A person who has read lot of investment books may not find anything new or drastically different. Atleast that was what I felt when I read this book after reading lot of books. But unless and until, you have practiced value investing principles atleast for few months and was confused whether you should be investing in a turnaround case or a company which has proven performance or whether to average down when the price is falling or whether to catch a falling knife, then you will find this book quite handy. No other book I have read till date deal with RISK in such a comprehensive manner as this book.

3 Likes

An excellent read.

No other book I have read till date deal with RISK in such a comprehensive manner as this book. ==> I agree with u Anil

New Memo by Howard Mark.(Dare to be Great)

http://www.oaktreecapital.com/MemoTree/Dare%20to%20Be%20Great%20II.pdf

I have started reading the book, and for me The Most Important topic that is discussed in the book is about RISK and how do we look about this subject. This book contains a full 3 chapters dedicated to RISK and almost every other para got something to ponder about.

HM defines Risk as -

“Risk means uncertainty about which outcome will occur and about the possibility of loss when the unfavorable ones do”

Risk means more things can happen than will happen.

He tell his father’s story of a gambler who lost regularly -

One day he heard about a race with only one horse in it, so he bet the rent money. Halfway around the track, the horse jumped over the fence and ran away

Poor gambler I must say.

Further he tells that Investment risk comes primarily from high prices which in turn is due to excessive optimism and inadequate skepticism and risk aversion. People fail to understand that almost everything is Cyclical. What goes up naturally comes down. Today’s performers will be tomorrows dog.

He compares markets to a pendulum.

The market has a mind of its own, and it’s changes in valuation parameters, caused primarily by changes in investor psychology (not changes in fundamentals), that account for most short-term change in security prices. This psychology too, moves like a pendulum"

Says, biggest errors are caused because of this psychology and not information or analytics.

I think, to be a better investor its important to be able to crunch the numbers of the company but also keep a check at the investor sentiment ruling behind the company. To much of money flowing to a particular sector should raise some alarm bells. Housing finance co ?

I think he talks about Second level thinking in the same book. This is easier said than done. These kind of things look good only in a bull market. Just to give a couple of examples. Lets take Amararaja and Exide. Exide is the second level thinking (valuation etc) here. But if you look around, you will see amararaja logo all over the place. (at least in Karnataka). There lies the confusion. How can one be sure exide will come back?. Other example is Indusind bank vs public sector banks. Second level thinking is that these psu banks have to have some value right?. But then the NPA issue never seems to end. ( Even in the recent quarter there was a big jump in NPA). How does one build the conviction to buy them?. The same can applied to Cera vs HSIL.

I would love to hear the views from the seniors like @hitesh2710 etc.

Thanks

Discl: I told all the companies mentioned above, except the PSU banks.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “RECOGNIZING RISK”

We have seen the process for the identification of risk in the previous article of the same series. In the current issue, I am going to discuss regarding recognizing of the risk.

For the successful investing, we must have to focus on the generating return with having a proper control on risk. And for the controlling risk, we require to identifying and recognizing the risk.

The risk is always being at a much higher where we are too much optimistic towards the particular scenario and also paying a much higher price for the buying particular asset. But we should focus on When odds turn out against us than how we can able to protect ourselves or get out of such scenario with least damage. So, for the protecting ourselves, we need to avoid paying too high prices and also keep ourselves away from the extreme level of optimistic sentiment.

Click for Video — Auction scene

We always forget the real worth of the assets in the bull phase and start chasing that asset class. Such behavior is dangerous for the health of our wealth. This increases the risk while we are purchasing assets more than its worth.

The market always works in a pendulum and people generally forget the nature of the pendulum. The pendulum always moves towards the both extreme directions.

Whenever pendulum moves towards the bullish extreme, many of us forget that such situations will not stay forever. Many of us forget about the risk which involves during the bull phase. And start taking higher risk for generating higher returns; which invites further huge amount of risk. At bullish sentiment, people generally buy assets at the highest valuations multiple and that invites the risk to the particular asset class. This scenario has a very high chance of getting damage to our wealth compared to generating a higher return.

Reverse to such scenario, whenever the pendulum moves towards extreme bearish phase, then generally people start recognizing the risk and start avoiding to invest in the particular asset class; which take out the risk from that particular asset class. Such scenario is the appropriate time for capturing the opportunities because in such scenario we have very less chance to lose.

Many a time due to bullish sentiment, we think that the risk is very low, we start taking more risky situations, also start taking leverage and from that time risk starts taking its shape. Our behavior towards particular asset class invites risk.

Risk will be only low if we as an investor behave in a careful and wise manner. We cannot eliminate the risk, but we can able to control its effect. We have to analyze risk in every scenario. Risk always has its presence, though we are having a bullish sentiment. And according to me, the risk is much higher while having a bullish sentiment.

At the extreme bullish sentiment, we forget to worry, fear of loss and instead of it, we think about to miss the opportunity. We think that all others will earn the money and we remain without earning money. We start taking much leverage and believe that we are living in a low-risk world.

Click for Video — Bull phase in auction

We have seen in the above video that the person who doesn’t want to purchase a horse for the Rs.5 lakh; same person bought the horse for the Rs.5 lakh due to the influence of the increasing value of the bid for the horse. The person doesn’t want to lose the horse and cannot see others to take that horse.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “RECOGNIZING RISK”

7 Likes

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “BEING ATTENTIVE TO CYCLES”

In this article, I am going to discuss on cycles and reasons for the occurrence of the cycle. For becoming a successful investor, we need to understand cyclicity of the market, earnings, business, etc., then only we can able to protect ourselves from the destruction of our wealth as well as we can able to grow our wealth.

We as a human also born, grow up and die. These cycles keep on continue. And like that company also came into existence, grow up and once it will close or might get some revolution.

(Click here for human life cycle - Humans Life Cycle Video for Kids - Science for Kids - YouTube)

As like our life, Economy, businesses, products, earnings of businesses, etc. also rise and fall. It also moves in a cycle. Many a time people forget that everything moves in a cycle and that situation provides us an opportunity for protecting and creating a wealth. We should always keep in mind that nothing in the world keeps on rising in a straight way. It will rise to an extreme level and falls to an extreme level.

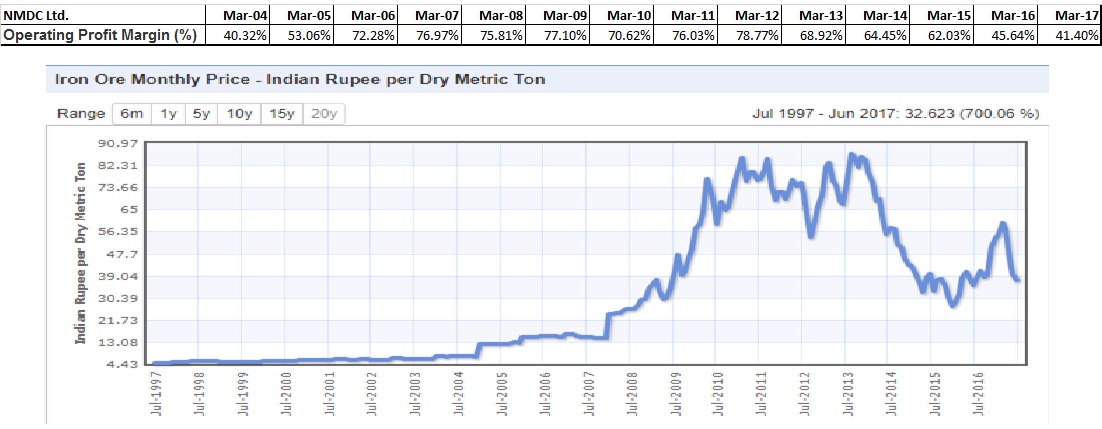

The margin of the company increases when the price of the iron ore increases and margin fall with the fall in the price of the iron ore. We must have to understand the cycle for protecting our wealth.

The main reason for the cyclical behavior of the economy is human involvement. Human nature is not mechanical but humans are emotional and inconsistent. Many a time Humans take decision based on their feelings, emotions which itself cyclical in nature.

When we feel good, we remain optimistic about the situations and reverse when we feel bad then remain pessimistic about the situations. Our psychological involvement pushes cycle to the extreme points and after that extreme point, cycle corrects itself to the reverse direction and then again come to the mean value.

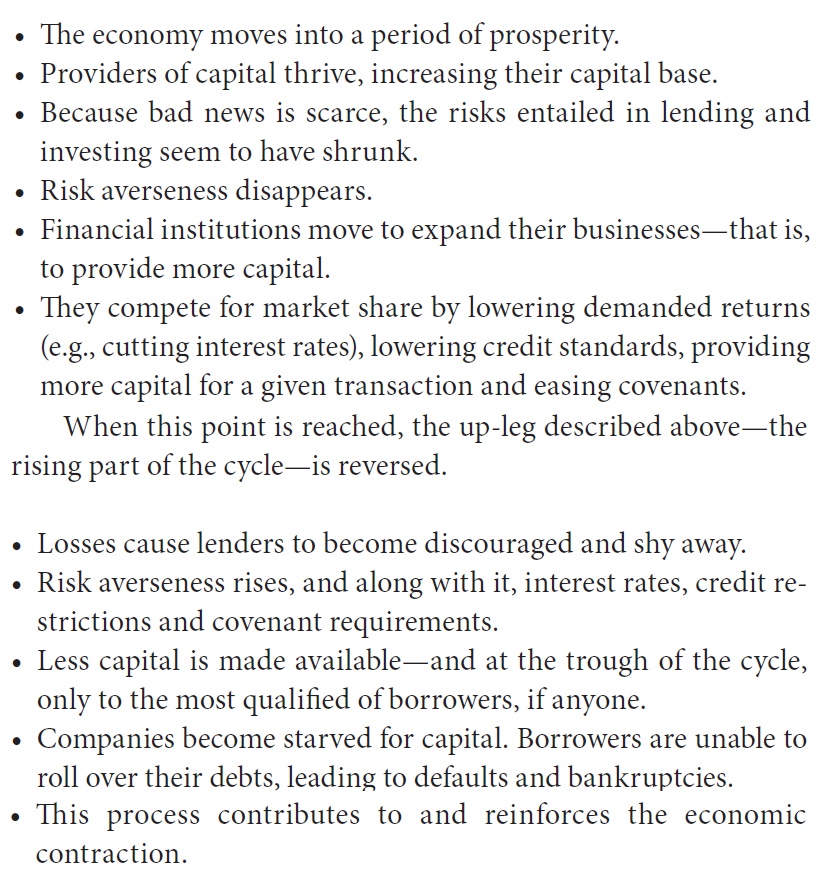

If we see carefully, then we can able to understand that more worst loan given at a good time rather at the bad time. Because people forget the cyclical nature of the economy, industries, businesses, etc. also the credit available at cheaper rate. And additionally, people break discipline. They start to borrow extensively which will be resulted into the burst of the credit cycle.

Credit cycle –

When we are happy then we might get happier for some period and then our mood turns to the sad and vice-versa. Our mood also keeps on fluctuating and that turns out to be our happiness or sadness. Sometimes we become extremely happy or sad, but that situation does not remain similar for forever. It will change, it will get normalized.

So, if the cycle is in good phase, then it might be remaining more good for the period and then correct for the bad phase and vice-versa. It will not remain good or bad for forever. It will come to the mean value at some point in time.

The cycle only stops occurring while people take all decisions by being unemotional and rational. But it is not always happening and such human decisions which will be resulted in the cyclical behavior of the market /economy. And this is only the major reason for keeps on occurring cycles.

High profit into the business attracts the competition. This competition will turn high-profit margin into the low-profit margin. And business will fall into the problem. Many players get close and get out of the business. Consolidation of among the players will happen and few players survived in the business. Those survived players will again be getting a good amount of business and the again cycle starts moving. No business keeps on growing for forever with the same pace of growth.

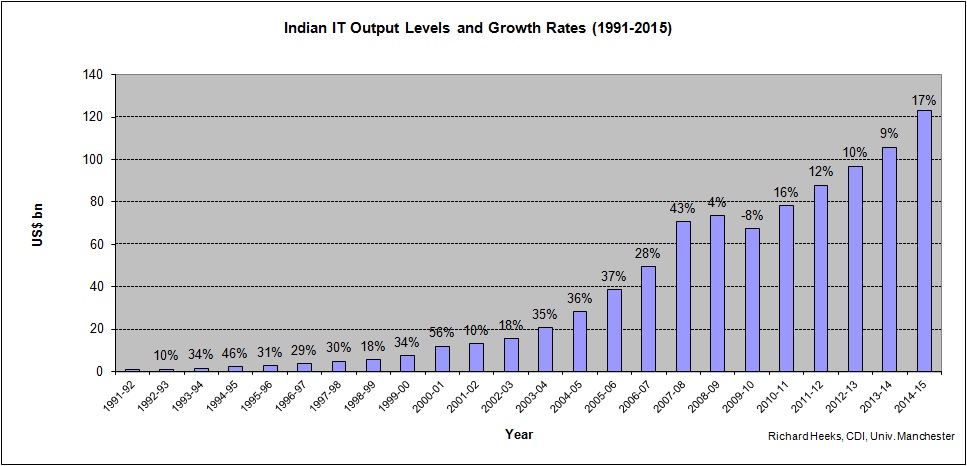

The growth of Indian IT is falling compared to initial days. Also, players among the industry and startup is rising rapidly.

We always need to keep in mind that everything moves in a cycle and when we forget it, we will be at the risk of losing our capital.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “BEING ATTENTIVE TO CYCLES”

9 Likes

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “COMBATING NEGATIVE INFLUENCES”

In this article, I am going to discuss regarding the psychological factors which affect our decisions negatively.

Market many times provide us an opportunities to earn superior performance through inefficiencies, mispricing, misperception, mistakes of other people.

But the question is why such opportunities come? What makes us different from other people? Why mistakes do occurs?

We need to analyze data and reach the conclusion. In investing errors occurs not due to analytical factors but errors mainly come from psychological factors.

Let’s look at the few psychological elements which affecting the investment decisions.

First emotion is GREED - Desire for money.

Most of us are making an investment for making more money. If we don’t care about the making more money than we are not going to make an investment.

And also there is nothing wrong with trying to make money. The market and economy run because of our desire to make money. But we should remain careful with a transformation of desire towards greed.

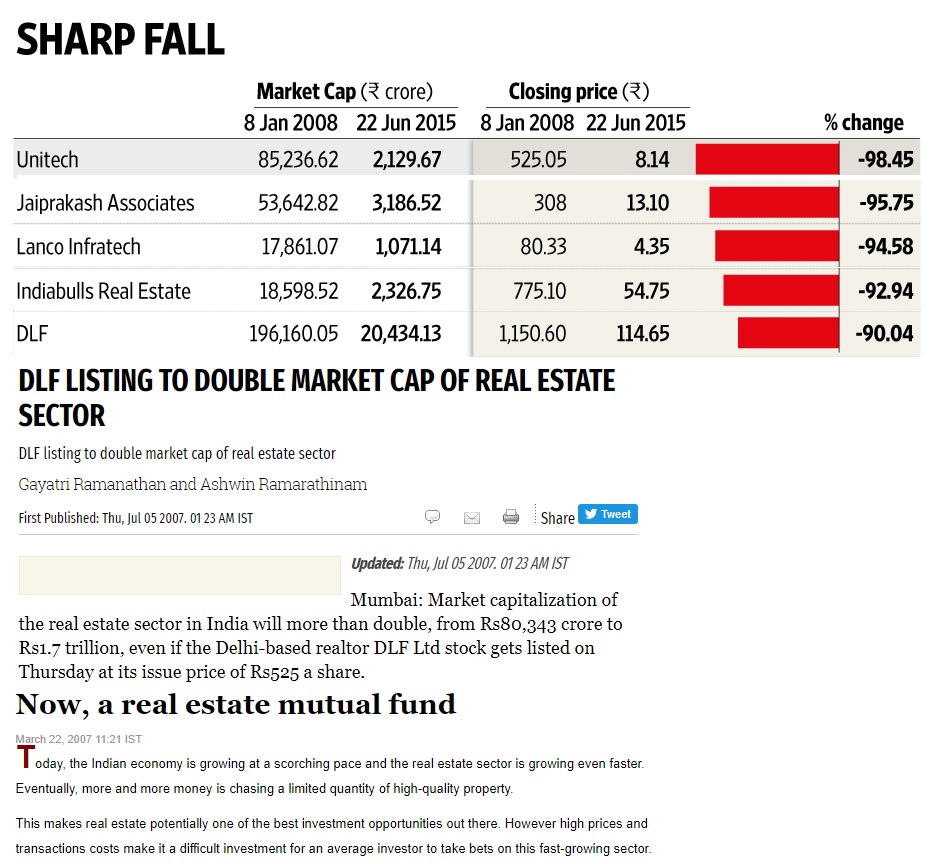

Real estate sector in India in the year 2007-08 creates a bubble and huge jump in the optimism by everyone. Such situation resulted under the sharp fall in the value of the sector.

Due to an impact of greed, people hope that their strategies help them to produce higher returns without taking higher risk for forever. And due to this hope, many times people hold highly priced securities with expectations of more appreciation can be possible. Many times such expectations went wrong and prove that expectations were unrealistic and people have ignored the risk.

Opposite of Greed is FEAR. As similar to the greed, excess fear is also harmful to the investors. Excess of fear stops us from taking a constructive decision while actually, we require taking such decisions. Due to fear, many a time we cannot able to make a good investment and also lose the opportunity.

The third factor is PEOPLE’S TENDENCY TO DISMISS LOGIC.

Generally, it happens that people stop using logical thinking and they start doing work with an irrational mindset. Many a time, we are not ready to accept logical reasoning for the situations and work as per unrealistic scenario. We do not apply what we have learned in the past but get easily deviate from those learning.

When market or a particular strategy starts generating higher returns for a while, then we started believing that it will continuously generate such returns without an involvement of risk.

Howard Marks called such situations as “Silver bullet”, the Holy Grail.

But is it really same strategy keeps on generating higher returns without risk?

As Warren Buffett mentioned, when prices started rising then it affects to the reasoning power of the people. It led to mania and situations of mania results towards the bubble.

The fourth factor is THE TENDENCY TO CONFORM TO THE VIEW OF THE HERD RATHER THAN RESIST.

Many a time, we started Believing to the crowd and starts to take an action as per the crowd behaviour. Though behaviour of the crowd is harmful and dangerous to us.

The fifth factor is ENVY. Envy comes into the picture when we are comparing ourselves with others. And envy works as a negative force which affects our decisions.

When we see that our investment is growing then we remain happy. But the time we start comparing our investment returns with investment returns of others then we become sad. Now, envy starts showing its colour and we make decisions which we may not take or which may be harmful to the financial health.

It is very difficult to see the higher growth of other compared to our growth.

The sixth factor is EGO. Ego gets satisfaction while we generated higher returns compared to others. And we are keeps on evaluating our return in the short term. While we should focus on the longer horizon returns rather than keeps on tracking returns in the short term and also try to get out of the trap of ego. Ego can be harmful to the financial health. We keep on demonstrates that how much we know much compared to others rather than focusing on how much we know and how much we do not know.

The seventh factor is the CAPITULATION. It means investors give up towards the situations while economic and psychological pressure becomes irresistible.

Many a time, overpriced assets become more overpriced, and under-priced assets become more and cheaper. This scenario affects to the psychology of investors and repetitions of such situations inspired investors to give up towards the situations and make investment decisions without using logical reasoning.

When few or all the factors combined then it affects to the investor’s decision making and that affects the market. This resulted in the mistakes and those can be expensive for our financial health.

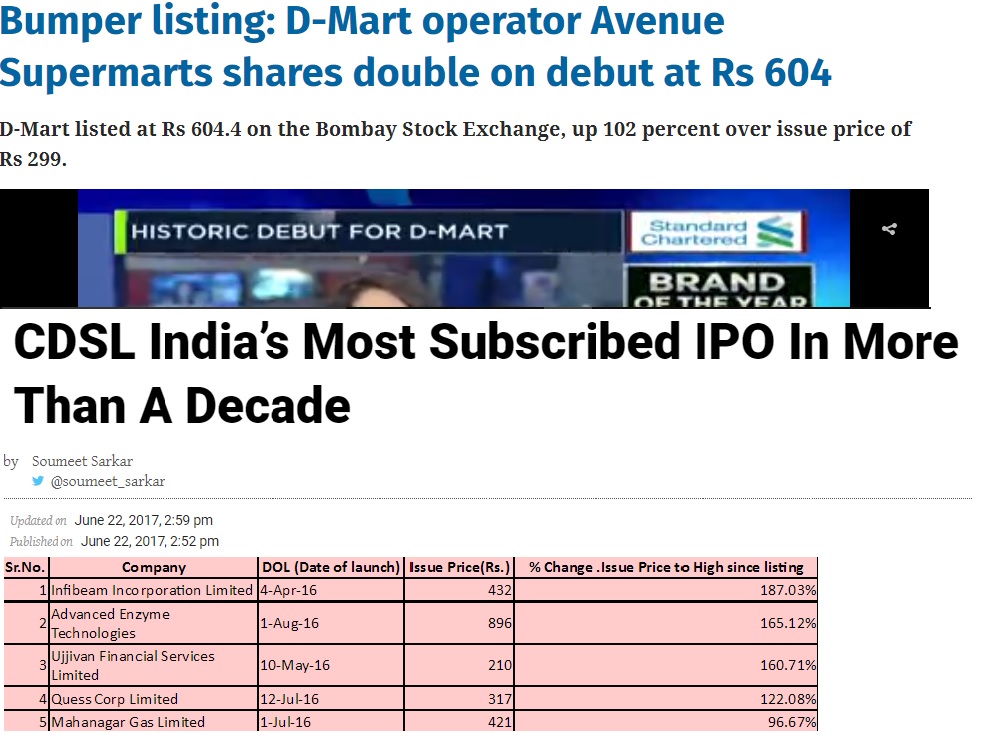

Psychology in IPO is funny. When our friend is applying to IPO and we asked for the business then he doesn’t know about the business. But he is applying for getting good returns. And he continuously getting higher returns and such higher returns earned by our friend attracts us to make an investment into the IPO. And such situations keep on repeating & more people get involved into the IPOs.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “COMBATING NEGATIVE INFLUENCES”

9 Likes

Thanks Jimmit1991. An Excellent tool, a mental model for gauging and understanding Risk… It will take me a while to find time to read the master; meanwhile your texts provide a good handle for the present times. Thanks again.

.

1 Like

A Talk by the Master on Google Talks :

3 Likes

Thanks a lot, what a presentation.

Everytime I read am finding different and new aspects of investment.

1 Like

I am thankful that my work is helping to others…

1 Like

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “CONTRARIANISM”

Many investors are following the trend for making their investment decision but for becoming a superior investor, we need to think in an oppositely.

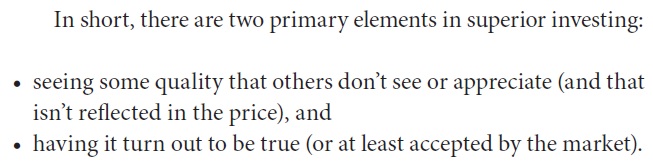

As we have seen that for becoming superior investors, we need to develop a skill of second level thinking. Second level thinking provides us an opportunities to generate above-normal returns and also protect us from the loss of capital.

We need to think against the crowd because crowd generally operates at the basic level of thinking rather than the second level of thinking.

If we engaged in doing what others are doing then we also get what others are getting. So for getting superior from others, we need to think differently.

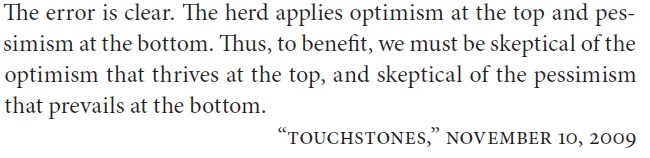

When we are joining the herd then following the herd can be dangerous to our financial health. When people are highly optimistic then prices started moving upward, top-level starts to form. And when people are panicky selling then prices started to go down, bottom starts get the form.

It seems much easier while we are understanding the concept but it is a much difficult task while we put it into the action.

-

We never come to know that how far pendulum will swing, when it will be reversed and how far it will swing to the opposite direction.

When pendulum starts moving towards an extreme then we are not able to know the extract extreme point and from where it will start reversing. Overpriced stock can become more overpriced and cheaper can become cheaper. -

We can be only sure about the reaching of the pendulum to the extreme level. We can just make an estimation that pendulum will reach an extreme, reversed it to mid-point and move towards opposite direction where it will reach to another extreme point.

-

There are many points which can influence the market behavior, many reasons which make pendulum to swing and not anyone strategy which is always able to generate a higher returns.

There are many examples where we can able to see the overpriced situations but we cannot be sure that such situations will reverse from tomorrow and starts going down. It can remain more overpriced and can keep on staying to the same situations for over a period of time.

We can able to see that expensive stock remains expensive for the longer period of time and cheaper get cheaper over a period of time.

Also, we cannot always go and make a decision to do the opposite of what everyone is doing. We cannot start walking backside as everyone is walking towards the front side. Just doing opposite of what everyone is doing, does not provide us profit-making opportunities. We need to analyse and make a logical reasoning then reach to the conclusion that we should go opposite or not.

If we just do opposite of what others are doing without doing proper homework then also we can able to lose our financial wealth. So that it is not only to take contrarian decision is enough but with it, proper homework is also required.

If some assets are temporary getting hate by people & with our proper homework then making a contrarian decision on it help us to generate an above-normal returns.

If everyone like some idea than probably it has done well or doing well. And if everyone is liking some ideas then prices reflect those liking. So much risk involves when crowd changes their mind. Price can fall significantly due to change in the mind of the crowd; which is harmful to our financial health.

We can able to create above average returns when we can able to buy an investment at the substantial discount. And the discount is available only when the major crowd is not liking it, not at where everyone is liking it.

For the protecting our financial health, we require having a skeptical mindset. When we skeptically analyze any situations then we will not fall in trap with the crowd. We have to always keep in mind that what can happen and what is the probability of occurrence of those events.

When a crisis happens than actually, we can able to see & believe in the negative side of the market. But we have to skeptically think regarding the negative side when positive waves going on. We always need to think that what can go wrong while everything is going in a good way.

If we believe in the story prevails among the market then we will definitely do what others are doing. We will tend to buy an investment at a high price with expectations of generating higher returns. We keep on buying overpriced securities with an expectation of another great fool will buy it from us. But we always need to keep in mind that while we are buying overpriced assets then we are only the great fool, no one else.

We will buy things which doing well and sell which performing poorly. Such actions resulted towards the losses during the crisis time, also we might not able to take benefits when things recover from the bottom. We remain followers not able to become contrarian.

We need to be skeptical enough for identifying the aspects that which is good for creating wealth and what is not good for it.

If we keep on follow the herd then we will not get a chance to evaluate situation skeptically and we will lose while the optimistic situation turnout as a pessimistic situation.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “CONTRARIANISM”

1 Like

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “FINDING BARGAINS”

In all the previous articles of the series, I discussed buying a cheaper assets / Investment. But buying cheap does not mean that we should go and buy anything which seems cheaper.

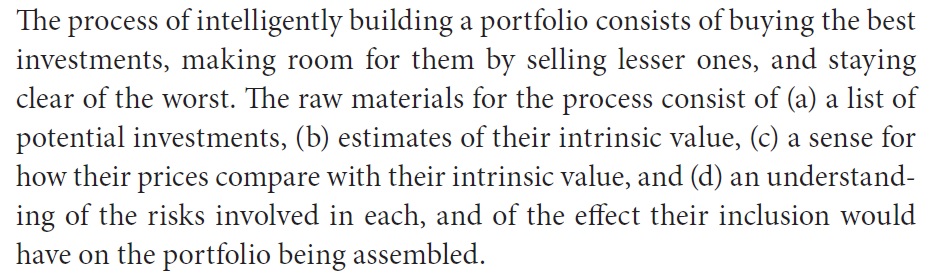

We need to prepare a list of investment ideas which are matches with our criteria, matches with our risk tolerance capabilities and exclude which are not matching with our criteria. There are not each and every idea which are compatible with our risk appetite, we need to work on the ideas which fall under our circle of competence. We get many ideas which can be good but not compatible with our criterion then we need to stay away from it.

Before eating a food, we need to know which kind of food we really like to eat. We do not like each and every food so as similar to it, we need to prepare a list of ideas which match with our criterion.

If we are managing the fund of others, then not only our risk appetite but also risk appetite of clients, we need to focus.

The second step is to select an investment idea from the prepared list; which is suitable for the potential returns and risk ratio, value for the money scenario.

After getting the list of the foods which we like then we need to work on the place from where we get a food with requiring quality, where we get food as per our spending, etc. we generally do not prefer to visit the place where food is not available as per our taste and preference.

If we pay high valuation for the any of the assets then it is logical that our potential returns will be kept on reducing and might be chances of occurrence of loss starts increasing. We making an investment for generating returns and enhancing returns.

We buy food for fulfilling our hunger not for exhibiting of our food dish with expensive food. We sometimes eat expensive food, not on a daily basis. As not only expensive foods can able to fulfill our hunger similar to that not only good and quality investment can able to provide us returns.

We need to focus on the bargain through which we can able to generate a potentially higher returns with minimizing risk.

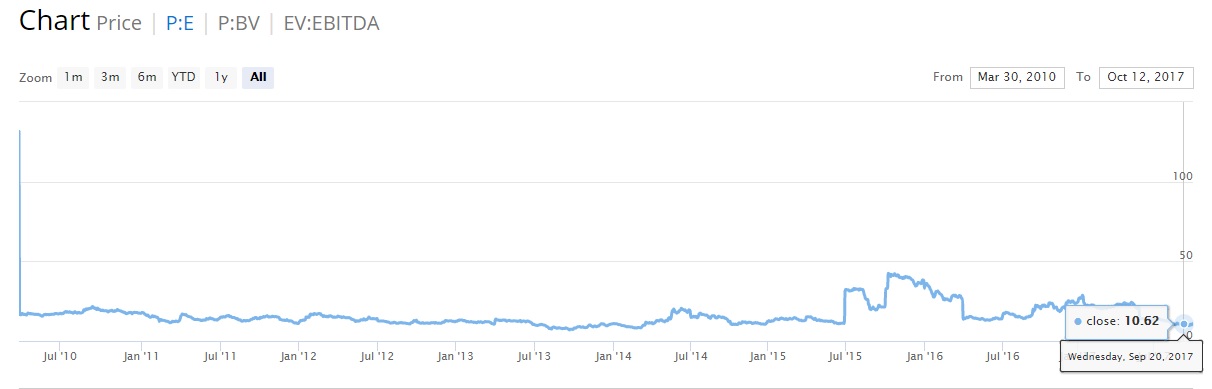

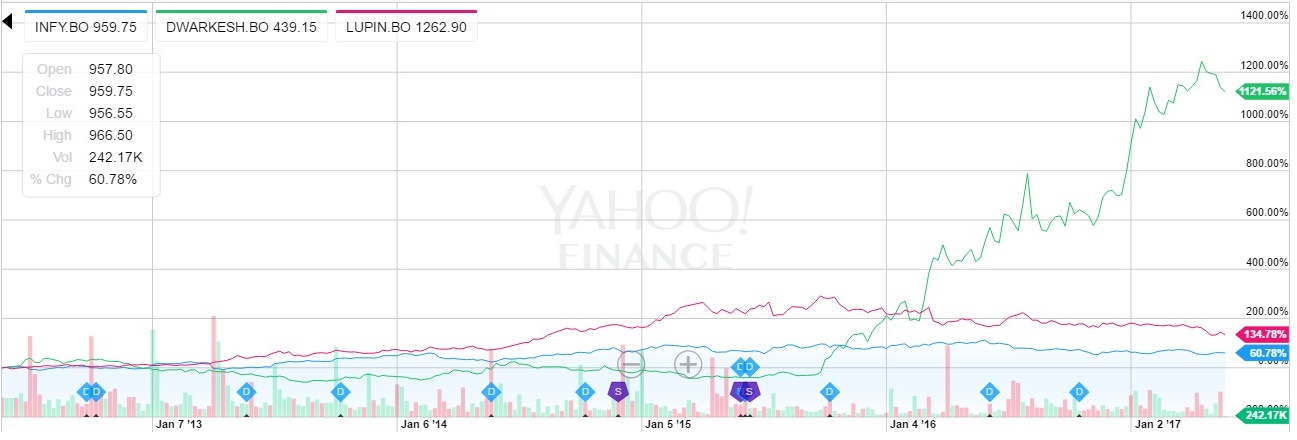

As I quoted an example of a good fundamental IT & Pharma company with cheap sugar company.

We can see that if we have bought the comparatively lower fundamentally good stock at a cheap price than this stock has generated a higher return compared to the good fundamental stocks in last 5 years.

Good food means we get a satisfaction & fulfill our hunger from eating that food, and that never matter how much expensive or cheap it is.

In general buying good assets mean, the assets provide us high potential returns relative to lower risk and also has a low price relative to the value of an asset.

Mr. Howard Marks mentioned that while popularity is high towards stocks and people hates bonds, also many institutions shifting from bond to stocks; such situations provide a bargain for the bonds.

When the time change and people seek for more safety relative to the price appreciation then they start recognizing the potential of bonds.

Generally, people start recognizing the potential of the assets while the price of an assets starts appreciating. But people who have identified assets earlier, those can produce above-average returns.

When the restaurant is crowded then only people recognize the popularity of a restaurant. We make a decision by seeing how much-crowded restaurant is. If no one at a restaurant then we generally not prefers to visit by assuming that particular restaurant provides a low-quality food. Similarly with stocks, when everyone is buying particular stocks then we also run for buying those stocks with assuming high quality with high return. We do not check anything and follow the crowd.

We should try to make an investment into the underpriced assets rather than fairly priced. Fairly priced assets just provide fair returns with risk involvement. So that we should focus on underpriced assets with risk involvement for generating above-average returns.

Bargain only available while perception is worse compared to the reality towards the asset. If everyone feels good and want to own that assets, then that asset will not be available at a bargain more.

When everyone cannot able to see the potential of the asset then we need to check the reason for unloved of the asset. Unloved assets can be available at the bargain if people hate it more than it should be.

If nobody is loved to the asset then nobody holding it So that demand for the asset will increase when people can able to see the potential of the asset. If our assumption has proven wrong and nobody is holding an asset or people unloved an asset then we might get limited downside or get the least loss from our investment.

When nobody to go for visiting a particular restaurant then we get foods at cheap cost with the quality for maintaining its customer.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “FINDING BARGAINS”

3 Likes

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “HAVING A SENSE FOR WHERE WE STAND”

Some category of people does not accept that cycle is unpredictable and largely unknowable, and those people put efforts for predicting the future. Few people ignore the cycle and adopt the buy & hold approach. They do not get aggressive or defensive with their investments in the cycle. Many people have wrongly understood the statement of Mr. Warren Buffett – “Our favorite holding period is forever.”

And the last category which is an appropriate approach for the investment. Such category of people accepts that cycle will occur. Everything moves in a cycle. Fundamental, psychology, prices, etc all moves in a cycle. We cannot able to know when existing trend will go, get the stop and start getting reversed. But we need to be confident enough that trend will stop sooner or later. No trend continuously keeps on going forever.

So that we should try to know where we are standing in the cycle rather than to predict timing and extension of the cycle.

By knowing where we are standing at the cycle, we cannot able to know what will be going to happen in the coming future. But we can prepare ourselves with a probability of occurrence of events.

I can’t change the direction of the wind, but I can adjust my sails to always reach my destination. – Jimmy Dean

Knowing present environment is not much hard compared to knowing future. We can come to know the present environment by observing the behaviour of participants around us, by observing our surrounding environment.

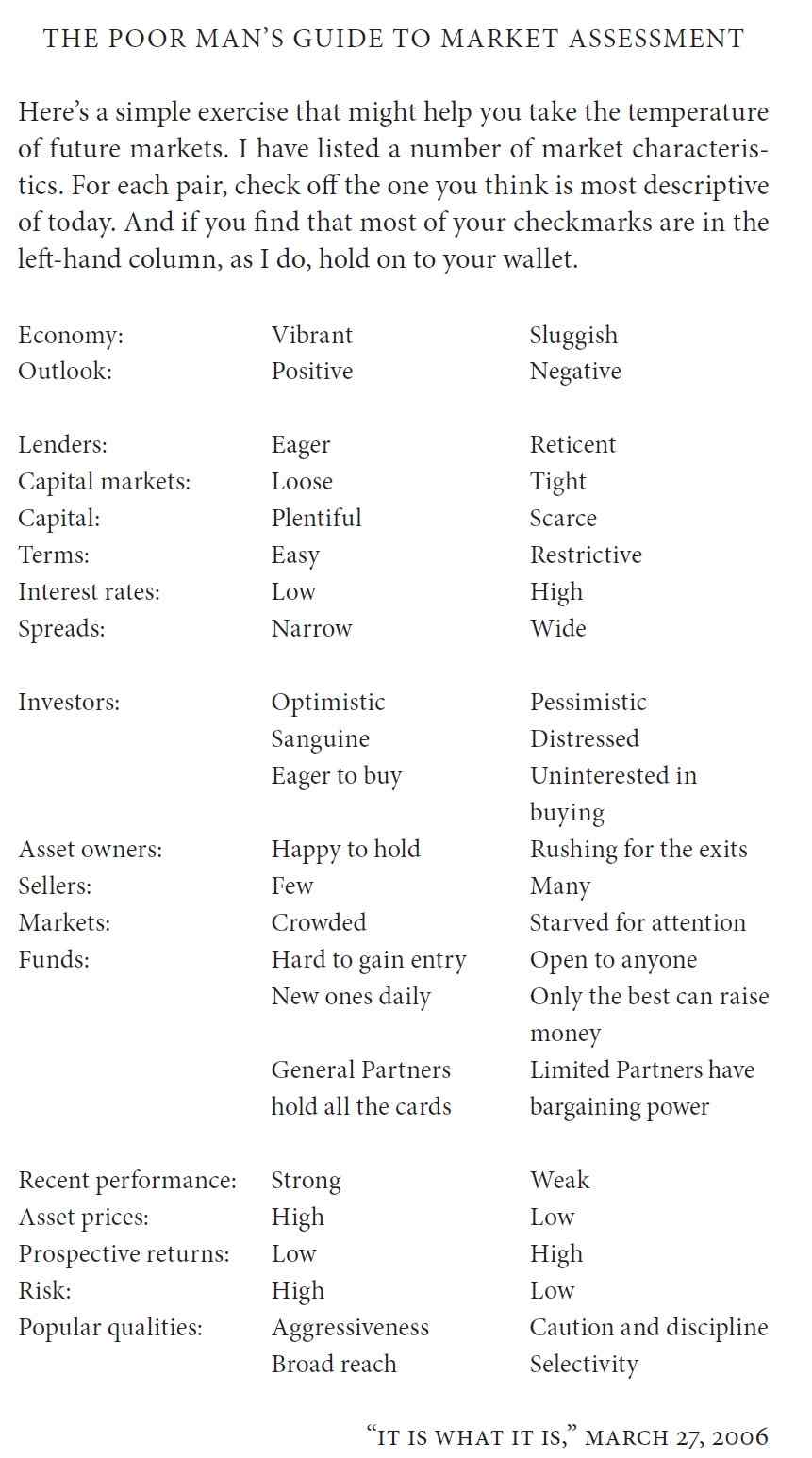

We have to focus on everyday events prevailing to the market. Such events provide us a rough idea of our position at the cycle.

When everyone is aggressive in buying a particular asset then we must have to take care and be aware of the upcoming risk. We should be aggressive in buying a particular asset while everyone is in panic and selling particular assets.

“Be Fearful When Others Are Greedy and Greedy When Others Are Fearful” ― Warren Buffett

We have to look around and think it by ourselves regarding present situations and make a decision that where we are standing in the cycle. What is market participants doing? What media is talking? Such questions need to be answered by looking at situations around us.

When too much money getting deployed into few assets then huge liquidity drives prices of an asset, such price momentum is not due to its actual fundamental. And also at the higher valuation people are ready to buy an asset aggressively. People are ready to buy Rs.100 worth of asset at Rs.200-300-400…. With the bright future expectations.

We cannot predict when huge liquidity gets dry but as a contrarian investor, we can prepare ourselves for upcoming risk.

We need to check which side majority of our answers falls and as per it, we can make an estimation of the present situation. And can able to prepare ourselves for the situations. When a majority of our answers falls at the happy situation then we have to be cautious towards the present scenario and vice-versa.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “HAVING A SENSE FOR WHERE WE STAND”

6 Likes

Excellent and explicit way of unfolding complex wordings with easy to understand example.

I really admire the person.

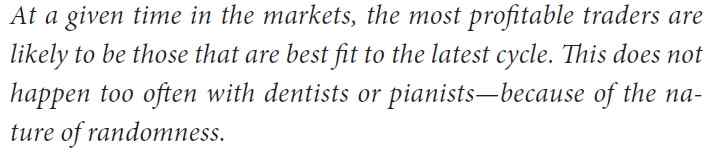

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “APPRECIATING THE ROLE OF LUCK”

While we involve into any of the investment decisions then those decisions are having dependencies on the future. As we know that future is uncertain and it is difficult to predict it. In such uncertain investment environments, luck plays an important role and we have to recognize the role of luck in our investment journey.

When we get some result or looking at the result then we must have to think the role of randomness in that generated result.

Many outcomes are visible to us but we have to think those outcomes with different viewpoints. If someone has made a risky & uncertain investment and he gets good outcome from it. We can say that such outcome happens due to luck not due to skill. But people take such outcome as their skill, not consider a role of luck.

For example, baller throw ball towards stump for capturing a wicket of the batsman and that becomes the wrong throw and ball has touch boundary line then it is not a skill of batsman but the role of luck.

Many times, people get the return on investment by just being in the right place at a right time. Not due to their skill.

If someone has invested his fund during the year 2013 with just making a portfolio with random stocks then also that person generated a good return. Doubled your Money in Last 3 Years? Skill or Luck?

In short term, we can able to generate a good return and many a time achieved an abnormal return by just being in the right place at a right time. But what about the long-term result? How we can say that luck always keeps on favoring us.

Generally, during a boom period, the person who takes a higher risk get highest returns. But that is not the reason to consider them as the best investors. Very few people appreciate the role of randomness or luck in the life or in investment journey.

Mr. Taleb has mentioned the list of things which are generally mistaken by us.

We should understand that when things going right, luck looks like a skill and people misinterpret lucky investors as skillful investors. Many a time, we get an extremely good reward by chance and we make a mistake to consider such result as our skill.

That means batsman hit ball for six and that ball also declared “No ball” and batsman get free hit and he again hit another six on a free hit.

In short run, we can win and make good returns by an occurrence of chances but in a long run, our wise decision provides us a good reward.

When we realize that investment outcomes get an influenced by the randomness then we can able to focus on every event with the different perspective. Otherwise, we just thought that such outcomes happen due to our skills only.

We have made a list of assumption for the occurrence of events but we also should focus on the occurrence of other different events; which we may not have assumed. It might be possible that sometimes all other events have collectively more probability to occurred compared to the single event on which we have put the huge focus. Such ignorance becomes dangerous for our financial health.

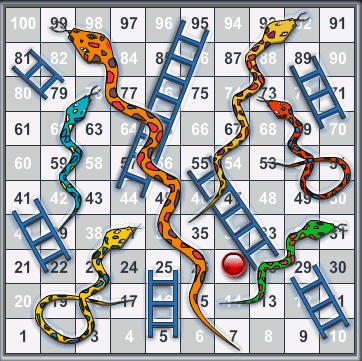

Investing something like a mixture of both skills as well as luck. Investing is not a pure luck like a snake and ladder game or not a purely skilled by the game of chase.

While we play chase then we require a skill to protect ourselves from moves of an opponent’s. We cannot able to win chase just by waiting for the favor of luck and mistake made by an opponent. We have to create a scene where opponent commits a mistake and we can able to win a game.

Whereas, there is not a requirement of a skill in throwing a dice while playing a snake and ladder game.

But we generally consider our winning as our skill while we should recognize that we are winning a snake and ladder just due to a support of a luck. While we should reach towards 100, we should not forget that there is a snake on 99 number which can bring us towards number 7. And transform our success into failure due to highly dependencies luck. Similar happens to us while we play an investment game on the base of pure luck. We may win till number 98 and maybe that our fortune transforms into failure by destruction in our wealth. We climb many ladders, get many multifold return generator stocks but we forget that such occurrence is due to luck. If we do not have our skill involve in it, then our wealth get destroy. We should not forget that investment requires a luck but also it requires a skill. If we fully dependence on the luck then we should never forget a snake on number 99.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “APPRECIATING THE ROLE OF LUCK”

3 Likes

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “INVESTING DEFENSIVELY”

Whenever someone asks us for an investment advice, then our first step must be an understanding his attitude towards the risk and return. We need to ask a question to him that what his choice - making money or avoiding losses is.

We cannot able to do both the things simultaneously in each and every situation.

If we provide an advice or we make an own investment without knowing attitude towards risk and return then we will not able to provide a proper solution. This is as similar as an asking for a cure from a doctor without disclosing our diseases to him. Investing is a full of bad bounces, uncertainty and random events which challenge us every time. So that such uncertainty requires knowing our risk-reward attitude for long-term survival into the market.

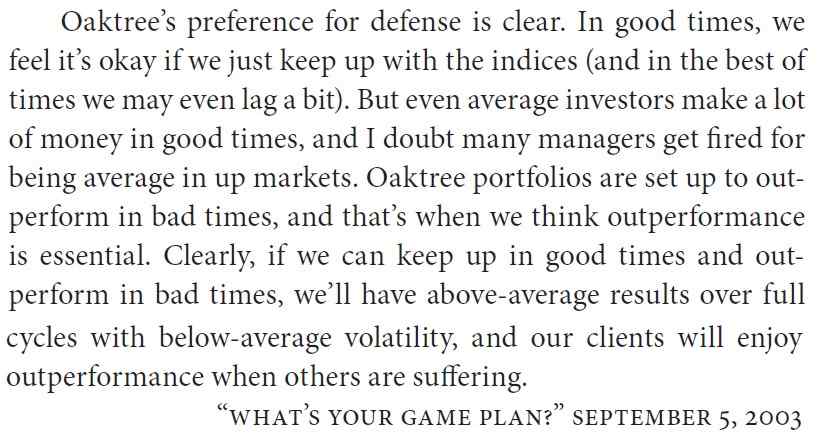

While we hit fewer losers then our probability to win the game is much higher. We need to choose how to play the game of investment - Offensive or Defensive.

We just need to do is to protect our wealth by not picking wrong opportunities. In investing, only avoiding losers is in our control, not everything else. We do not know what will happen in the future, our best investment can be turnout as the worst investment. But we have to be ready for it. We have to focus on missing wrong shots so that can protect game if our best turnouts as a worst.

If we look at the sports, many a time we need to protect our wicket rather play aggressively to make scores. Staying on a pitch provide us an opportunity for making a score while we get a good hitting opportunity. Investing also having many points which are similar to the game either positive or negative. As in cricket, Dhoni, Sachin, Rahul Dravid, Virat all having a different style to play a game. Some play defensive, some play aggressive and some make the balance of it. We cannot able to judge any players by looking towards his one match. Successful players perform well over a longer period of time with consistency.

Sometimes even a good players overestimate short-term success and forget to focus on the consistency of performance over a longer period of time.

As all players cannot be a Sachin, Dhoni, Dravid. As similarly, all investors cannot be a Warren Buffett, Charlie Munger, Howard Marks, etc. We just need to focus on our game in our comfort zone.

We are not able to know what will the result of the game we played, any uncertainty can affect it. We cannot only focus on one single investment ideas, we need to work on a selective group of ideas.

Negative side - If we keep on playing an aggressive investment game then we might not able to stick for the longest period of time in the game. Many uncertain events work as bounces for us.

Many a time, short-term investment success can become a reason to ignore the durable and consistent track record of investors. And few get attracted towards shine without checking its durability.

When opponents try to keep on throwing bounces then referee blows the whistle to give warning sign to opponents but in investing, there is no one who blows the whistle, we cannot able to get protected. Also in sports, we get notifications for the change of turn from our to opponents. But in investing, there is no notifications are available to us. We have to decide ourselves for changing the game from offensive to defensive.

We need to focus on the outperform into the bad time rather focus on outperforming into the good & best time. In good time, everyone can able to generate a good return but skill comes when we can able to outperform into the bad time. Doubled your Money in Last 3 Years? Skill or Luck?

Every player can able to play well against a weak team but a good player who can able to play well against strong opponents.

We should focus on either making more score or stay on the pitch for a longer period of time. We cannot say that only one way is the right way and we just need to select it. Selection of way can be based on our experience, learning, market environments in which we operate, etc.

We require a different kind of mindset for doing a right thing and avoiding doing the wrong thing.

Defense is focused on avoiding bad outcomes. It can help us to generate a higher returns but more through avoiding bad outcomes, through missing bounces, through managing risk.

If we bought an asset at Rs.100 and it falls to Rs.50; it falls by 50% but for reaching to Rs.100, that asset has to rise by 100% to just reach break-even.

When we play offensive and if it works then it will add additional returns to our investment. BUT if not works then it creates a damage to our investment and to our wealth.

Defensive game help us to stay in the game during a tough time also, it helps us to survive for a longer period of time.

Majority of a time, financial markets works in an average manner but it shows one abnormal day which has reason to destroy our financial health. We need to prepare for that worst day. We just can prepare for the worst day but cannot predict how worst it can be or when that worst day will come. But it’s sure that worst day will come.

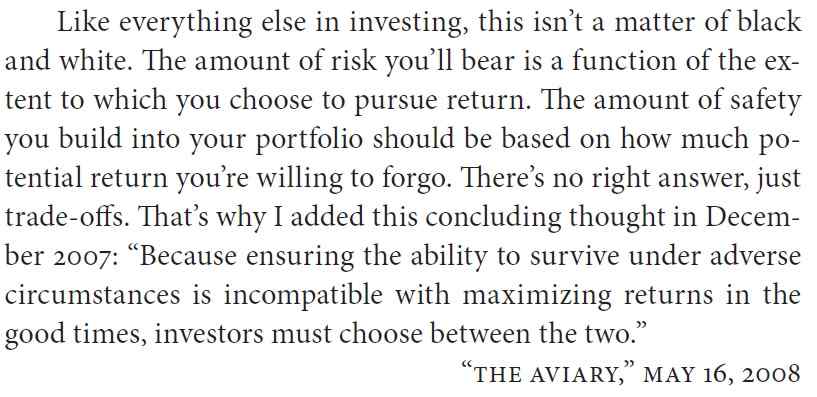

It is hard to say in investing that whether our investment becomes successful or not and it works in the future as we have expected, economy /industries / Companies moves in a certain way and we prove to be right every time. We need to take care of the unforeseen future events which can go against us and can meltdown us. Warren Buffett has given concept which can protect us from such unforeseen events that called “Margin of Safety”.

When we buy Rs.100 worth of an investment for Rs.90 then we have a chance to gain. But when we buy that same thing at Rs.70 then we have very less chance of loss and if odds will be in our favor then we can able to make a good return. So that buying cheaper provide us a “Margin of Safety” when our assumptions go wrong.

In the over-optimistic scenario, people buy Rs.100 worth of investment avenue for more than its worth (I.e. Rs.150, Rs.160) and then find a greater fool who will buy at the higher price from him.

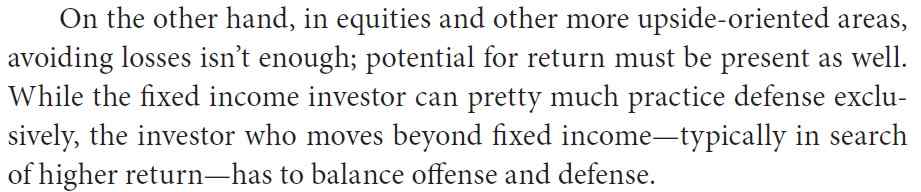

When we need an above-fixed returns then we need to go for more uncertainty but how to balance the defensive game with the inclusion of offense is the key area to focus. We cannot get higher returns with the exclusion of offensive game. We cannot able to win the match by just keep on making a single run. We need to hit 4 & 6 but with also focus on not losing a wicket.

Our first focus is to play a defensive game for staying on the pitch and then the inclusion of offense to the game for generating higher returns. Such approach provides us a consistency for a longer period of time.

If we take out a history of investment managers, investors then we will come to know that very few get survival for the longer period of time. Not due to their inability to make a 4 & 6 but to lose wickets in many matches. Many investors come and performed well in a good time but worst time make them disappears.

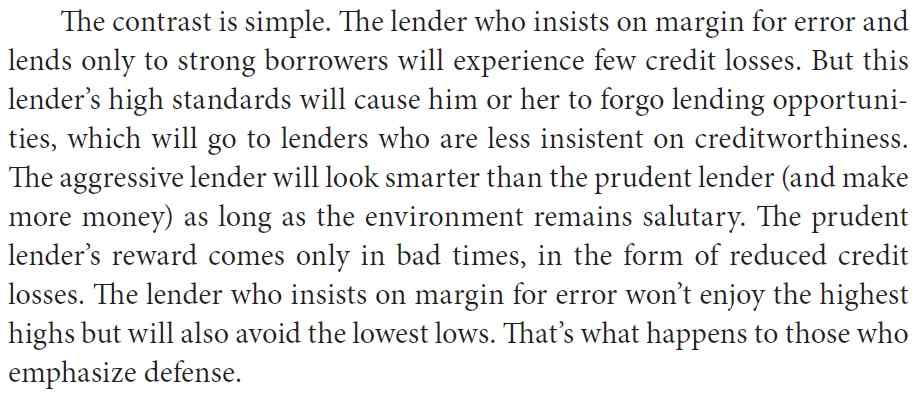

The managers who do not get survived for a longer period, the majority of them have built up their portfolio on based of favorable scenario and with the hope of likelihood of outcomes without keeping a room for the occurrence of an error.

Aggressive investors require competitive technical skills with fortitude, patient mindset, and capital. The investment might have potential to work well in a long-term but above quality provides a support to stay in a game for a long term.

We should focus on controlling risk, avoiding losses rather than try to focus on gaining again and again.

Simply defensive investing means being scared while making an investment decision. Worrying about losses, bad luck, worrying about something he doesn’t know, bounces etc.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “INVESTING DEFENSIVELY”

1 Like

We have seen in all article series of “The Most Important Thing” that Mr. Howard Marks is always keeping focusing on the avoiding losses. If we can able to avoid losses then our investment success will come to us.

When we are going to focus on the risk and avoidance of risk then there is a chance of under-performance of our investment portfolio during the bull phase of the market. But also we can able to get protected from the worst situations coming into the future. We can able to get survived into the market for a longer period of time.

For avoiding losses, we need to avoid the pitfalls which invite the losses. And sources of pitfalls can be analytical/intellectual or psychological/emotional.

Looking at the analytical/intellectual error - such error occurs while we collect too less information, uses wrong analytical methods, wrong approach, computational error, etc. Such errors wrongly direct the result and tend us to make a wrong decision.

One type of analytical error which is called by Mr. Howard Marks is "Failure of imagination”. This error means we cannot able to imagine or little in imagine full range of outcomes or not understanding consequences of occurrence of the extreme events.

“Failure of imagination” is the inability to understand the different range of outcomes in advance. In investing, we need to be dealing with the future and many a time, we try to assume that future will be similar to the recent past.

Most of the time future looks like the past so assuming it does not harmful to us. But what happens while future will not repeat the scenario as similar as happens in the past, either we have to lose huge money or no money made by us.

Events might occur or might not occur or it take times to occur compared to what we have assumed.

While we largely depend on the certain outcomes to happen in our investment then not occurrence of those events can kill our investment. So that we should always try to focus that if certain events do not occur then also we should not lose our huge money. We should focus on controlling our risk.

During sub-prime crisis also things do not work as it should work which resulted in a global meltdown. During sub-prime also investors believe that risky situations do not go to happens and securities are backed by assets based mortgage which encourages the risky behavior of investors. Majority of the investors did not expect that value of backed assets also can befall.

We should make an investment which can protect us against deflation and hyperinflation situations. We should not always a stick to the cash, treasury or gold to avoid pitfalls. But as a when requires, we should shift from defensive to offensive and offensive to defensive.

It is important to avoid pitfalls but there must be a limit which differs from each and every investor.

Psychological factors are most interesting sources of investment error. These factors tend to extremely high or low prices of an asset, sometimes very irrational. (My Article on Psychological errors - BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “COMBATING NEGATIVE INFLUENCES””)

One of the psychological factors is GREED. Excess of greed tends to be higher security prices. We want to make a more money and for that, we keep on buying an asset though it’s price trading at a higher range. We believe that assets will keep on appreciating into the future.

The second psychological error can be an error of not noticing. Sometimes we have a plan to steadily invest in the stock market. And we ignore the undisciplined buying by others has created a boom.

The third error can be not consistent with doing a wrong thing but failing to do a right thing. Average investors just being a fortunate enough by avoiding pitfalls. While superior investors avoid it and also take an advantage of it.

Our psychology resists us from accepting novel rationale and keep believing that “It’s different this time.”

The way pendulum swings, people forget to be skeptical every time rather believe that things keep on doing well.

The combination of Greed and optimism lead us towards the adoption of strategies which provides a higher returns without taking a higher risk. Pay higher prices for the securities with the hope of still left with an appreciation.

Just knowing about the pitfalls provide helps to us to some extent but the implementation of it leads towards success.

We should always learn the lesson and remember it throughout our journey. Mr. Howard Marks pointed out eleven lessons such as -

We should always be focusing on the things surrounding us. Excess supply of investment funds will lead to the situation called - “too much money chasing too few ideas”. Such situations can be dangerous for our financial health and we need to be careful during such situations.

When people become careless, investors not worried or skeptical about events, everyone becoming more bullish, increasing leverage. But we have to always keep in mind that such scenario will be going to reverse, it will never remain forever of the same magnitude.

It is near to impossible to avoid downfall but we can able to reduce our pain.

When we loss less than others then it provides a benefit to us such as we can able to maintain equanimity with others, able to avoid a psychological pressure and can able to generate higher profit by buying at a lower price.

Surviving during the declines provides us an opportunity to buying an asset at the low price. But for achieving success through this formula, we need to avoid pitfalls.

The way errors can appear to us is infinite but some of them are quoted by Mr. Howard Marks. Such as data or calculation error in the analytical process, ignoring the full range of outcomes or probability of occurrence of events, psychological factors (I.e. greed, fear, envy, ego, etc.), extreme risk-taking or risk avoidance behavior, etc. The second level thinkers can able to understand errors and also can able to detect over or underpriced assets. They can take a proper benefit of it and also take benefits of errors from others.

Errors are moves around us, sometimes assets prices reach higher level or reach the lower level, sometimes such extreme scenario happens with entire market, sometimes to individual securities. Sometimes an error occurs while we do something and sometimes doing nothing leads to an error. So that error is around us and without any errors, there will be no occurrence of any events.

All above-discussed points don’t indicate rules for avoiding pitfalls but it provides us an awareness, flexibility, adaptability, and mindset to take the cue from our surrounding environment. There are times where few of our acts resulted in errors.

And sometimes reverse to such acts.

BIBLIOPHILE: THE MOST IMPORTANT THING BY HOWARD MARKS “AVOIDING PITFALLS”