Caustic soda prices have cooled down from Aug level. However Q2 average price was good. Combined with continuous ramp up in solar power addition and diversification, company appears to be on steady ground. As power cost is the major expenditure for caustic soda industry, increase in solar power will help in adding to the bottomline.

As regards future Outlook, experts can comment on trend in soda price trajectory.

Further to my above post, I forgot to mention about the transfermor problem which led to disruption of some production line. Don’t know it’s impact, if any.

Company reported that around 120 TPD capacity of caustic got affected due to breakdown of transformer, which is approx 12% of total capacity, that too will be affected for around 60 days, hence impact would be around 2% on annual basis

1 Like

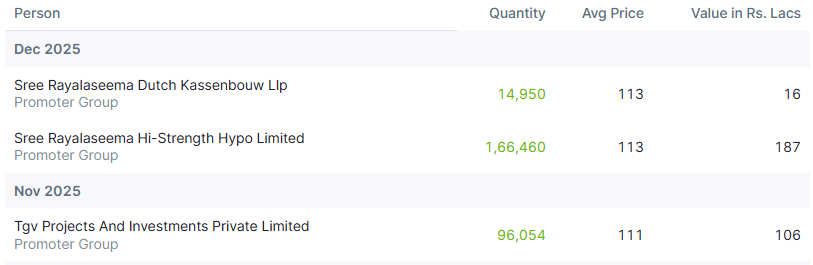

Promoter bought more stake in November & December at Rs. 111 per share.

Q3 results should see full impact of 10MW solar capacity addition & 10MW back pressure steam turbo that were added during last few days of Q2. However, there would be some impact of softness in caustic pricing + 120 TPD capacity shutdown due to breakdown of transformer.

Globally, Ineos Inovyn (Germany) has shutdown 200ktpa in Q42025. Dow chemical will start shutting down 250 ktpa capacity in mid 2026. Further, chlorine demand is expected to remain weak in Europe/US which will squeeze caustic production.

Alumina/Aluminum segment which is one the significant user of caustic is expanding aggressively in India. Outlook of Textile sector, which also one of the biggest user of caustic, is tied to US-India trade deal.

1 Like

Sab achha lekin fayda kya ? Shareholders get nothing , company earns very good but pays peanuts of 10% dividend even in good times, promoter finds one or other way to writeoff, also they take incentive on profits but don’t reward shareholder who stood with them in bad times also

2 Likes

Results in line with expectations; performance down QOQ due to 120TPS capacity shutdown & pricing pressure; also has a bit of impact due to change in Labour code, without this net profit would have grown at 24% YOY

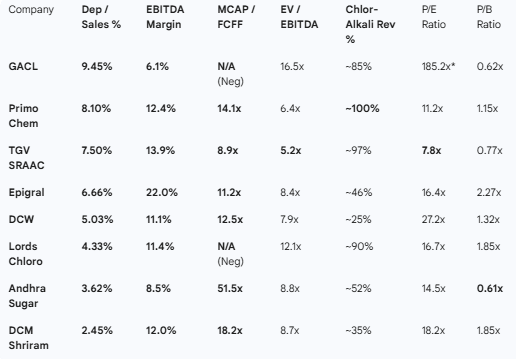

From FY26, TGV has adopted a more conservative depreciation policy by reducing the estimated useful life of its assets. While this aggressive non-cash charge temporarily suppresses Net Profit, the company continues to deliver industry-leading EBITDA margins of approximately 15%. Excluding specialty-focused peers like Epigral, TGV’s operational efficiency remains superior. Despite the accounting-led impact on the bottom line, the stock remains undervalued, trading at a trailing P/E of 8x and a P/B of 0.8x

Forward outlook is even more compelling when we factor in its aggressive expansion roadmap slated for completion by Q4FY27. The company is set to scale its caustic soda capacity by 50%, moving from 1,000 to 1,500 TPD, while simultaneously addressing its largest cost driver through the addition of 45MW of solar power and a 50MW battery energy storage system.

What gives greater confidence in the story is that the promoter has consistently bought at ~98 per share and then at ~112 per share.

Source:

2 Likes