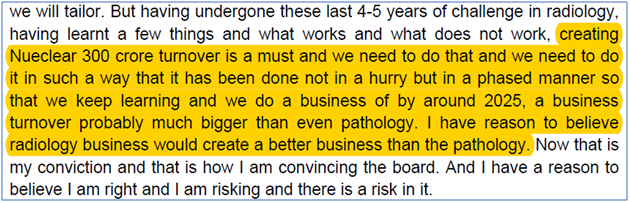

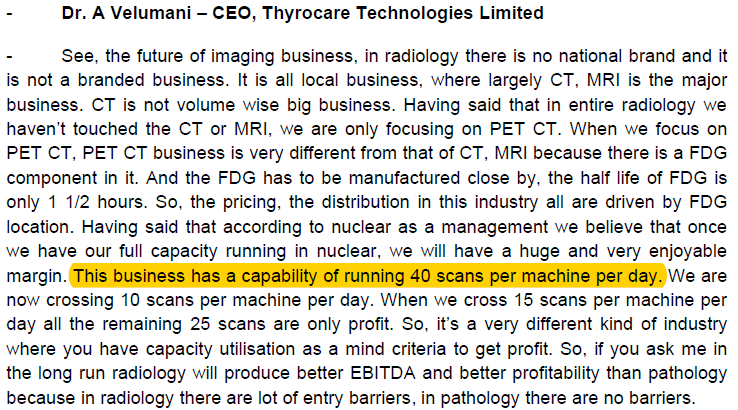

Below highlighted statement by Dr. Velumani saying that 1) radiology business would create a better business than pathology and 2) radiology business turnover probably much bigger than pathology by 2025…made me do a high-level NPV and IRR analysis.

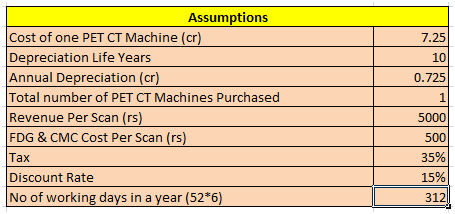

Below sharing NPV and IRR results using conservative assumptions of revenue from 1 PET CT machine with life of 10 years with straight-line depreciation and residual value of zero. In the first year machine would do 10 scans per day (they are doing 12 per day today) increasing by 15% every year reaching 35 scans per day in year 10.

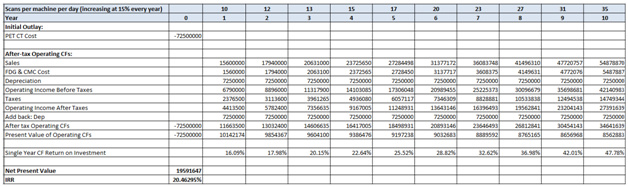

Numbers are pretty impressive. Get positive NPV with discount rate/opportunity cost of 15% and IRR happens to be 20.46%. The best thing is that as scans per day increases to 21-22 per day, it generates almost 30% ROI in after-tax cash flow terms. In first 5 years, business recoups initial investment (in after-tax CF terms) and then generates twice the amount of initial investment in last 5 years when the business is scaled up.

It is high CAPEX and low OPEX business model. With most of the machines managed and operated by franchisee, Thyrocare management can simply focus on adding the PET-CT machines at right locations with right franchisee partners.

All views/comments invited.

Disc: not invested. This is just a first stab and I have a lot of questions to better understand radiology business potential and its possible impact on the overall numbers.

Just to keep you updated, on my complaint one of Thyrocare’s senior executives investigated the matter and shared his finding with me. It was found that the local service provider had erred on two accounts. First, he was supposed to take an additional sample for the kind of tests I had opted (which he didn’t). Secondly, he dispatched the samples one day late. Thyrocare said that they would be dealing with the service provider as per company policy. They offered me a full refund of money spent by me, which I initially declined. But had to accept later as they didn’t have their in-house technician in my city and told me the same service provider would come to take the re-sample, which was not acceptable to me. I must say I am really impressed with their speedy action. So, there is nothing wrong with the company ethically. How effectively the company is going to deal with such errant employees is yet to be seen.

Thanks for the analysis and sharing the spreadsheet.

I have a question regarding the scans per day per machine. As per my understanding, a CT scan takes about 2 to 5 mins. PET scan takes around 20 minutes (and it can be higher for different body areas). This is just the time spent on the scanner. The preparation time per patient also needs to be taken into account. Even if we assume an efficient staff who do the next patient prep in parallel, one is looking at an average of around 40 mins per scan?

Assuming that the center manages to perform 20 scans/day/machine. We are looking at around 13.5 hours of scanning. Is it reasonable to assume that scan centers operate such long hours?

My guess is that initial full-body scan would take longer. But once cancer cells are identified in the body part, future scans would be limited to that body part only, decreasing the amount of time taken. However, this is my guess. I am not an expert in PET-CT and would like to hear from any PET-CT expert participant on this point.

The Pet scan would be needed to be done for the full body. It’s done to look for metastasis of tumour. SO usually you would do full body scan. And usually the follow up can be done with simple ct scan for the part.

Not sure why you feel that company has cancelled the buyback. Actually they have utilized most part of designated 63Cr. (except for some loose change with which they cannot buy even 1 share). Approx 959,000 shares bought. (approx 1.8% of total issued equity).

Seems that buy back price of 615 was working as some psychological support during recent carnage. Post buy-back closure some favorable price may come our way.

you just spoke the crux of point i made earlier … there is no moat , there is no EOS etc.

Its a good business with very high ROE but with no entry barrier whatsoever and any money spent on brands is waste, as people don’t care about brand .

Lets see who turns out to be right in long run, may be market knows something i don’t know.

With due respect to your views and contribution, I would suggest to put points objectively without directly concluding something with very small sample size. Much appreciated if there are datapoints backing any conclusion to add more perspective to discussion. For example if you believe there is no EOS, it can be backed with datapoints that should show that with increase in volumes the Fixed+variable cost remains the same.

Similarly, some more datapoints and scuttlebutt for strength of distribution network, service quality would be helpful. Also, good to check if hospital which gave report same day did themselves or outsourced to players like Thyrocare you never know

Hi Really Sorry didn’t mean to spread the fake news but breaking news on Zee news was there yesterday morning in which they mentioned buyback is cancelled

Regarding strength of distribution network , i frequently see lot of labs and advertisement boards of Lal Path Labs while travelling but have not come across any board or any labs of thyrocare here in Central and North Delhi. - Thyrocare’s does not advertise much, it is a well known fact. They are predominantly B2B - they get samples predominantly from the small labs, clinics and hospitals through out the country. They have agents who collect samples from various places. Advertising is for B2C business (Dr Lal is B2C, but also B2B)

Also while i was searching for near by labs on google, there were around 4 labs of Lal Path as compared to 1 of Thyrocare and 1 of SRL Diagnostic in 4-5 km vicinity. – _You are talking about collection centers (they are not labs). Dr Lal is the market leader in the North

I don’t know how you can come to the conclusion? It is well known that there are a large number of labs (most of them are standalone or with very small geographic reach). Apparently there are 100,000 labs throughout the country. Thyrocare gets samples from these small labs!_

There is enough room for a number of players to grow in this field. One does not have to kill the other!

There are a few things which are in favor of organised labs (such as Thyrocare, DRL, Metropolis etc) - they have the size, operating leverage (massive automated machines which can deal with thousands of samples), lower cost of operations and quality.

If govt decides to regulate laboratory businesses organised players (they might introduce quality control for all labs and also might introduce price caps for certain blood tests) will prevail at the expense of small labs since the cost of running the lab will increase substantially for small labs and they will not be able to sustain for long…

I think before concluding distribution scale we must realise 1.Though they are national players, they have their own geographical concentrations of strength 2. Look at hub n spoke model n central processing lab location for better clarity n national distribution n concentration of branches, collection center etc 3. They r different in terms of product offering n product revenue distribution ( customer segment , type of tests ). I think there are some significant geographical , customer, product and management based differences which can be studied while going through various company collaterals in details for these 2 companies before concluding on small sample views (nothing bad it helps but only when all dots can be connected else sometimes, might lead to wrong conclusions )

I have been tracking Thyrocare since IPO, here are my 2 cents.

Cost wise they are very cost effective when you compare some established labs here in Pune.

Just yesterday I did Vitamin D3, B12 and CBC test for my kid which costed 2750 at a big reputed local lab and then called up Thyrocare to know their price, it came to 1800 but then they have packages for around 2K which covers many other tests (70+ parameters). I don’t think local labs in Pune can beat Thyrocare prices.

Quality wise I am not sure, because I was given negative feedback by some people that they dont do proper tests. This can just be an rumor spread by vested interests(read doctors and local labs). Local labs pay around 40% as commission to doctors.

“This year in March, we have done a Rs 350 crore capex and we had a 42% EBITDA. As a company, there was not much of depreciation

or interest and so we could literally get around Rs 90 crore odd as a PAT. This would continue to grow as the business grows. If the

business grows 20%, PAT should also grow 20%. We expect in next three years to have roughly around Rs 400 crore of PAT in hand.”

Am unable to do this math, and get to Rs. 400 Cr from 90 Cr - how is this ?

Do they have a 3-5 year articlated vision of about Rs. 400 cr PAT ? If yes, what is the rough expected share of various business lines ?

Others may find this podcast shares some additional insights especially with respect to Dr. Velumani thoughts about his children, their relationship and how he sees them taking forward the company.

One interesting comment that stood out for me was that, he doesn’t think twice about signing off on any investments into the biz, but he is very wary about signing off on expenditure without due diligence. Not a surprise but alleviates one’e concern about unused cash sitting on balance sheet.

you never know

you never know