Hi Dhvanit in your portfolio you have significant portion allocated to shri balaji valve ltd. I am researching this company for quite sometime. I am trying to figure out their clientele, but could not find any information. Do you have information regarding who their clientele are and what portion of their revenue is represented by top 5 or top 10 customers?

2 Likes

Apart from the RHP, there is no information regarding the customers.

In the RHP they haven’t provided in any information with regards to who are there customers.

Concentration is as follows:

The data here is of prior periods and it may have changed post listing.

Also, it is highly unlikely that any information will be provided in the Annual Report.

The only way to obtain the information is through meeting management in AGM or through mails/calls if they agree.

3 Likes

Signature of Peak Bull Market,

It was hard to believe at first, But this guy with single Yamaha Showroom in Delhi went for an SME IPO, looking to raise 11cr … Next what The IPO got the bumper oversubscription- 100 times.

Indian Markets Hit Fever Pitch as Resourceful Automobile’s IPO is Oversubscribed by 200x Despite Negative Cash Flow Automobile sought ₹12 Cr, received ₹2400 Cr. Operates 2 Yamaha two-wheeler showrooms under the brand Sawhney Automobile. Despite two years of negative cash flow, the grey market premium soars over 70%. Have you heard of the PP Waterball story…?

18 Likes

@Dhvanit_Merchant17, @kdjolly, @DocDhiru

While the SME arena is hyperactive, updates, ideas and musings from our prolific contributors have been much muted. Request you all to pl share your experiences of the last 3 months and how you see the SME space faring in the coming months.

Disclosure : started investing recently in SMEs, with interests in TAC info, Z Tech, Supreme Power and Shivalic Power cont.

Majority of the SME spacd is now in overvalued category now. Even broad markets are also trading at relatively higher multiples and the base (reported earnings) itself is on historic highs.

The market and people are just factoring any and every positive update for the companies and good amount of scripts are trading at forward PE rates which are expensive even at FY 26/27.

Plenty money is pumped everywhere and apart from the March 2024 earnings, elections and budget hiccups; whole space is on an one directional journey to the moon from March end.

The SME space do provide opportunities but the risk at the moment is now at its highest levels when looking in the past 4-5 years. You can also measure it by the frequency of the SME IPOs and the oversubscription in those.

Note: I have made a base of 10% cash holdings since last 2 months and do not intend to use it until sideways/bearish sentiments occur on fortnightly basis.

Present view: Hold or sell

Disclosure: Currently I am not holding any of the stocks mentioned in your post.

4 Likes

SME IPO is approved by exchanges, not by SEBI, due to this such Yamaha dealer IPO / tiny hospital in Bharuch etc got approved for IPO.

3 Likes

3 Likes

Anyone tracking K2 Infra? Looks good at current valuation.

It looked good at current valuation but after the annual report, there is some traction and promotion going on in social media platforms, so be a little skeptical about it.

I went through RHP and AR today and concluded that if executed as per targets, the company is indeed cheap on valuation front. On receiving 33 cr order from railways 2 weeks ago, the company mentioned 477 cr orders to be completed within 15 months.

The management is decent, customer concentration is bad as 60-70% dependent on Vindhya Telelinks under Jal Jeevan Mission.

The business has also changed a bit in FY 24 vs FY 23. FY 23 had higher margins and 36 cr from services while margins cooled down to industry levels and sale from services fell to only 11 cr. As per concall PAT would be between 10-13% which is in line with FY 24 margins.

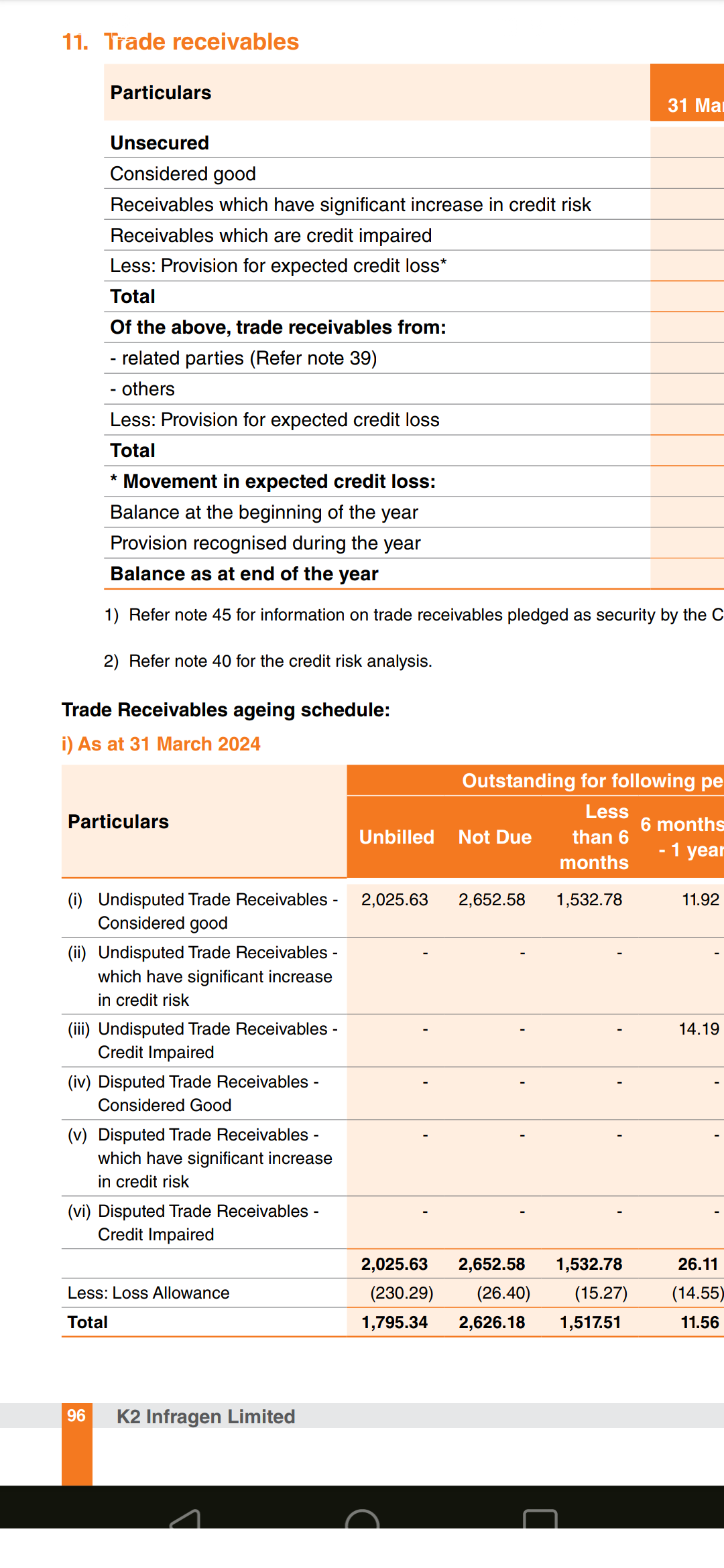

The company follows IND AS and is aggresively providing for credit loss allowance which is strange for a small SME company as there is no tax deduction available. In 2 years they have provided 6.5 cr worth of allowance. They are deducting it from trade receivables, so any moment on opposite side cannot be determined. Meanwhile they are also providing for bad debts and not adjusting it against Bad debt reserve.

One strange is this:

The company is providing loss allowance on unbilled revenue. This makes no sense to me. Why to book revenue and anticipate loss when it is not yet billed?

As mentioned earlier, company is at a good price if execution is done with stable margins. If that is to happen the movement of trade receivables will be the only concern atleast for H1 & H2 FY 25.

Disc: Under watchlist

10 Likes

Thanks for the detailed response. Have taken a position, hope the management delivers.

@Niraj_Punjkaran will share my portfolio and input very soon.

2 Likes

SME Holdings as on 13/09/2024:

| Stock | Cost % | Latest % | Avg Holding Period |

|---|---|---|---|

| Qualitek Labs | 10.53% | 15.77% | 58 |

| Holmarc | 15.08% | 14.76% | 198 |

| Trust Fintech | 12.06% | 12.84% | 43 |

| K2Infra | 14.35% | 9.04% | 9 |

| Aurangabad Distill | 6.04% | 8.56% | 351 |

| Chaman Metalics | 6.42% | 7.51% | 193 |

| Vision Infra | 10.02% | 7.36% | 1 |

| Delaplex | 10.27% | 6.42% | 12 |

| Knowledge Marine | 1.08% | 5.78% | 767 |

| Bondada Engineering | 8.32% | 5.61% | 15 |

| Kotyark Industries | 2.60% | 4.07% | 599 |

| Tanvi Foods | 3.22% | 2.29% | 1 |

The average holding period for Qualitek, Holmarc, Trust Fintech and Chaman Metallics is lower than actual due to tax harvesting. In all 4, I have entered on the day of listing and later on bought and sold.

Thesis for new additions:

- Qualitek Labs: Companies with 20%+ growth guidance for next few years - #213 by Dhvanit_Merchant17.

On top of the mentioned post here, the company is operating cash flow positive and has been investing significant amount on setting up their labs.

Their Fixed assets have increased from 14 cr in FY 23 to 30 cr in FY 24 (majorly capitalized after RHP date, i.e. after Jan 24 and before Mar 24) and is further expected to be at 42 cr in FY 25 (30 cr + 7 cr WIP + 5 cr from IPO funds).

Once they achieve operational efficiency in their newly established labs, it will act as a significant boost in bottomline PAT, although it may take 12-18 months to achieve that.

- Trust Fintech:

The company is into CBS software for co-operative banks in Maharashtra and is slowly adding new banks under its clientele. This provides a one-time decent revenue and a longer-term revenue for maintenance, bugs and updates since changing CBS for banks is a cumbersome task.

Moreover, from IPO funds they are developing CBS and LOS software for North America and Latin America. This may or may not work but their domestic revenue is enough for them to sustain and any revenue from these markets will boost their top line.

Recently, the company has also won small order from Indian Bank. This is a one-time order but they have started tapping the PSBs.

Investor Presentation:

TRUST_13082024111802_NewIntimationtoNSEInvestorMeet130824.pdf (nseindia.com)

H2 Results:

Company heavily capitalized their employee expenses, resulting into decent Profit and Loss. Had it been not capitalized; the company would be at nil profits. Moreover, they will continue to capitalize it in H1 FY 25 also.

Peers:

They have considered NPST and Veefin as their peers, but Trust’s customers are completely different from NPST and Veefin and also Trust do not have heavy tech implementation comparatively and thus do not command the same valuations as its peers and might never will.

- K2 Infra:

This company was in my watchlist, and I recently bought it after going through it’s AR and RHP. The thesis solely depends on their ability to execute their order book which the management has given timeline of 15 months.

Further: The SME portfolio - #110 by Dhvanit_Merchant17.

The valuations are overvalued, and the execution of the order book will dictate the valuations and price of the company.

- Vision Infra:

Proxy to NHAI capex. The company is into renting of road equipments. Having reviewed the RHP, the company looks decently valued amongst its peers.

The negatives here are high debt and the profit arising from sale of fixed assets. It constitutes more than half of its PAT which is very high considering the nature of the income being one-time.

-

Delaplex:

Good business at good valuations. I had purchased it earlier in June but sold it due to some cash crunch and re-entered at the same price a month later. -

Tanvi Foods:

The company faces significant liquidity crunch.

They finally started production of the new manufacturing unit. The construction started at least 4 years prior.

The price has fallen quite a lot and valuations are completely off the mark.

The company also has significant inventory levels.

The production and sales from the new unit will command its future, else it is going towards mediocrity with the burden of fixed overheads from new plant.

New unit details:

3753d325-ac10-43a2-8406-bc5b90702aa9.pdf (bseindia.com)

Update on Bondada engineering:

I had sold the company in January with the reasoning of high valuations and it proved to be a big mistake. I have re-entered the stock, albeit at even higher valuations but they have started execution, and they routinely receive big orders.

Regarding previous high allocated holdings:

-

Omfurn:

I exited from Omfurn just before their FPO listing because of their poor subscription figures and high liquidity post FPO listing. I completely exited post H2 results. -

PNGS Gargi:

Once the holding turned into long term, I exited due to continuous trading at expensive valuations. The exit was just before their preferential issue.

My portfolio under SME stocks is at around 60%.

Average Holding Period post tax harvesting is 188 days.

From the previous post, I have exited in many of them post their sub-par H2 FY 24 results.

12 Likes

What’s your entry price for K2 Infra? It has corrected over 10% in the past couple of weeks.

In the 280s. I will be waiting for H2 FY 25 or H1 FY 26 results and then decide the next step.

But the problem with most of the SMEs is they will runup a lot before the actual results.

My entry price is also in the 280s. Are you indifferent towards H1 FY25 results? Do you wait for 2-3 quarter’s results to decide your next course of action?

Can you provide your opinion on Cadsys India? Is it buyable at current valuation? I know managements have written off receivables in past? But considering valuation, what you can do?

Anyways awesome analysis done by you. I just amazed how deep research you sir do in SME space .

I have sold Cadsys some time ago at around 200-210 range before the run up and dump face by the share.

The cashflow was disastrous from the start but PL was very good at that time (based on H1 FY 24 results). There is only one positive news posted by company somewhere in April regarding a hiring.

Press Release April 9th 2024 (nseindia.com)

The person is appointed as Independent Board member, so what would be actual impact I cannot quantify.

The loss of revenue of 8 million USD is a sad outcome for the company and considering their unsecured borrowings at high interest rates in USD, short term looks bleak. They have not written off the receivables, so it stays a question whether the management is willing to write off the receivables or create a reserve or do nothing and the auditor’s response for the same.

Meanwhile in the Annual Report the MD states that a weak and challenging Financial Year 2024-25 is anticipated.

Current valuations look cheap but considering the loss of revenue and a lack of cash flow generation makes the case very risky.

2 Likes

Any views on Abs Marine Services ?