Excellent set of numbers from Thirumalai chemicals. Should continue to do well in coming qaurtes as well. Add this to the advantage of anti-dumping duty on chemicals used in plastic, IG Petro and Thirumalai should do well

Disc: invested

The ADD Final Findings document has a lot of interesting relevant data points about the business and sector in general.

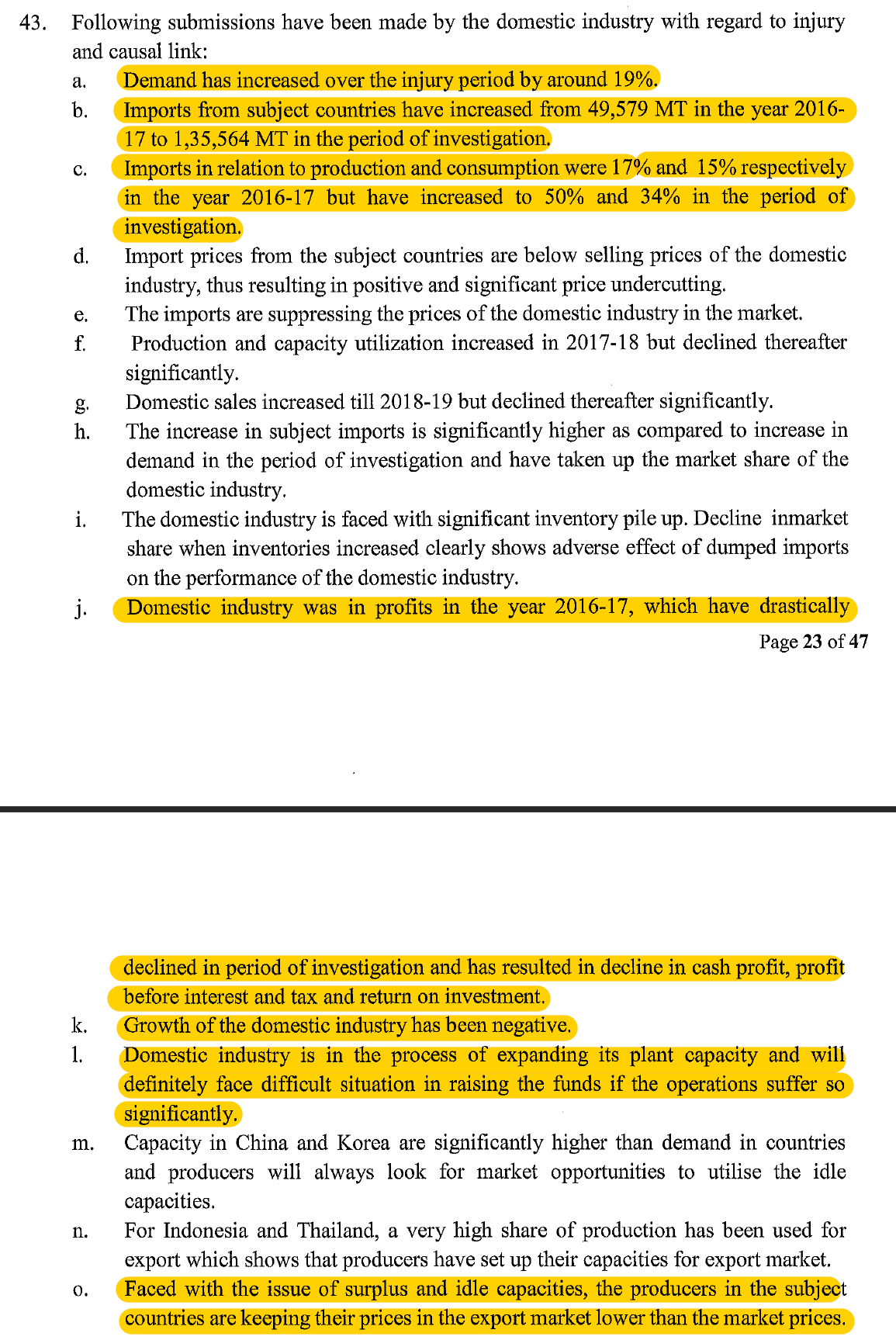

This part shows how the domestic manufacturers Thirumalai and IG Petro have suffered due to the dumping

Though the domestic consumption has grown, the domestic industry hasn’t gained from it and sales has been flat.

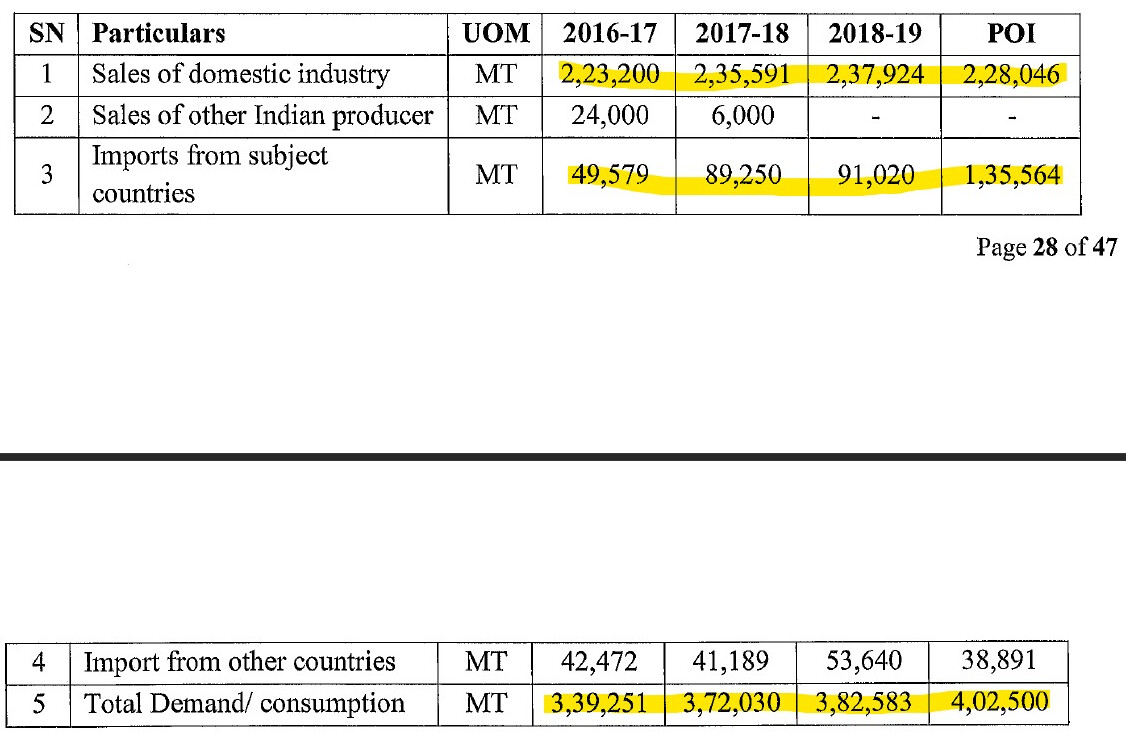

And the domestic industry has lost market share

This could all change with this duty being imposed which appears to be anywhere from 5-15% depending on the country (Towards the end of the document).

This will let the domestic players run their capacities better, capture lost market share and also have better margins for the same. I think about 20% growth in topline is possible with the ADD in place and margins as well could be in the 25% range

8 Likes

Hi @phreakv6 , if possible please share reason for margin expansion? Is it due to increase in end product price or decrease in raw material or reduction in other expenses . What are the pointers to track to anticipate trend of this quarter and next quarter results

Hi,

This is essentially a commodity play right? So its fortunes largely depend upon 1)raw material price fluctuation, 2)industry capacity utilisation 3) dumping from external sources as suggested by you.

Although crude prices are on an upward trajectory, Phthalic Anhydride prices are also increasing according to price index data from eaindustry.nic.in.

I have 1 question I’m trying to understand.I hope you can help me with it.Margins of the company and also of IG Petrochemicals have increased tremendously from Sep20 quarter.What can explain that?

Thanks

Recently govt levied ADD on PAN , which helped domestic industry to regain lost market share in PAN, previously without ADD china dumping PAN in india very very cheap price. With ADD coming into picture these players start regain mkt share

This is just a recommendation, right? The final decision from the dgtr has not been released as of yet I think… If someone has the dgtr official document which has the details of the anti dumping duty, please share

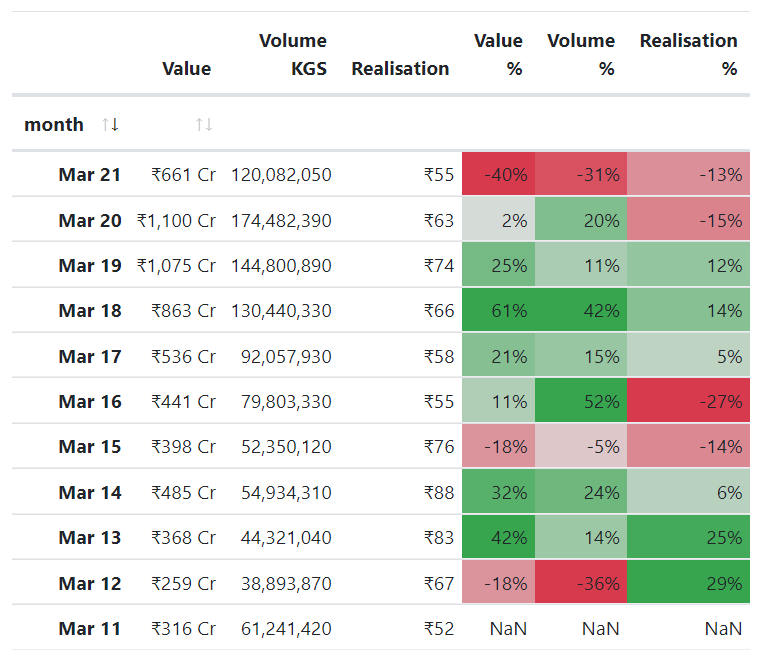

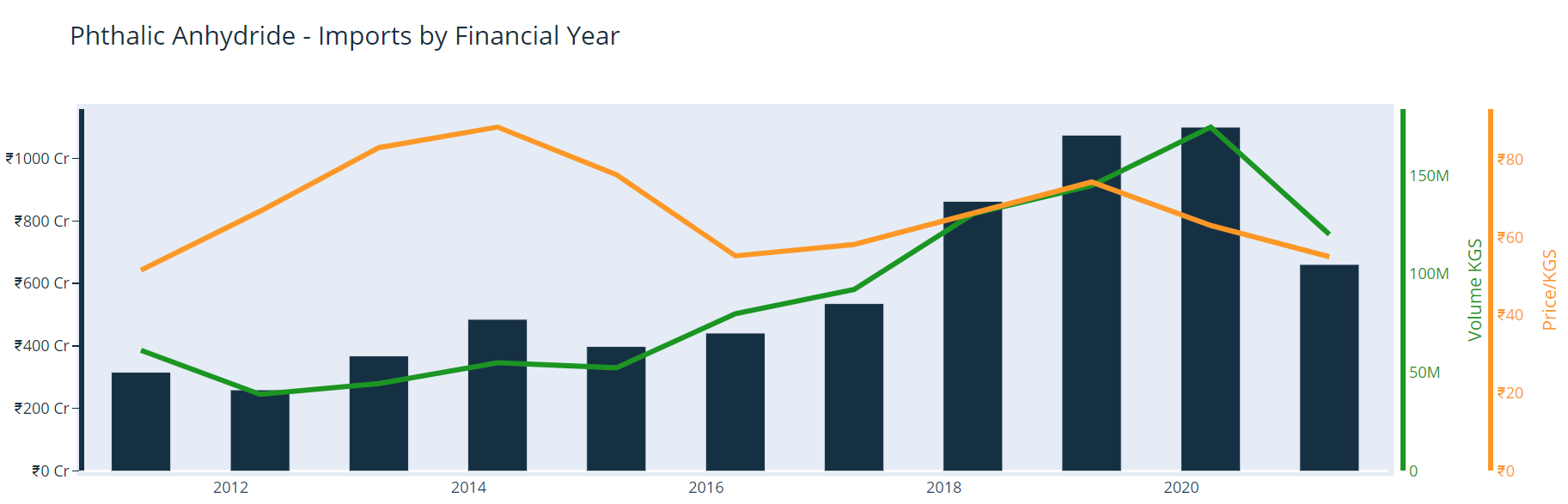

I believe this is mainly due to reduction in imports. This is how the imports look until FY21 (Mar '21 is not included). There is a 31% drop in volume imported. This volume has grown consistently in the last 5 years otherwise.

Even with increased imports, if the import prices were above 65 levels, the margins of domestic players have been good (15-20% range at EBITDA level in FY18 and FY19 for eg.).

Of course imports and dumping is only one aspect of what can get the business good margins (albeit a very important factor). The other factors are o-xylene (the main RM) and PA spreads, demand (paints are a big driver of PA).

Yes this is a simple commodity business but its a duopoly. The main competition is outside the country in Korea, China and Indonesia. If that competition is kept out, the domestic players will churn out 25% EBITDA margins and with the capex done recently numbers can be better than in the past. There may be lot of other nuances but this is the big part of it. Of course valuation matters as well, at current valuation I believe a lot of it is not priced in.

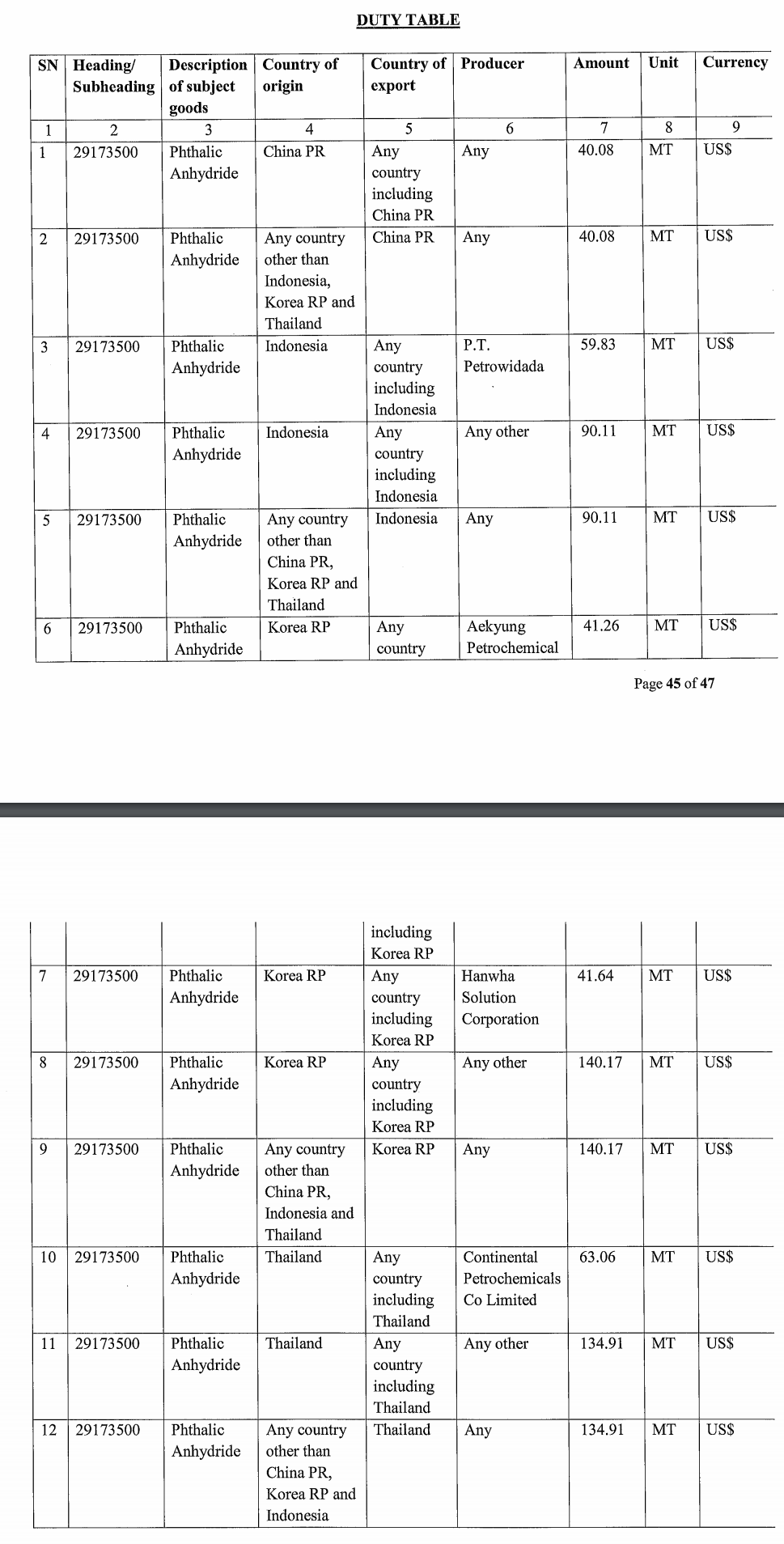

This is the Final Findings document. The duty table is here. Am not sure from when it will come into play though.

6 Likes

Usually post the Final findings document is out, the official document on imposition would come within 30-60 days… Both thirumalai and igpl in a pretty sweet spot as of now

The reduction in imports does indeed explain the increase in margins of domestic players. But ADD is being imposed now,I wonder what caused the reduction in imports then.That answer is one factor in determining how sustainable the increased margins are.The ADD is highly welcome considering the tremendous rise in imports.This does have the promise of a very profitable cyclical play.

Not to bother you,but how can I get the import data and realisation like the one you shared above?Data organised in this way helps a lot in understanding the competitive dynamics especially of such cyclical industries.

Thanks a lot

This my own tool and its not public. I think screener and tijori also provide this information so you can check those.

1 Like

FY21 AR is out

My notes

- Dahej commissioning significantly delayed because of shortage of manpower due to Covid lockdowns and delays in delivery of material.

- Dahej project is ready to be commissioned in the near future (Safety and commissioning checks done)

- Dahej total capacity will be 210k MT of PAN, Fine chemicals and Derivatives (Bulk of this capacity though is still in design phase and what’s ready could be only a part of it)

- Ranipet plant modernization helped in better utilization and margins (better quality, reliability, safety and energy use)

- Demand is good and expecting significant bounceback after present Covid wave

- ADD yet to come into play and import of PAN is at all time high. Implementation of ADD Final Findings (duty imposition) is delayed as critical govt. departments in Delhi are slow due to Covid. Company is following up actively to get this done soon

That’s the parts I was interested in as these are what’s going to drive numbers going forward.

Disc: Invested

7 Likes

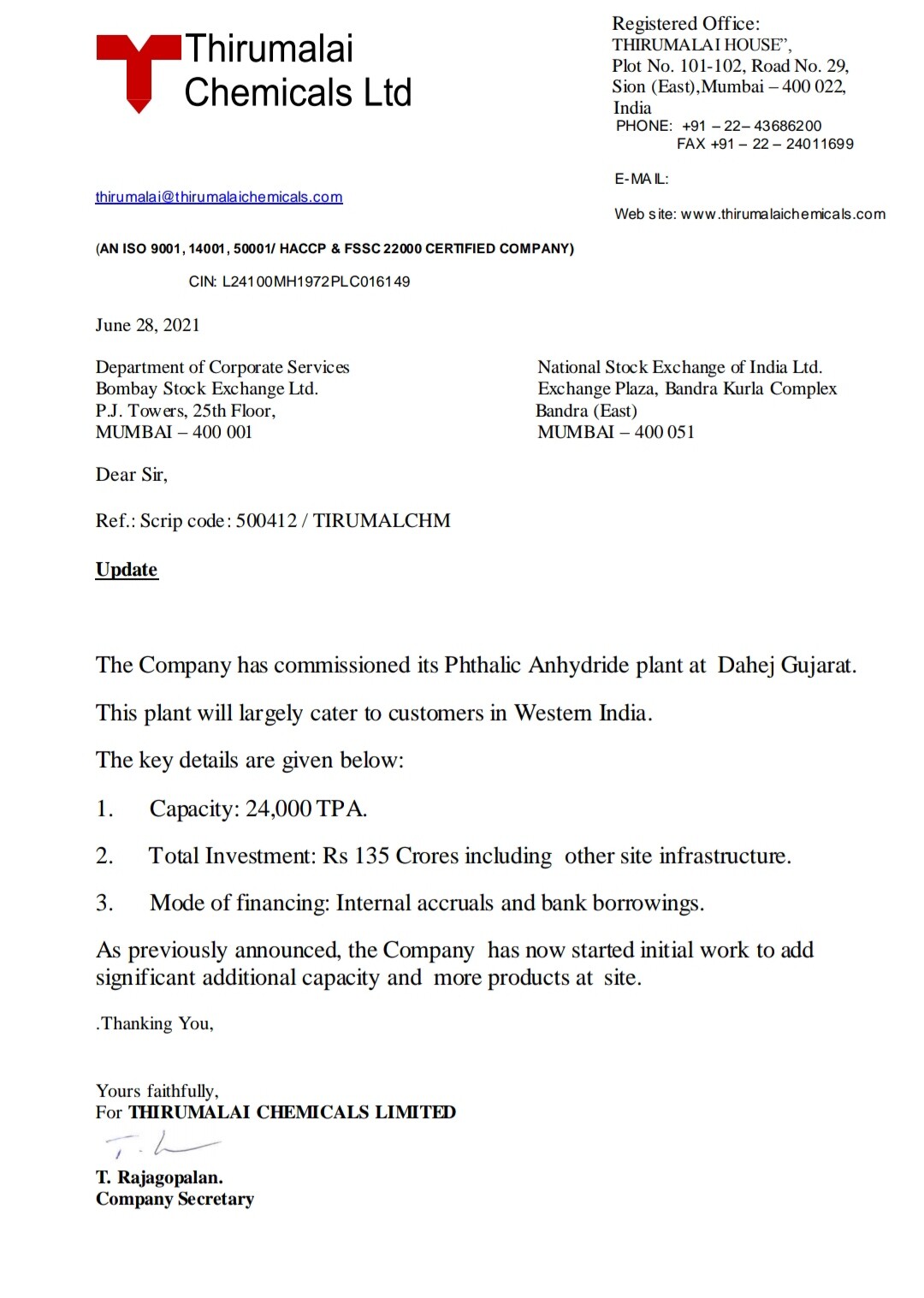

Hi @phreakv6 . Dahej plant for Pathalic Anhydride commissioned.

4 Likes

Took 3 years to finally commission it - let’s hope the logistic cost come down now

1 Like

My Thesis:

World over smaller companies having 50-60k MT capacity have closed down during last 10 years . Same has happened in India and now Business has become duopoly which may over a period of time lead to an advantage.

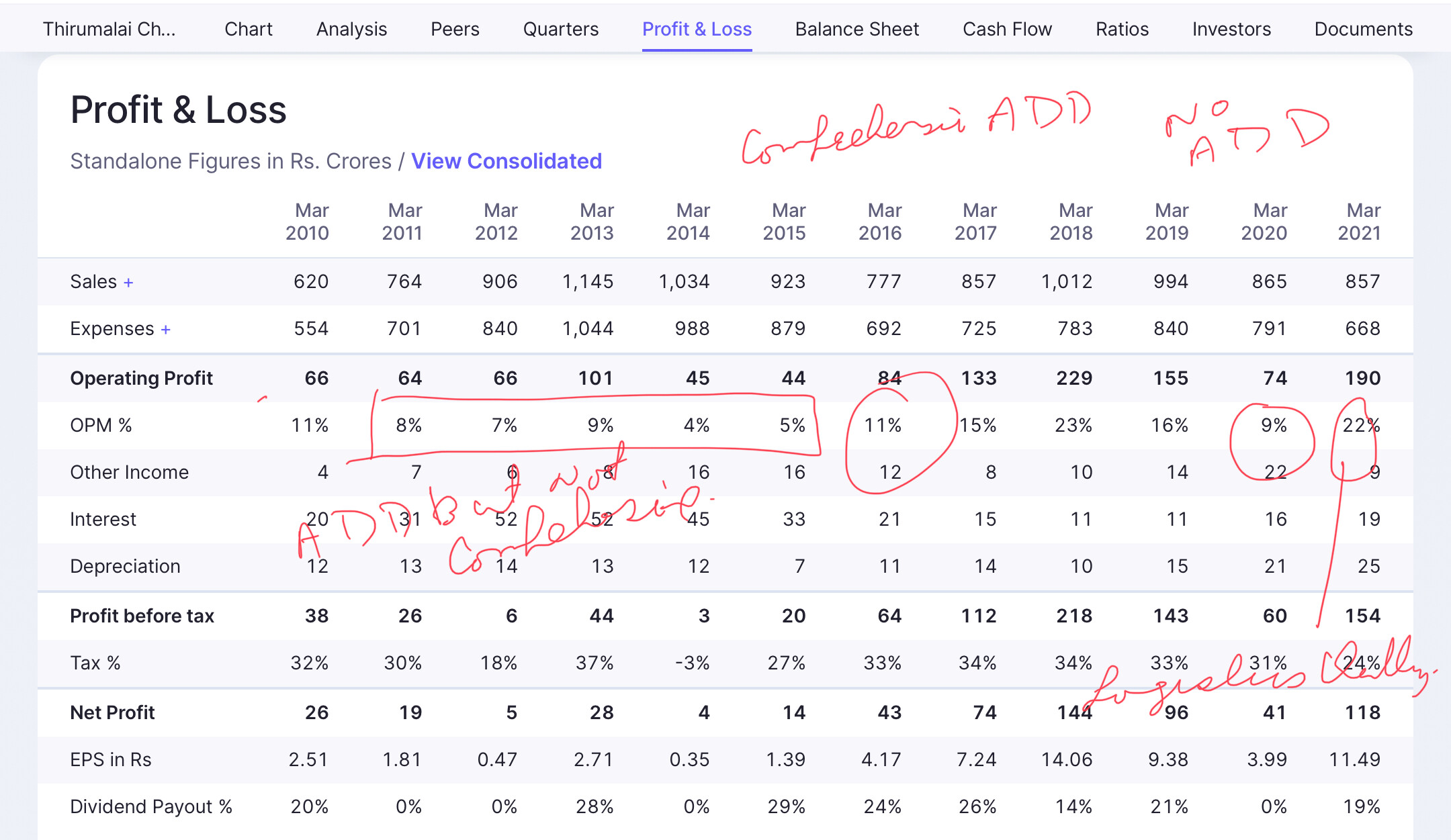

Anti-Dumping Duty (The only Truth) - Dumping happens at Thirumalai’s level as well the products, which are made by the customers. From 2009 till 2021 Thirumalai has done well whenever there is comprehensive ADD (covering all the culprit countries). It was mostly in 2010 and between 2015-2018. The question is how has Thirumalai utilized the money earned during ADD period.

Raw-Material: RM prices follows either crude or if there is artificial shortage due to production of OX shifting to Para – Xylene. Thirumali has no pricing power and they are not able to pass the RM price increase. Another challenge is that when OX price geos down, customers stop buying because of fear of inventory loss. This has happened at least twice in last 11 years.

Operating Skills of the management: Negative Working capital. In 2011 Debtors were 25% of sales. In 2012 they decided to reduce business on credit. In 2021 Debtors has come down to 6% of sales. Inventories will come down significantly, as they scale up in Dahej (80% Customer and 100% RM source is in western part of India). IG Petrochem still has 14-18% of sales with Debtors

In spite of various challenges like Higher power costs due to old plant or higher Inventory due to location disadvantage, Thirumalai has shown better ability at managing the operating business.

Some of this is getting addressed as they have modernised the TamilNadu plant (which will lead to more than 20 cr of savings in power cost and better efficiency wil lead to higher production/sales) and Dahej will help in reducing logistics cost and inventory. All these will directly flow to flow to Cash Flow and bottomline.

| Average of 5 years | IG Petro | Thirumalai |

|---|---|---|

| Debtors (%of sales) | 14% | 8% |

| Working Capital (% of sales) | 7% | 2% |

| ROIC | 36% | 62% |

| Gross Margin | 32% | 34% |

Capital Allocation Skills: Management seems to be prudent. They take time to decide (may be sometimes too slow). WHen they were not able to make money in MA business, they clsoed the plant for 3 years. Sales suffered but prudent was to shut down temprorialy. When Malaysia was not performing, they took charge on the books.

Coming back to the question of what has happened with the CASH. They took the profit generated during ADD and modernised the TN plant and undertook Greenfield Dahej plant. This time they are nimble. Upcomming ADD will help with cash and they are expanding in USA and Dahej. Over a period of time profit from ADD will help them gain scale, geographical reach and new capabilities in adjacent businesses. Even partial success may change the dynamics of the business (similar to NOCIL)

Optionality: Malaysia and US can change the trajectory

Concern:

- Large Expansion By IG Petro and Thirumalai. Unless the majority of the capacity is used for the downstream projects it may create supply glut. India Needs comprehensive ADD for many years to be able to absorb this capacity

- Sources of Fragility: The profitability of the business is totally dependent on the Government. This is being addressed through downstream business. No pricing power and no control on RM

- Next Generation - The new MD has to show the hunger to grow while being prudent. In the past Thirumalai has been too conservative but it seems that’s changing now under Ramya.

- Single Location Risk: With new plant in Dahej and subsequent expansion, risk arising of single location with be mitigated.

Levers of growth: 1. Market expansion (In the current line + new usage of PA) 2. Volume captured from import 3. Better pricing and margin due to downstream products and scale 4. US and Malaysia business

ADD and RM will always create opportunities to enter at lower levels and make money during the better years. Due to Duopoly structure, increasing PA demand, the Trajectory of business may change with scale and downstream products – but this has to be seen.

Thanks, @phreakv6 for your wonderful analysis which helped me get started.

Disclosure: No Position. Interested

16 Likes

Excellent results posted by the company.

4 Likes

Very good Q1 numbers reported by Thirumalai.

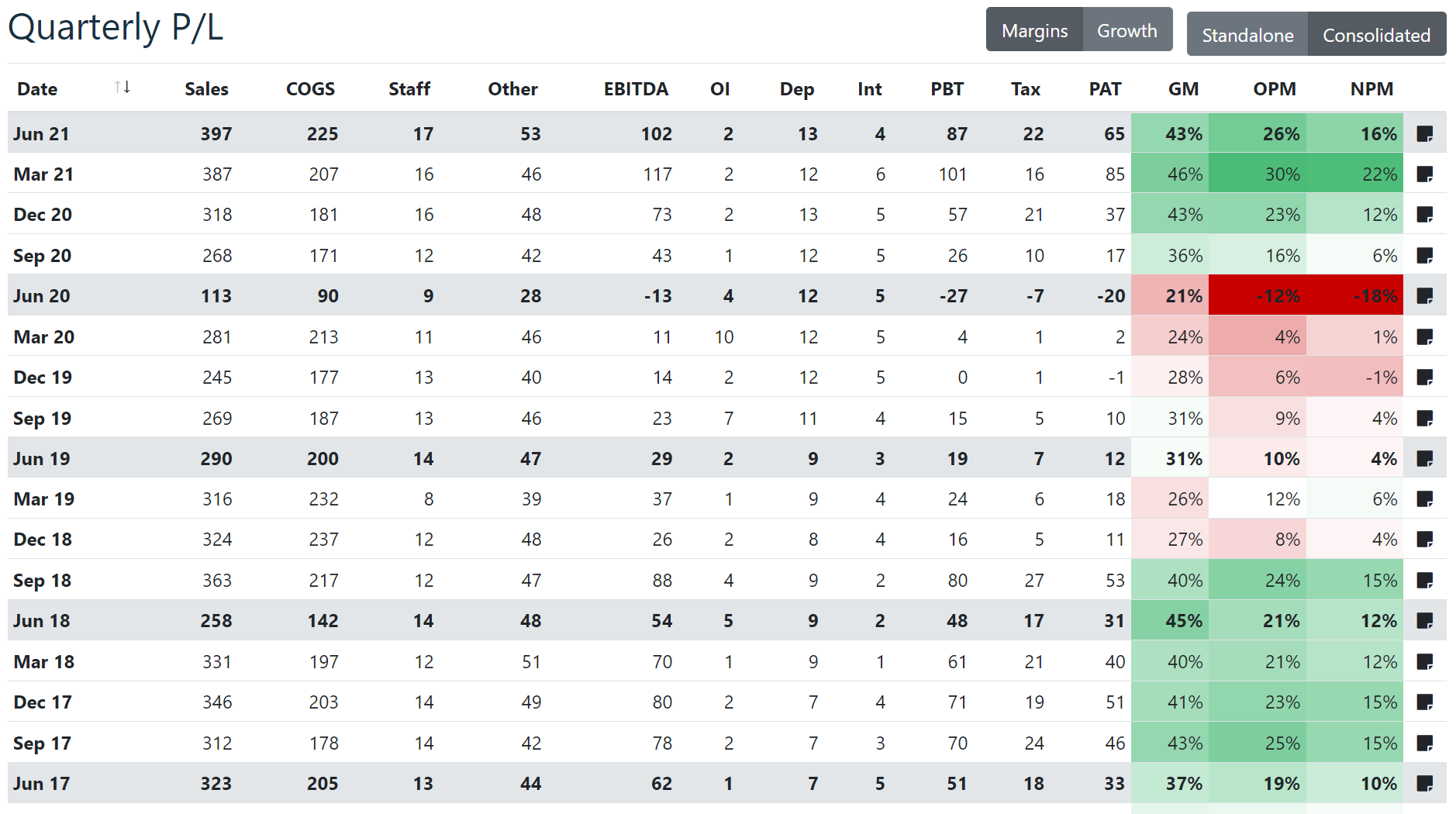

Some observations

-

Topline has grown despite lockdown - Could be because the end-use industries Paints and PVC pipes are both doing quite well

-

Company had mentioned in June (in the FY21 AR) that dumping was still high in Q1. Same can be seen in import data as well for April month (31% higher imports by volume and 59% by value YoY). This could have lead to some pressure in realizations - Otherwise margins probably could have been 30% like Q4

-

Though gross margins are similar to CY18 levels at around 43%, the operating margins are higher by about 300 bps on average in the recent two quarters. This is probably due to revamp and modernisation of the Ranipet plant. The management had mentioned this multiple times in last year and this year’s AR. Power and efficiency improvements seem to have lead to about 300 bps improvement is my guess

-

Going forward with the Dahej plant, another 300 bps in margins can probably be saved in logistics cost

-

Without dumping when ADD comes into play fully, hopefully in Q2 (management should clarify in tomorrow’s AGM) and with Dahej starting to contribute, the margins should be in 30%+ levels.

-

With TTM EBITDA of 335 Cr and TTM PAT of 204 Cr, currently its trading at 5x EV/EBITDA and 9x P/E which still offers very good value considering the capex contributing, ADD, logistics cost savings and sectoral tailwinds with PVC and paints demand. TTM PAT is already at ATH (204 Cr vs 170 Cr in FY18) while price is about 45% below ATH

UPDATE: AGM Notes

- About 150k is the current capacity. 200k capacity planned in two phases of 100k each - 1st phase will come online in 2-3 years

- Though underlying commodity is volatile - the management keeps an eye only on end-use demand volumes (which are growing) and margins

- Most production and demand is just-in-time due to volatile nature of commodity and people don’t want to take stock losses

- ADD customs notification should be coming in next few weeks

- Dahej plant will help in exports to Europe and middle-east. It was hard for them to export to these markets from South India due to logistics costs

- Dahej plant will produce PA, MA and food ingredients

- US subsidiary (wholly-owned) will commission 40k MPTA Maleic Anhydride plant. This plant has a logistic advantage so will have adequate RM cheap RM supply.

These were the pertinent points I found interesting, so I may have missed a lot of other information.

Disc: Invested

28 Likes

48th AGM Chairman’s Speech.

2 Likes

I couldn’t find any comments on the Dahej plant, any idea when will it start contributing to the topline and bottom line?

Company commissioned Dahej plant on 28 Jun 21… update was provided by the company on Bse…

1 Like

Management talk with CNBC-TV18.

Highlights:

- Healthy outlook due to demand in paints and construction sector in general.

- Q1 is representative of EBITDA margins and EBT margins. Company will continue to deliver similar to Q1.

- Current Capacity utilization is 90% plus. About 15-20% increase in capacity due to new plant at Dahej and debottlenecking.

- About 70% increase in capacity in next 3 yrs, 140% increase in next 5 yrs in India. Have sufficient demand for these capacitites.

- Biggest speciality chemical capacity addition is ongoing in US through subsidiary. The largest speciality food ingredients plant based on shale gas will be onstream in 2 years.

- About 800-1200 Cr. investment is planned and 60-70% of it will be from internal accruals.

Thanks!

9 Likes