Most hospitals have stopped almost all elective surgeries and infact discharging patients to prepare wards and ICUs in anticipation of covid 19 cases

The first order effect of COVID-19 tests on the bottomline/topline of diagnostic companies will be limited. However these companies will be transformed in many different ways after this pandemic. This is just an opinion - I am not aware of the higher order changes, I need to do more research on that.

Disc: holding (about 5% of portfolio).

Datar Cancer Genetics has published their research online. If there is an objective review of these papers it would be really useful.

Disclosure: Holding 5%. I am not a medical professional. I have no knowledge on diagnostic science.

Liquid biopsies are completely different type of tests to tumour markers which thyrocare is promoting. Tumour markers have been around for ages, whereas liquid biopsies are recent advances in the laboratory technology…

Liquid biopsies are still in the research phase, they are still not used in routine clinical practice even in advanced countries…

Re - promotion of tumour markers as a package

Clinicians don’t generally use tumour markers to diagnose or detect cancers (why? - false positives are not uncommon). Clinicians rely on history, presenting symptoms, scans and biopsies to diagnose cancer. We only use tumour markers as a “diagnostic test” if all the above fail to give us an answer and if cancer is still strongly suspected.

Tumour markers are mainly used in the follow up of cancers once cancer is diagnosed - these marker/s could be used to assess response to cancer treatment and they are also useful in predicting relapses after cancer treatment is completed.

The above mentioned are the reasons why most clinicians won’t favour routine blood testing of tumour markers…

Nalanda increases their holdings significantly on 25th.

3 Likes

Thyrocare is doing well compared to the share market in general and for good reasons:

Balance sheet - very strong, no debt and plenty of cash. So no chance of going broke. No significant lease liabilities… This is the first thing one should look at…balance sheet is more important than profit/loss during such extreme situations. Survive first and grow when the situation improves

Revenue - will drop in the short term but expenses will also drop (less consumables - which is 30% of revenue), staff revenue is 10% of revenue will go up relative to revenue…but that is ok

Covid-19 testing - no idea about the profitability of this new testing segment

Management with skin in the game and significant stake in the business - 66% promoter holding and minority shareholder friendly

Take care every one

Best wishes

3 Likes

1 Like

1 Like

Any idea…what happened to this proposal of Dr V buying back this business ? Is it still planned or has been deferred indefinitely.

It is clear that Thyrocare will not make any money from Covid-19 swab testing, but they will accumulate enormous goodwill

But I see a great opportunity for thyrocare in antibody testing (blood) in the near future and in the medium term. Antibody indicates immunity (and could be negative in the acute stage when the patient is suffering from the covid infection - nasal swab is the test to do in the acute stage).

2 Likes

Directors rejected the proposal…Nueclear remains within thyrocare family

Thanks so much for the amazing insights Aniket … Worth it’s weight in gold.

1 Like

Like the clarity in promoter’s thinking. Need to brace for poor numbers in Q4 20 and then very poor numbers for Q1 21.

1 Like

Yes, indeed. Companies with stronger balance sheets will surely be much more resilient to the unprecedented crisis situations such as this where a big healthcare crisis has accompanied a big economic crisis. Thyrocare, being a very low leveraged entity along with its established diagnostic care operations should be placed more comfortably to come out relatively faster out of Covid-19 crisis.

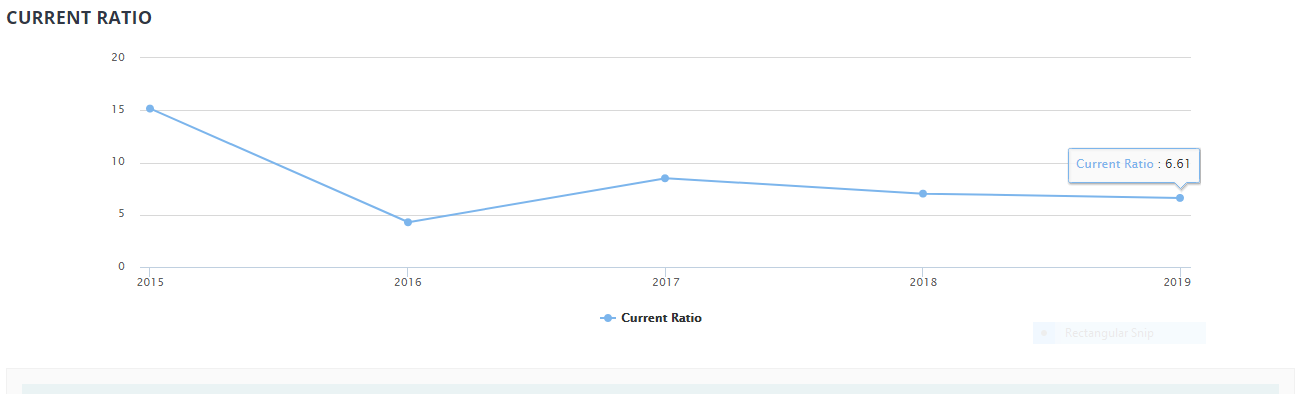

It has had near negligible debt-to-equity ratio hovering around 0.01 for last few years. Moreover, to look deeper, it has very delivered a very healthy current ratio as well in those years with last year’s figure being at 6.61 , as evident from the chart below:

This indicates a strong liquidity position of the company wherein it can pay back its short-term liabilities with its short-term assets. That means the company does not need to tap other sources of liquidity to meet its current obligations, which is a very good sign as far as stability on the operation front is concerned in times of uncertainty.

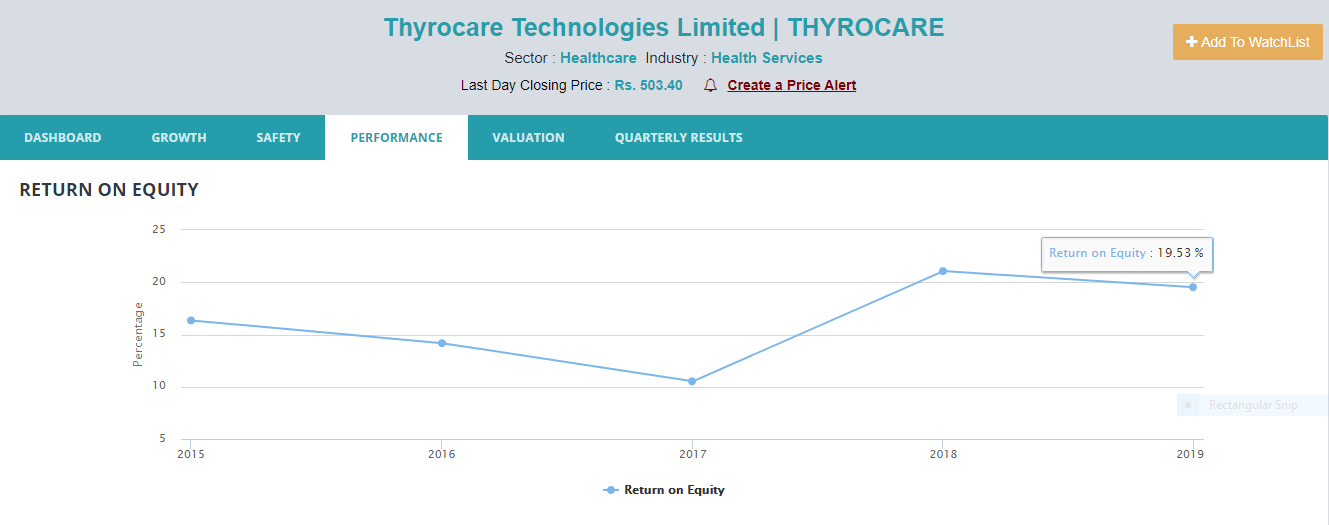

What is more commendable is that by way of its efficient business operations, it was able to squeeze very healthy profits with respect to the money put into the business which has resulted into stronger return-on-equity for Thyrocare Technologies over the last few years :

Being a ratio that attempts to bring together a balance sheet & P&L statement, a better return on equity ratio signifies the profit-making abilities of the company with respect to its net worth. So in the case of Thyrocare Technologies superior return on equity combined with very modest debt suggests that its a high-quality business that is more resilient and less prone to the economic downturns. To add to that, plenty of cash on its book Thyrocare Technologies can be counted amongst the companies which are supposed to display more stability and come out stronger & faster out of the uncertain and volatile times.

4 Likes

Glad I could help Srinivas! ![]()

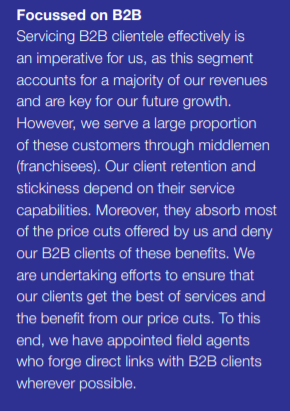

Thyrocare serves its b2b clients through the franchise partners. metropolis & dlpl have a different partner which sources samples for b2b. (in some areas where the franchise partner is not available for b2c, this b2b will do both businesses)

Dr A Velumani also wants to serve the b2b clients directly as the price cuts are not reaching the b2b clients who are other labs & hospitals. Removing the middle man could further help thyrocare be the lowest cost producer by a wider margin which strengthens the moat further.

Source- AR 19

2 Likes

Rs 1000 profit per covid swab test!!!

1 Like

Its nice to see that its a profitable and not just a chartiable venture for Thyrocare and there is a possibility of expansion of margins as volumes increase. I am more curious to know if their normal Thyroid and Aarogyam tests are considered essential services. Are they currently operational at full capacity? There is an announcement that Nueclear operations are suspended (may not affect numbers much) but no such thing for normal tests.

Diagnostics collection centers will be opened from 20th apr according to MHA circular.

The promoter had warned that the revenue was almost zero since the lockdown

1 Like