It looked good at current valuation but after the annual report, there is some traction and promotion going on in social media platforms, so be a little skeptical about it.

I went through RHP and AR today and concluded that if executed as per targets, the company is indeed cheap on valuation front. On receiving 33 cr order from railways 2 weeks ago, the company mentioned 477 cr orders to be completed within 15 months.

The management is decent, customer concentration is bad as 60-70% dependent on Vindhya Telelinks under Jal Jeevan Mission.

The business has also changed a bit in FY 24 vs FY 23. FY 23 had higher margins and 36 cr from services while margins cooled down to industry levels and sale from services fell to only 11 cr. As per concall PAT would be between 10-13% which is in line with FY 24 margins.

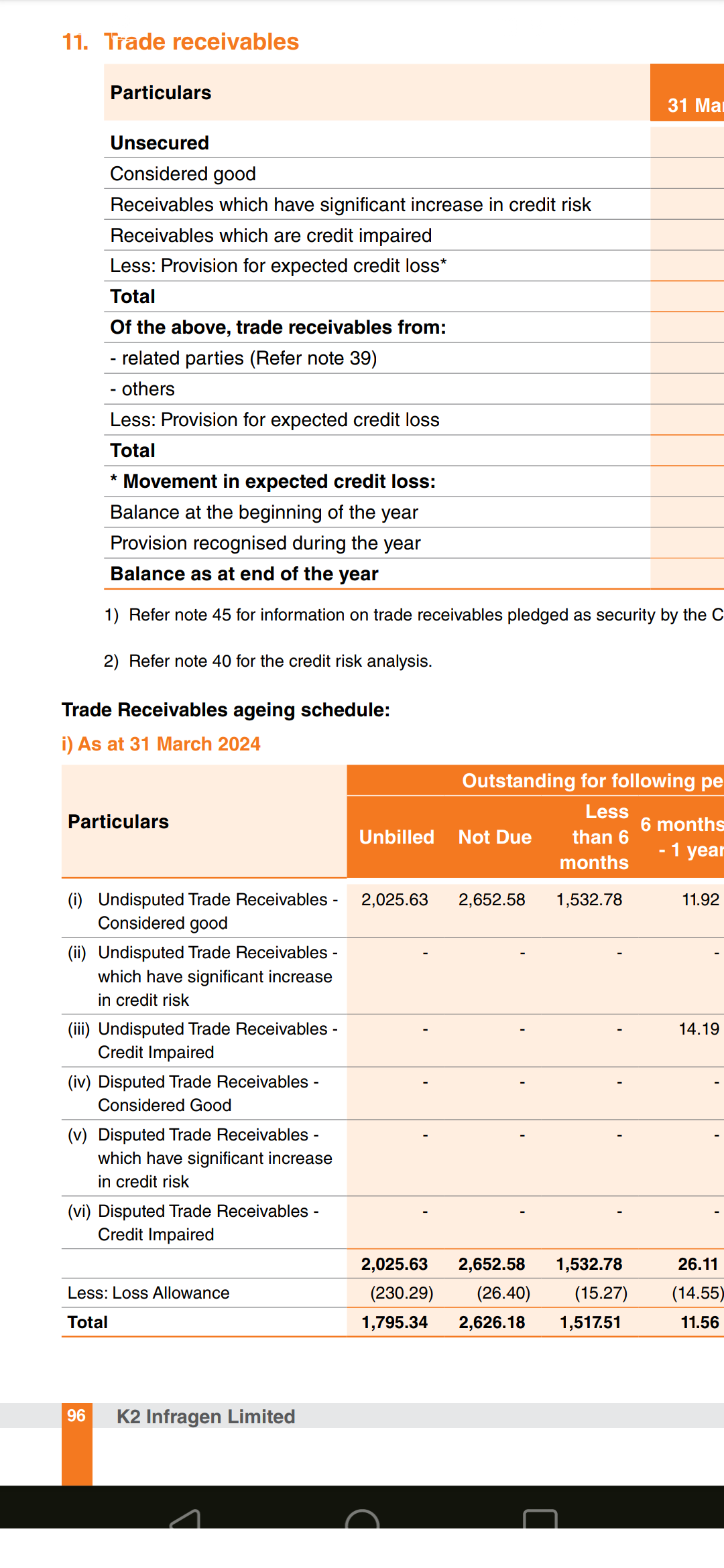

The company follows IND AS and is aggresively providing for credit loss allowance which is strange for a small SME company as there is no tax deduction available. In 2 years they have provided 6.5 cr worth of allowance. They are deducting it from trade receivables, so any moment on opposite side cannot be determined. Meanwhile they are also providing for bad debts and not adjusting it against Bad debt reserve.

One strange is this:

The company is providing loss allowance on unbilled revenue. This makes no sense to me. Why to book revenue and anticipate loss when it is not yet billed?

As mentioned earlier, company is at a good price if execution is done with stable margins. If that is to happen the movement of trade receivables will be the only concern atleast for H1 & H2 FY 25.

Disc: Under watchlist