.Low capex requirements and high asset turnover along with high margins enable the company to generate high ROIC on the core diagnostic business, which is around ~40%. This will enable the company to fund its growth with ease and warrant it to make a high dividend payout. In fact it has cash and bank and investments of 91cr as of FY2015 on a consolidated basis. The net cash flow from operating activities is around `40-45cr/year and will be used to fund the next phase of growth.

Why margins are Higher than the Peers?

Operations are Automated : The company’s operations are relatively more automated in nature, thereby requiring less manpower Intervention, unlike its peers which need to employ qualified manpower like Phds and doctors. As a result, employee costs for Thyrocare account for 10% of sales V/s 20% of sales for its peers. This contributes towards the company enjoying better margins compared to the industry (~41% for Thyrocare’s diagnostic business V/s ~26% for Dr Lal Pathlabs). This coupled with the low capex requirement for the diagnostic segment makes its diagnostic business a high ROIC business. This it has minimal requirement for day-to-day working capital which supports its ROCE. It also has one of the highest EBITDA margins in the industry.

Thyrocare Brands:

Operational BreakUP

Business Strategy and Growth Driver:

•Intends to grow its Wellness and Preventive offering from 51% in FY15 to ~80% over FY2020. The management expects the business to have high growth prospects and low competition segment coming to preventive care, Aarogyam has grown 30% CAGR over the last five years. So, MANAGEMNT believe this will be the engine of their future growth and will clock 30% growth for next few years. In time, this segment accounting for 75% of our revenues.

- The management intends to grow its network of RPLs (augmenting 10 RPLs in FY17E & FY18E) and authorized service providers. Thyrocare intends to add 75 RPLs going forward, with INR 30mn investment/ RPL with a total investment of INR 750mn.

•The management anticipates robust growth in the Nueclear business vertical, which became EBITDA positive in 9MFY16E and should become PAT positive by the end of FY17E.

•Company is in very high growth Industry and there is a remarkable change that is moving from unorganized sector to organized sector

•The preventive healthcare - the kind of health consciousness coming in companies now requiring every employee joining them going through all these tests. This is all opening up a huge market for these companies.

D)Financial Performance

Company has demonstrated attractive financial performance over last four years. For FY2011-15, its compounded annual growth rate (CAGR) for sales is 23%, where the sales grew from INR 78 crore to INR 180 crore in FY2015. The company’s operating profit grew at CAGR of 20%, from INR 35.6 crore to INR 73.0 crore in FY2015. Its profit CAGR has been 18% from INR 25.0 crore to INR 48.5 crore in FY2015. The company has no debt on books. In fact it has cash and bank and investments of Rs91 crore as of FY2015 on consolidated basis. The net cash flow from operating activities is around INR 40-45 crore per year and will be used to fund the next phase of growth.

Management Overview

Dr. A. Velumani is the Chairman, CEO and Managing Director of the company. He has over 19 years of experience in the diagnostics business. Born in Coimbatore, Tamil Nadu, Velumani spent 15 years as a scientist, and left his job at the Bhabha Atomic Research Centre in Mumbai because he “wanted to do something different”. The immediate reason for starting Thyrocare was fairly straightforward: He had a PhD in thyroid biochemistry. Using money from his provident fund, Velumani started his first lab in Byculla, Mumbai, in 1996. He soon began expanding to other cities. “The growth was pulled [by demand], not pushed,” he says. Since the business started generating cash from the first day, Velumani claims he did not have to borrow money ever. He continues to own a majority stake in the company.

Business Risk and Concerns

•Highly fragmented market with intense local competition (standalone centers are 48%, Hospital Based Diagnostics 37% and Diagonastic Chains 15% of the industry).

Thyrocare directly competes with some major diagnostic players like SRL Diagnostics, Metropolis and Dr Lal Pathlabs. In addition, there are many small and independent clinical labs aswell as labs owned by hospitals and physicians

•The industry faces risk with changing technology and new product introductions.

Advances in technology may lead to the development of more cost-effective tests that can be performed outside of a diagnostic laboratory, such as point-of-care tests that can be performed

by physicians in their offices, complex tests that can be performed by hospitals in their own laboratories and home testing that can be carried out without requiring the services of diagnostic laboratories. The development of such technology and its use by customers would reduce the demand for laboratory testing services and negatively affect revenues.

•High investments in the imaging business with high gestation periods would keep the profitability in check.

Thyocare’s consolidated ROIC will come under pressure in the near term as it has entered the molecular imaging space by acquiring Nuclear Healthcare Ltd (NHL).According to the company, this business will take 3-4 years to attain peak profitability while it accounts for almost 40% of its fixed assets of the company (as on 9MFY2016). Thus, though Thyrocare could potentially provide listing gains, the pressure on its ROIC in the near term and the not-so cheap valuation demanded by it will keep the upside in the stock limited.

Disclaimer : Not invested as Valuation is out of comfort Zone . Studied the company to get an idea on healthcare and Diagnosis Sector. Some Notes are taken from various brokerage Reports , newspaper articles and management interview…