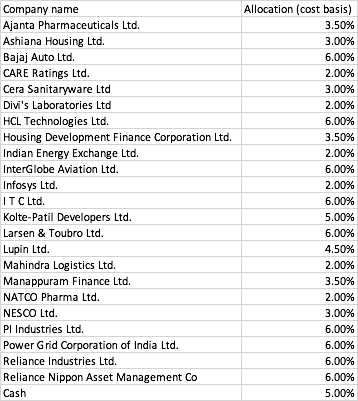

As of today, I sold Shemaroo. The degrowth in traditional business of 50% is too hard to digest. I continue maintaining a small tracking position. The updated portfolio is:

As of today, I sold Shemaroo. The degrowth in traditional business of 50% is too hard to digest. I continue maintaining a small tracking position. The updated portfolio is: