This is a part of which document. Can you share the link?

Mail sent by Thomas Cook intimating demerged price. Please check your mail from Thomas Cook

Not any document as such. But this message comes up when I try selling the Quess corp shares from my demat a/c online. The shares are reflected but trading is not allowed on them as of now.

Given this cost apportionment is the below calculation for acquired costs of QC and TCIL correct

Assume 100 shares of TCIL purchased at 180.00 Rs ( Total cost of acquiring = 18,000 Rs)

Number of Quess Corp shares received = 18.89

Cost of acquiring 18.89 QC shares = 18000 * 0.2527 = 4548.6

Cost of acquiring 1 QC share = 4548.6/18.89 = 240.79 Rs

Cost of acquiring 1 TCIL share will then be = 180 * .7473 = 134.51 rs

5 Likes

Folks tracking Thomas Cook, may give attention to what EBIX corp (A Nasdaq Listed Co has been doing in India).

Ebix has been on an acquisition spree in India

Weizmann- December 2018

Ebix entered into an agreement to acquire 74.84% controlling stake in India based Weizmann for $63.1 million.

Pearl- December , 2018

Ebix acquired the assets of India based Pearl, a provider of a comprehensive range of B2B and B2C travel services, under the brand name ‘Sastiticket’, ranging from domestic and international ticketing, incentives travel, leisure products, luxury holidays, and travel documentation for $3.4 million

Lawson - December 1, 2018

Ebix acquired India based Lawson, a B2B provider of travel services and international ticketing, for $2.7 million and has been integrated with Ebix Travels’ operations to bring in operational synergies and wider country wide footprint

AHA Taxis - October , 2018

Ebix acquired a 70% stake in India based AHA Taxis, a platform for on-demand inter-city cabs in India for $310 thousand. AHA focuses its attention on Corporate and Consumer inter-city travel primarily with a network of thousands of registered AHA Taxis.

Routier- October, 2018

Ebix acquired a 67% stake in India based Routier, a marketplace for trucking logistics for $413 thousand.

Business Travels- October 2018

Ebix acquired the assets of India based Business Travels for $1.1 million and same has been integrated with Ebix Travels’operations to expand the wholesale travel and consolidation business.

Leisure – July, 2018

Ebix entered into an agreement to acquire India based Leisure Corp (“Leisure”) for approximately $2.1 million, with the goal of creating a new travel division to focus on a niche segment of the travel market.

Mercury - July 1, 2018

Ebix entered into an agreement to acquire India based Mercury Travels for approximately $13.2 million, with the goal of creating a new travel division to focus on a niche segment of the travel market. Mercury’s Forex business will be integrated into EbixCash’s existing Forex exchange business.

Centrum - April 2018

Ebix entered into an agreement to acquire India based Centrum, a leader in India’s Foreign Exchange Operation markets for approximately $179.5 million.

Via - November 2017

Ebix acquired Via, a recognized leader in the travel space in India and an Omni-channel online travel and assisted e-commerce exchange with presence in India, Middle East and South East Asia. Ebix acquired Via for upfront cash consideration in the amount $78.8 million plus possible future contingent payments of up to $2.3 million

Paul Merchants - November, 2017

Ebix acquired the MTSS Business of Paul Merchants, the largest international remittance service provider in India, for upfront cash consideration in the amount $37.4 million.

Wall Street - October, 2017

Ebix acquired the MTSS Business of Wall Street, an inward international remittance service provider in India, along with the acquisition of its subsidiary company Goldman Securities Limited for upfront cash consideration in the amount $7.4 million.

Itz Cash - April 1, 2017

Ebix entered into a joint venture with India-based Essel Group, while acquiring an 80% stake in ItzCash, India’s leading payment solutions exchange. ItzCash is recognized as a leader in the prepaid cards and bill payments space in India. Under the terms of the agreement, ItzCash was valued at a total enterprise value of approximately $150 million. Accordingly, Ebix acquired an 80% stake in ItzCash for $120 million including upfront cash of $76.3 million plus possible future contingent earn-out payments of up to $44.0 million based on earned revenues over the subsequent thirty-six month period following the effective date of the acquisition

13 Likes

The problem with Thomas Cook however is it botched up acquisition of Sterling. This one wont make money anytime soon, and whatever be the purchase price, I cant justify a value beyond say a Sinclairs Hotels.

It cant be compared to Mahindra Holidays because most of mahindra Holiday nos come from foreign subisidiary.

Holiday ownership is a dying business and Sterling is at best a resort co (with some own properties and some asset light)

This will bleed money and we wont be able to justify this stock ever on a PE.

Sterling Land value is 500 crores (basis last revaluation)

The cash cow today is Forex, which I feel is on a downward path sooner or later. Infact there was a twitter update on someone who had visited China and spent entire time without Cash.

Infact I realised recently myself, that I can take bare minimum Forex (for Taxi etc) and complete the foreign trip just on card…Hardly makes a difference. Most of the Holiday component cost is Hotel + Airfare which we anyways pay through Car beforehand.

Food, activities and travel is a smaller component

2 Likes

This is how the Travel Business looks like at EBITDA level

Adjust for 150 Crore of Interest and Dep and Tax of 20 Crores and you are left with PAT of roughly 50-60 crores at best.

Sterling turnaround seems distant. Forex can only go down from here on a longer term basis.

EBIX, Makemytrip will ensure Thomas Cook cant earn big margins in this segment.

So what should be the value of such a business.

At 1500 Crore I might take a chance, at 2500 Crore it looks like dice is loaded against me

5 Likes

Digiphoto imaging services is not counted in above table , any reason for that ? Also there seems to be some cash/float of 1000 crores , if we consider these 2 should the valuation change a bit ?

Please share the source link , Would be helpful.

The Cash has to be adjusted with Customer Liability.Balance cash is towards float, which isnt free cash.

On last concall management had said that their free cash position is roughly 250 Crores only

DigiPhoto is too small as of now…and doesnt look can be very meaningful ever

2 Likes

Very timely post, appreciated by more than 50% within 3 working days. Was very beneficial, thank you

What will be considered as the date of acquisition for Quess in this scenario?

Can anyone decrypt the legalese in this -

The Company has been advised that as per Section 47 (vi) (d) of the Income Tax Act, 1961, in a

scheme of demerger, the issue of shares by the Resulting Company to the shareholders of the

Demerged Company in consideration of Demerger of the undertaking, shall not be regarded as

transfer. Accordingly, Date of Acquisition of Shares of Quess (the Resulting Company) shall be deemed to be the date when the equity shares of Thomas Cook (India) Limited (the Demerged Company) were actually acquired.

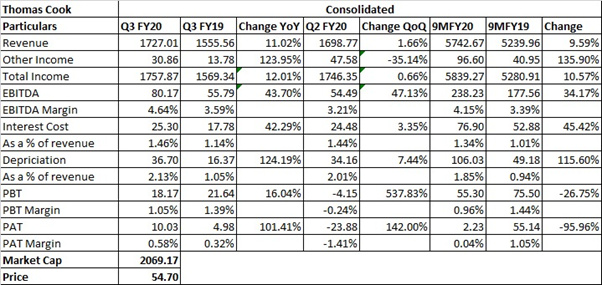

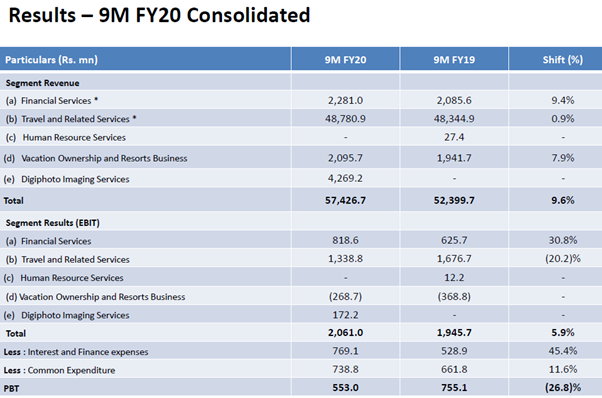

Thomas Cook Q3 Results!

Q3 FY20 IP:

Q3 FY20 CC:

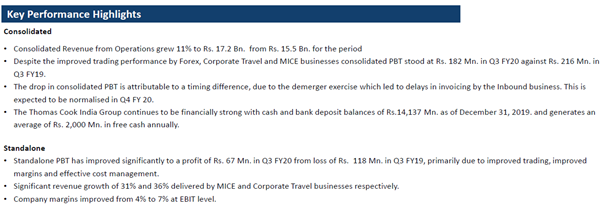

- I believe that the major businesses that is Foreign Exchange, the Inbound Business, Corporate Travel and MICE at a consolidated level did extremely well. And have not only surpassed last year’s numbers but have also achieved our own internal – have exceeded our own internal targets.

- Now in terms of the other metric that we measure very closely internally is the cash balances, the cash in the form of bank deposits and other investments which is at INR 14,137 million as of December 31. And this has generated in excess of our average free cash generation of approximately INR 2 billion.

- I do not believe that the headwinds have gone away. All the news reports around the coronavirus do represent some form of a threat to our business. Too early to tell. But from what little reports I’m getting in from our various businesses across Southeast Asia, there is an impact, and we will have to wait and see.

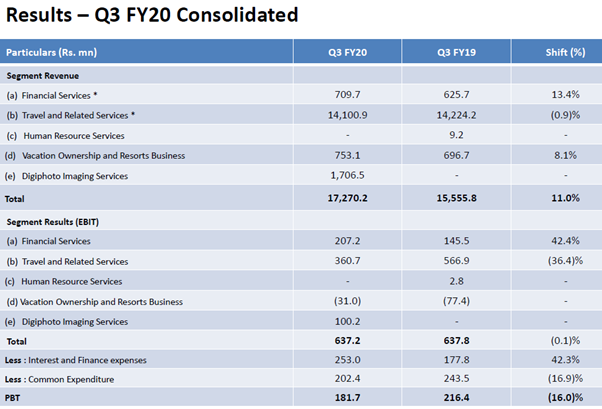

- To move on first to the financial services, I think we’ve had a very good quarter on the financial services side. Our revenue from operations in the financial services side grew by about 13% from INR 625 million to INR 710 million. And consequently, the EBIT on the financial services side moved dramatically from INR 145 million to INR 207 million. This performance is the backdrop of a very strong growth on the retail side where we saw over 14% growth in our top line sales for the retail side. The B2B side of the business which is corporate and wholesale also came out with very impressive numbers registering a double-digit growth close to about 10%. And The Borderless Prepaid Card, one of the fledgling segments that we have actually witnessed over 42% (sic) [47%] growth registering a total volume of $133 million for the quarter.

- Getting to the travel and travel-related segments. As Madhavan said, we had a mixed bag, the B2B side of the business which is corporate and MICE performed very well. The B2C side which is more the holidays on the international and domestic side was a little subdued as you will appreciate that there was this slowness in the economy, the challenges that we spoke about with in terms of the Thomas Cook U.K. shutting down, the C&K closing down, the impact of the negative sentiment in the market. All of that played a little on that side of the business. But despite that, our top line sales on the holiday side grew about 8%, albeit our profitability was a little strained.

- On the Inbound side, we’ll explain a bit more because while you look at the revenue, they represent a flat trajectory. As far as the EBIT on the travel side is concerned, it looks like a degrowth of 36% but we’ll explain that and I will leave that for Debasis to explain as to what that impact is. It’s more of an accounting impact than anything else. But we will explain that in the subsequent conversations.

- As a result, there are some disruptions in the business processes. The business could not carry out this invoice, while the business went on in terms of servicing – getting customers and servicing them, it could not raise invoices on time. There has been some delay during the month – especially during the month of December and some disruptions on payment to suppliers, et cetera, as well.

- Sterling Holidays & Resorts: The [first] quarter. During the quarter, our total income of Sterling rose from INR 675 million (sic) [INR 697 million] last year to around INR 742 million (sic) [INR 753 million] this year, a growth of around 10%. For the second quarter running, we have had an increase in membership sales. So the membership sales – and this is at the total value which was at 21 – INR 218 million last year, is now at INR 333 million, a growth of almost 53%. So for the – even in terms of units, because the membership sales is now because of, as you are aware, Ind AS 115 impact came in from last year. So we can take only 4% revenue in the top line and the balance goes and sits in deferred income. What is relevant is the – the quantum. So even that has gone up from 752 units to 930 units during the quarter. We continue to open more resorts under the management contract scheme which means at 0 CapEx. So we opened 1 during the quarter, 2 more are on the annual during this quarter. In terms of occupancy during the quarter, it went up by – went up to 65% from 63% of the comparable quarter last year. ARRs have been soft for the last 2 quarters. One last time due to disruptions on the rain, and therefore, people canceling. And this time, because of the CAA protest, there were lot of cancellations in the north and east. And this happened in December. However, we have maintained the ARR, the ARR is roughly at the same level as last year. As regards to EBITDA, we are at INR 27 million for the current quarter against negative INR 21 million for the same quarter last year. Now in terms of the 9 months performance, total income is at INR 1,913 million – INR 2,092 million versus INR 1,913 million, a 9% growth, same as in the quarter. Again, the number of membership units has grown by 18.5% to 2,636 units and occupancy is at 66% for – cumulatively for the year. ARR has also grown marginally for the year to INR 4,519 against INR 4,452 last year. As far as the EBITDA is concerned. For the 9 months, we are at a negative of INR 5.2 crores as against INR 17.7 crores negative last year. That has improved. In sterling, they are recognising costs upfront and revenue will be recognized as and when it will be generated so there is Negative PAT.

- Interest Costs: So on the quarter numbers, if I sort of do a deep dive on the interest cost, interest and finance charges and do a like-for-like comparison, you’ll see that the operating interest, actual interest cost has moved up from INR 61 million last year to INR 77 million this year. And I’ll come to the reasons of that separately. The other finance charges which are primarily bank charges, credit card charges, cash management charges, have moved up from INR 116 million last year to INR 129 million this year. And there is a new element which has come in which is the interest on lease liabilities. Now this is INR 47 million. Now this is – coming out of the new accounting standard Ind AS 116 which came into effect from 1st of April of 2019 and which basically reclassified the lease rental payments into 2 parts, it’s into the depreciation and interest. Now that interest comes and sits here. There is no – this was not there, obviously this was not there in the last financial year. And that’s why the numbers are disparate. As far as the interest cost, I also – we also (inaudible) the interest costs going up from INR 61 million to INR 77 million. And that’s primarily operating interest in – operating a large part of that, out of that INR 16 million, the major part of that, about INR 12 million out of that is on account of the new subsidiary that we have which is DEI, the one that we acquired on 30th of March. And INR 4 million is – the balance is in the other subsidiary which is not a big number anyway.

- Debt Structure: Quess as we have moved out of – Quess has moved out of our accounts for the last 2 years or so. So the debt that we see on our balance sheet-- first of all, at a net debt level, we are negative debt because the cash and bank balances exceed the debt. At a stand-alone level there is no debt. However, there is debt – debt in the subsidiaries. And the interest cost is on account of those subsidiaries, largely. Now each unit is – each unit has its own working capital requirements and therefore has working capital loans. And that’s where the loans are coming from.

- As far as Digiphoto is concerned, I think we have had a very good quarter, despite all the challenges, like as we mentioned on the call. This is a business that operates across the globe with Far East and Middle East being a big market. Middle East has been going through a bit of a slowdown. But despite that, they had a very good performance. They acquired some new sites (inaudible) which is effectively the Dubai Frame, the Dubai Aquarium and the Dubai Ice Rink. They got some 2 large contracts in the Atlantis, which is the Atlantis Bahamas and the Universal Studios Beijing. So from a pipeline point of view, that total acquisition or new contracts that they have inked in the last quarter, that will runup in the full year of FY '21 is close to about $40 million. So that’s the new pipeline of businesses that have got. For the current quarter, which is Q3, on a comparable basis, their volumes actually went up by about 7%, 8%. And profitability improved by about the same percentage. This, despite the challenge that we saw in parts of Hong Kong, which was the unrest that we had and in parts of the Middle East. Despite that, they had a very strong performance. Just to give you some metrics around their performances, the number of partner addition actually moved up from 115 to 137, the number of sites that we operated last quarter was 227, this quarter is 257 and number of transactions was 1.56 million, which went up to 2.5 million. So this are some of the metrics. So effectively, it was a decent quarter for them. And we’ve been running on the expectation that we have put up for the business that – when we acquired. So for the current quarter, the profitability in terms of a [metrics] was about INR 10 crores. And I think it’s kind of trending on line of expectations.

- Summer Bookings: So currently, it’s a little too early to comment on the forward bookings. And I’m saying more specifically because if you look at it, we operate 3 brands on the outbound space. Obviously, I’m going to keep the Hong Kong operations out of it but we’ve got SOTC and Thomas Cook, the 2 brands that we operate on this space. You will appreciate that we had the news of Thomas Cook U.K. coming in the last week of September. Hence, we delayed our launch for the summers whereas SOTC went ahead with its launch early in September itself. So from a pipeline point of view, our pipeline started a little later as far as Thomas Cook is concerned but as far as SOTC is concerned, it started much early. From a view at this point in time, for Q2, which is calendar Q2 for FY '20 which is the peak of the summers, our forward bookings are almost like 7%, 8% growth over the previous year at this point in time. Albeit, we have seen, as Debasis mentioned and there was a question in this regard previously in terms of average transaction value. We are seeing some change in patterns as how customers are traveling, they are preferring the more shorter product, the shorter format of the product, as a result of which the ATPs are impacted but the silver lining there is that people are taking more frequent holidays. So we’ve got – getting the same customer travel with us a lot more. And that we believe is far more sustainable. So the big – answer to your point is we are seeing about 7%, 8% growth for Q2 at this point in time.

Disclaimer: Tracking

3 Likes

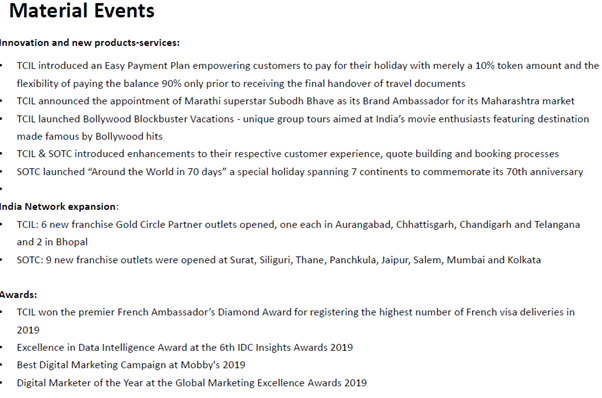

TCIL has posted a recent interview with their MD. Interview is fairly comprehensive.

Link below.

https://axis-capital.kpoint.com/kapsule/gcc-c3c62860-76af-4618-b321-c1cf0606682e/nv3/embedded

Furthermore, two day ago TCIL announced that the board will consider share buyback proposal on 26-Feb-20. Let us await the outcome of that meeting.

Disclosure: Invested

3 Likes

Update on buy-back:

TCIL has announced the buy-back of 2,60,86,956 Equity Shares (being 6.90% of the total paid-up equity capital of the Company) at a price of Rs. 57.50.

The aggregate amount (Buyback Size) will not exceed Rs. 150 Crore.

The promoters will not participate in the buy-back as a reflection of their confidence in the Company’s growth prospects.Currently, promoter stake is 65.6%. This will increase to 70.46% post buyback.

Hi, I’ve just started reading about how to invest and wanted to discuss a bit into Thomas Cook India.

The stock has fallen since Sept’19 due to poor quarter(s) and the management says it is mainly due to negative sentiment among travelers due to shutting down of cox and kings, slowing down of economy, increased airfares and now, the coronavirus.

However, the fundamentals seem unchanged (please correct me here if I’m wrong), the management is good and the stock is being offered at a steep discount (even less than the book value).

I believe once people start traveling again (maybe 6 months, maybe a year) after the virus subsides (hopefully) and I understand it does have some risk, but I believe it might be a good opportunity to invest at this moment.

Would love to listen to experienced investors/people following the stock.

Disclosure: Not invested

1 Like

The other issue with this stock is that analysts find it difficult to value.

Part of the reason for stock being down since Sept is the demeger of Quess Corp - one of their investee companies

1 Like

Buyback announced and Fairfax not participating -shows management confidence. Valuation very attractive. You can view it as paying only for Sterling resorts and getting other verticals for free. But how soon it will turn around in current situation is anyone’s guess.

2 Likes

If we believe in -

(1) “This too shall pass scenario” - people back to normal life and want to enjoy life after lock-down.

(2) Market leader will eat market shares of other small players - small players finding hard to survive due to their financial and technological limitations

(3) Cash is king - TCIL is net debt free company compare to other small companies. Cox and King already died leaving market to TCIL!

(4) After COVID-19 people will be more focused on quality compare to cost - willing to book travel with company having good quality control and hygienic services

(5) Being operated locally but has global market reach - Network effect to play to capture maximum travelers across the world.

Short-term Pain but long term gain scenario for TCIL currently !!. When blood on street who has courage to buy the stock!! When others are fearful be greedy!

Disc - started buying @25

3 Likes

The company had planned a buyback @ 57 before lock-down. Has anybody received any updates on that?

3 Likes