My understanding is that thyrocare will not take undue advantage and he will not try to make “excessive” profits from a dire situation like covid! Do you have any news items or interviews to back your claim? I don’t think he ever said he will not make any profits - he is recruiting like crazy because of the increasing demand - how is he going to pay his staff??

Market agrees with my assessment - gone up 40% in the last few weeks

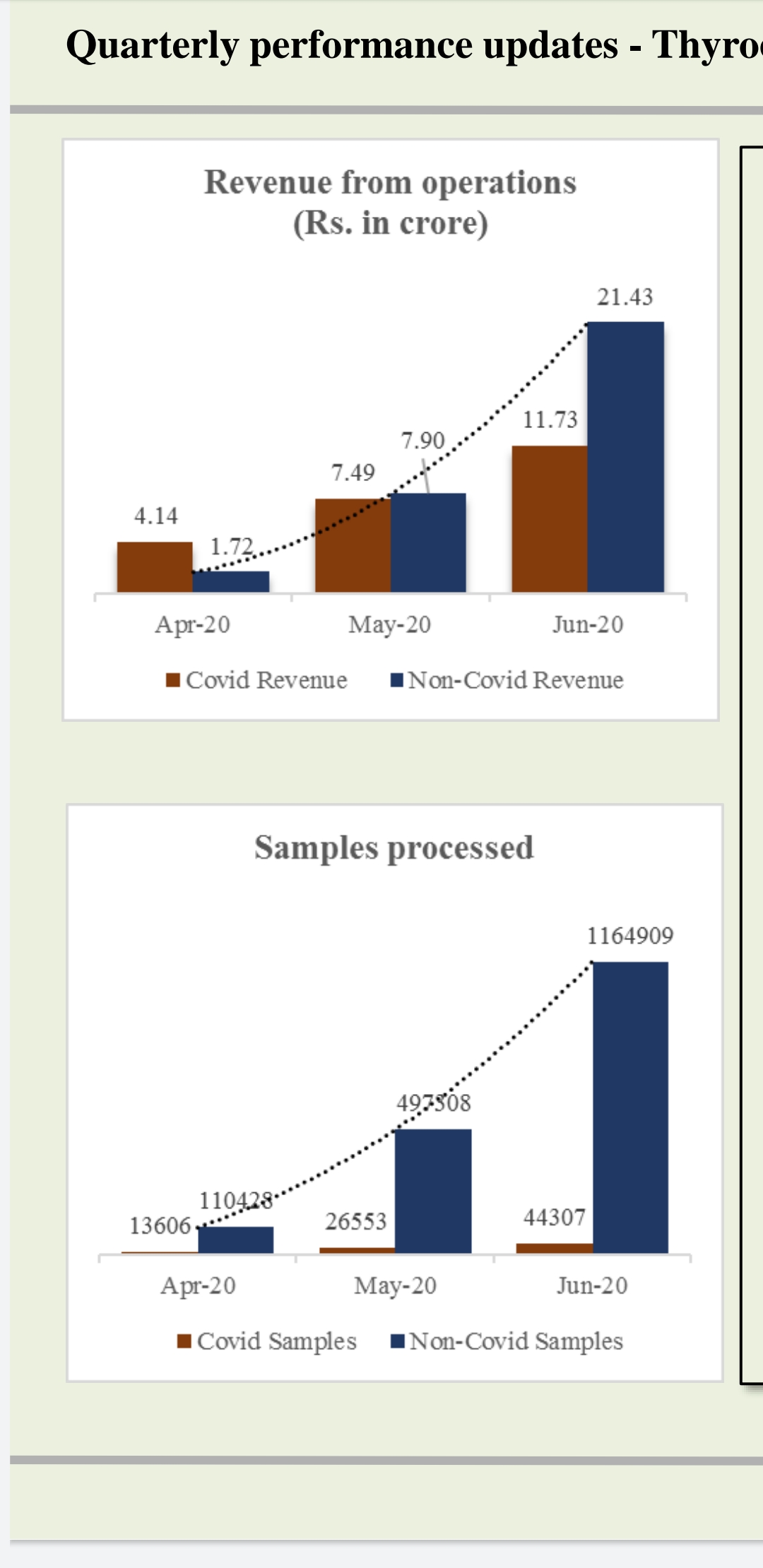

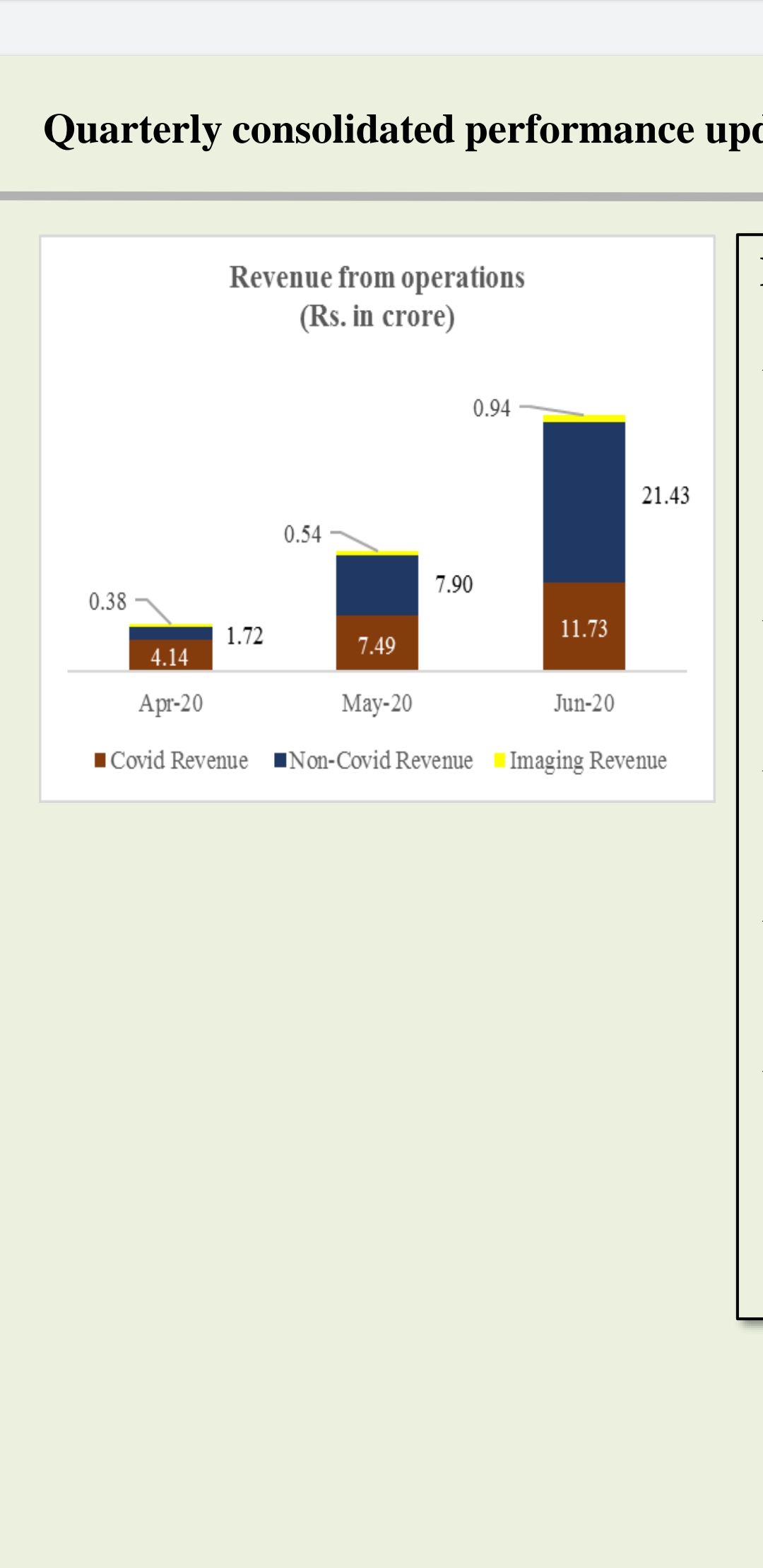

Headline report is disappointing and not unexpected given the near zero non-covid business but, the cash flow is much much better.

Nueclear business will struggle for a long time and in my view, if some one is interested in thyrocare it is better to concentrate on the pathology business and its cashflow…There will be more impairment in the Nueclear business in the near future…

Pathology business actually made a net profit of 4.42 crores + add depreciation of 4.48 crores = 8.9 crores cashflow

Consodlidated also not too dire - 0.23 crores net profit + add depreciation of 6.97 = 7.2 crores cashflow

Mainstream tests coming to regular growth + top up of Covid tests , if we take June as baseline ( 21 cr + 12 cr) *3 = 100 cr, this is already similar levels at Q1 2019.

Going forward = Manstream revenue stabilized ( pent up demand + regular growth with prevetive health awareness ) and covid tests as top up at least for few Qtrs, good tailwinds for sector and thyrocare.

With revenue side more visible, would be interesting to see how margin profile evolves with covid tests in the mix.

Where to find this info of top shareholders? I could only find people holding more than 1%, but not sure how to check for top 200 or 1000 shareholders. Appreciate if u can share this info.

Wow, another hefty rise to an all time high! I didn’t think share price would appreciate this quick…I have been accumulating since the IPO in 2016. Strong conviction and knowledge in this field prompted me to buy more and more when investors were giving up on the Thyrocare story, especially the retail investors. Most importantly the promoter was top notch and trustworthy…

I have seen thyrocare disappear from many portfolios shared here over the years…Retail bought during the hype of the IPO and sold as the share price depreciated…Have a look at the shareholding pattern - retail investors only hold some 7%. It used to be 12% or higher…

The market cap of this leading diagnostic company is still only 500 million USD. Think about it…The total market cap of the listed diagnostic companies is approximately 3.6 to 4 billion USD. Diagnostics industry is growing at 10-20% and this will continue for 10-20 years.

This is quite the news .

Was any reason given for such a step?

Why bring an outsider , when promoters have done such a fantastic job of running the company

Dr. velumani said in the interview, he wants some outsider who is fresh to the company with non-medical background ( preferably having marketing experience/background) to be the CEO. Couple of candidates are shortlisted and mostly this position will be filled with in a month. He also told that his children are too young to take that chair and they told they don’t want to inherit that chair.

This decision is taken from the better governance perspective as he alone holds the position of MD, Chairman and CEO.

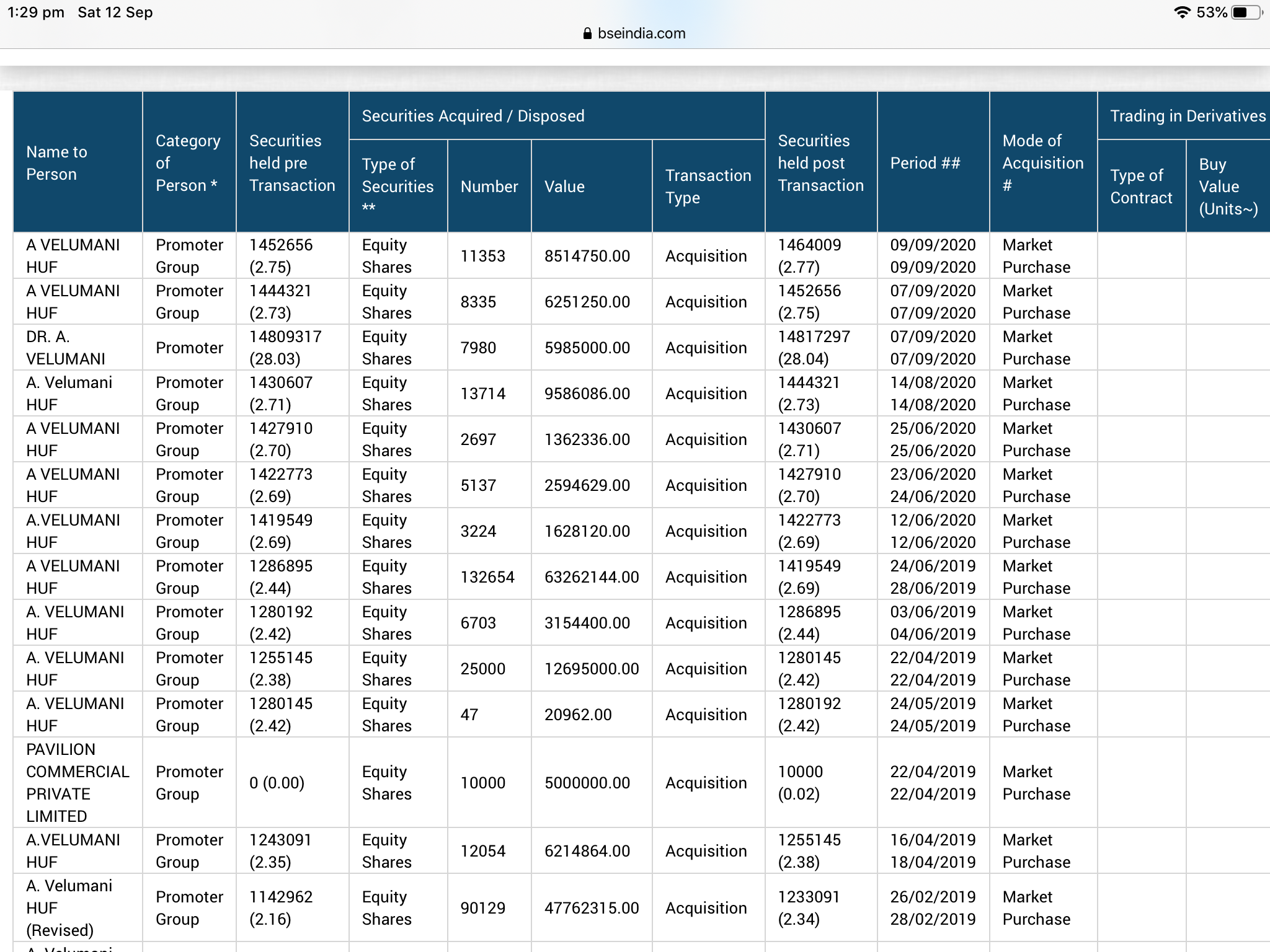

Also could see promoters continuously buying from the open market.

Optically PE looks high 67 odd at the current market price of 782 - that is because E has halved due to Covid, a temporary disruption in business. Market is looking beyond Covid. There is a very long runway for this business.

Why is Dr Velumani buying on market even at these prices?? He knows much more about his business than anyone else…

Arindam is ex ceo of SRL and cfo of sterlite tech. The alumni pedigree is great. coalgate ex is of pre 2000 and we should not count.

I would have loved if they have got some one from marketing or the one who have built strong digital channels. Again Velumani is still the key differentiator for me to stay put in this.