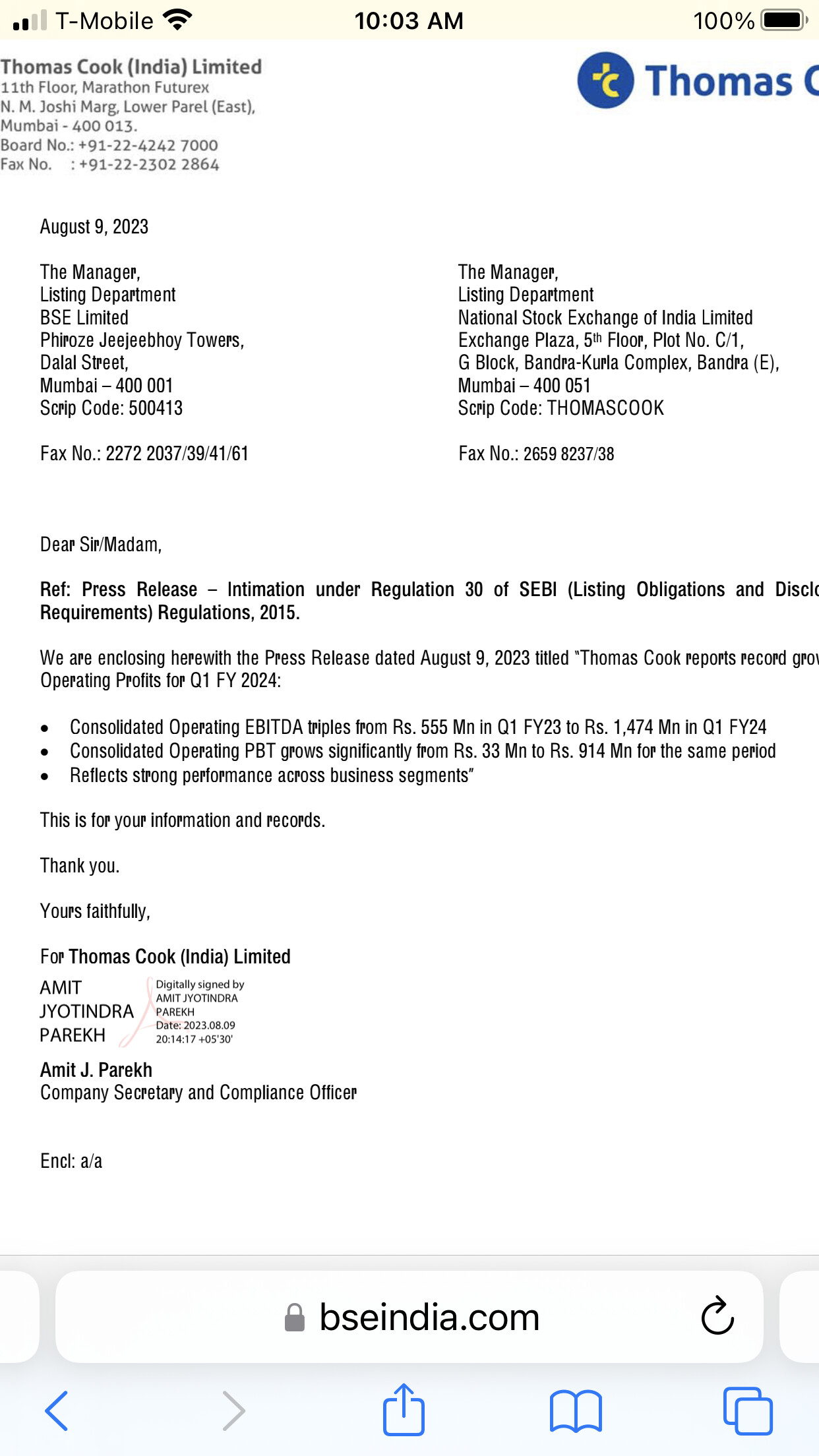

News:

Disc: Invested

News:

Disc: Invested

Nice accumulation of new flow over the last few days - one addition is around Sterling Holiday resort repaying Cumulative Convertible Debentures and extinguishing them. A shift in capital allocation where subsidiary is repaying capital to parent. If this trend is established in multiple subs (and Thomas Cook is home to many) and key shift in capital allocation decision making gets established. Markets generally reward those companies. In the last few days, dividend declared, repayment of capital from subsidiary starts adding some confidence. Can they keep this up?

Discl: Invested

Latest my disclosure: Exited and booked profit last week

I think there still is a long way to go in terms of fundamentals as well as price.

On the OFS & other things of Thomas Cook India.

https://twitter.com/SmartSyncServ/status/1730167254052905367?s=20

I sold Balaji Amines seeing analysis of Mr Bakshi in 2017 at 450, rest is history.

Hi!! I had purchased Thomas cook as a value buy in Oct 21 and the revival in business has played out well for the stock. The overall business has also shown improvement in margins as cost reduction taken during pandemic were sustained post that. The profitability also changed as their acquisitions started contributing to the bottom line.

There still seems to be some room for outbound revival growth, but overall the value proposition in the stock has caught up as it has started trading above it’s long term average valuations. Hence, I was trying to analyse and see if the story is structural and there are any re-rating triggers…

Also analysing if there are any decent moats in the business or supply side dominance which would help them in their journey from here on.

Having said that sharing a few questions that come to my mind, if anyone can help answer those…

Industry…

Travel and travel related business… which forms majority of their revenue is a commodity (hence it’s contribution to EBIT is very low). The only moat businesses like these usually have is brand identity and distribution reach.

And at company level…

At stock price level…

Systematix has coverage on the stock…

Systematix Group TC@IN Thomas Cook India - IC - 01-02-2024 - Systematix.pdf (1.5 MB)

Can someone tell how IDBI Trust sold 38000 shares at just 19.9lacs (i.e Rs.52 per share) on 20th Sept or 10,096 shared at 1.1 cr (Rs.1,124 per share) on 3rd Sept while market price is in range of 200 - 230 in this period? Similar with remaining transactions too

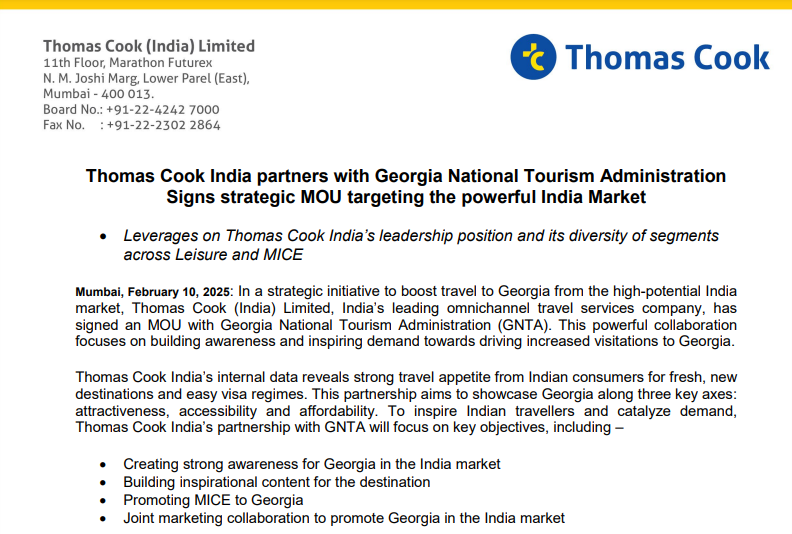

Thomas Cook India has signed an MOU with GNTA to boost Georgia’s presence in the Indian market. Key focus areas: