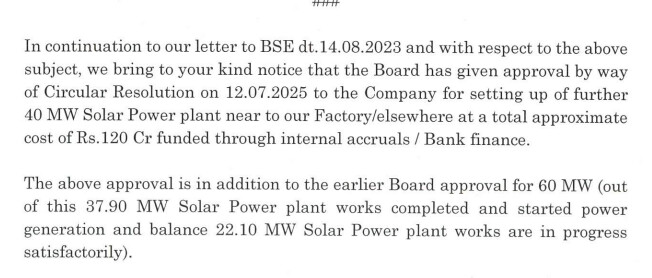

Capacity in Solar has recently moved up from around 23 MW to now 35 MW. Brings down cost of power due to substitution of electricity purchase from the Andhra SEB (Rate of Power will be Rs 7+ per unit from the SEB)

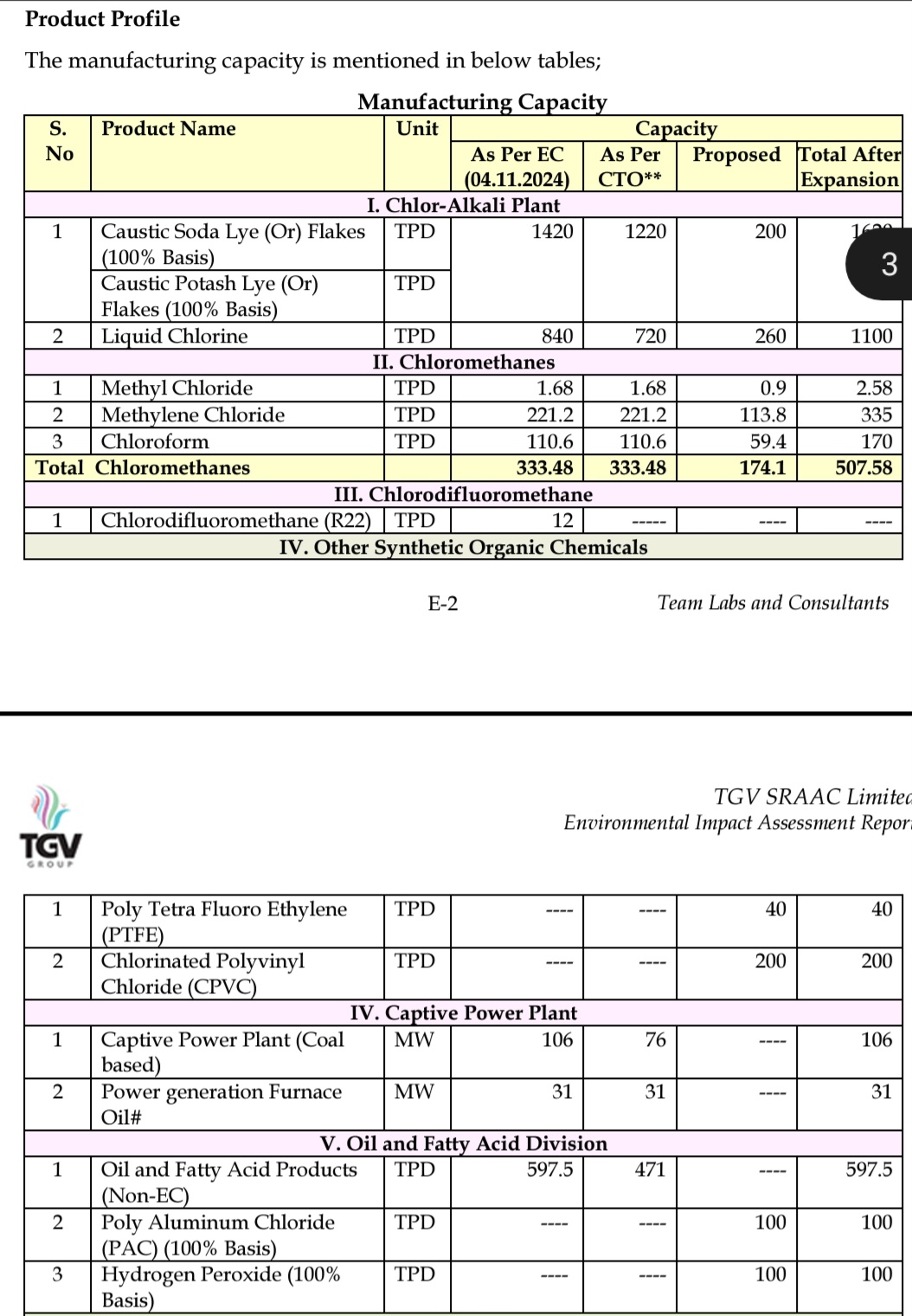

The capacity increase in CMS is 250 TPD moving to 380 TPD. Forward integration of Chlorine will be hugely beneficial. Other caustic companies in their recent concalls have mentioned negative realizations of Rs 9000 to Rs 10000 per tonne of Chlorine. Even if CMS sells at breakeven price, the negative realization of chlorine will be absorbed by forward integration efforts.

With commissioning of both the abovementioned investments the company will claim additional depreciation on assets and defer its tax payout thus positively impacting cash flows.

(This shows up as deferred tax liability in the P&L but actually is a non cash expense representing taxes that need to be paid in the future. Historically this deferred tax shows when they commission some capex). One needs to look at PBT or EBIDTA growth to get a better perspective of financial performance.

These structural changes will benefit future quarterly profits and cash flows. Basically ROCE profile of the company is improving which will help in better profitability across cycles.

Disclosure: Biased, Invested, Post for educational purpose only and I am not a SEBI registered analyst.