Post 17: How does a market linked product work?

A market linked product is a combination of a protection and an investment product. Customer pays premiums, gets a benefit of a life cover, some charges are deducted and the remaining amount is invested in equity or debt funds as chosen by the customer.

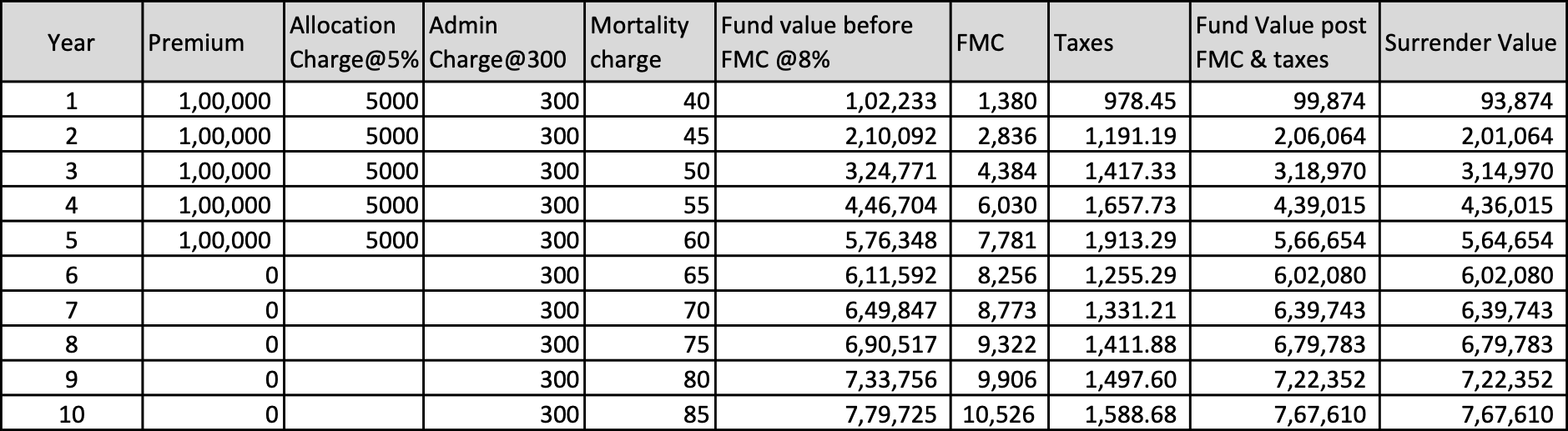

If one were to look at a customer benefit illustration, it would look like this:

This is the customer view. A few points to note:

• There are typically four types of charges – Allocation (initial charge on premium), Admin (monthly amount), mortality (for life cover), Fund management charge (FMC is applicable on fund value)

• While there is a lock-in for 5 years, surrender charges are low and infact, are zero after five years.

• Longer the maturity period, higher the customer returns and higher the charges that company can collect. Hence, there is an alignment of the interests of customers and company over the long term.

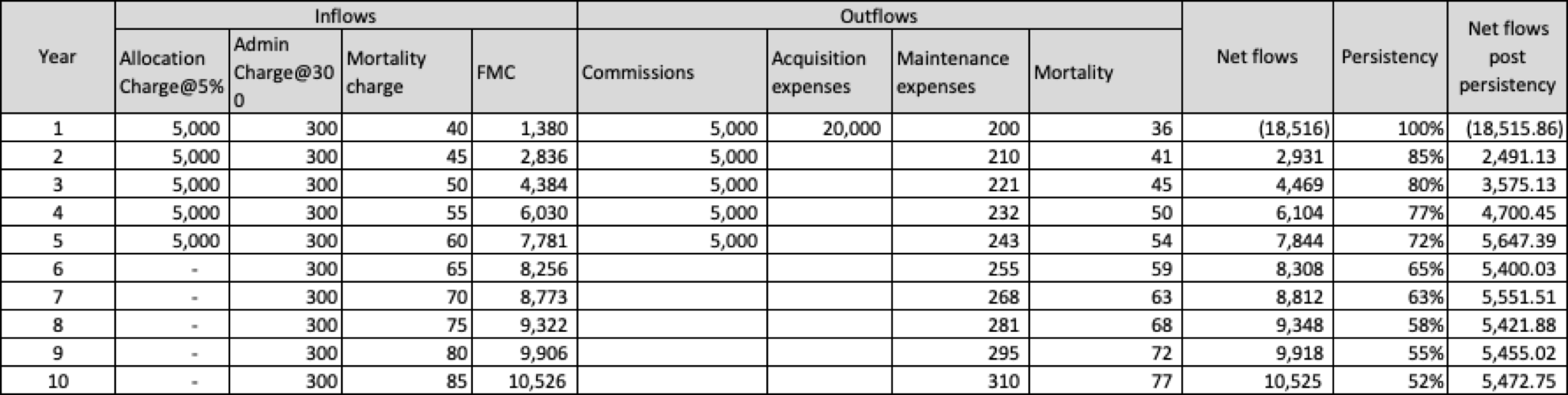

Now, let’s move on to the life insurer view:

In the case of market linked products, fund returns belong to customers. For the life insurer, the relevant cashflows are charges earned and expenses incurred. While charges are available in the customer illustration, expenses are not and hence, the insurer would need a separate view to look at its cashflows.

Key points to note:

• For the last column, NPV@7% is 11,362. Now, given premium was 100,000 p.a., the VNB margin is 11,362/100,000= 11% (remember this is an illustrative percentage)

• There is an initial negative cashflow which is called new business strain.

• Significant positive cashflows emerge later. If we do the NPV@7% for first five years, the number is negative 4,500. So, persistency plays a key role here.

• There is no significant impact of interest rates, while fund performance can impact FMC and hence, equity/debt market volatility can impact value.

• Impact of mortality can be marginal if experience is on expected line but if it varies significantly, it can impact value.

Key learnings:

• Market linked products can generate more value if persistency is better, expenses are lower and mortality experience is aligned

• There is strain at inception, so it consumes capital initially

• Interest rate impact is negligible

I have ignored many technical and regulatory requirements, but that’s fine for now since the objective is to just understand the product at a broad level.