I am reposting this after understanding the forum guidelines. I was not able to edit my original post so created a new one.

I have this company in my portfolio which makes fittings and fasteners for pipes, solar modules and have recently announced order win larger than their market cap.

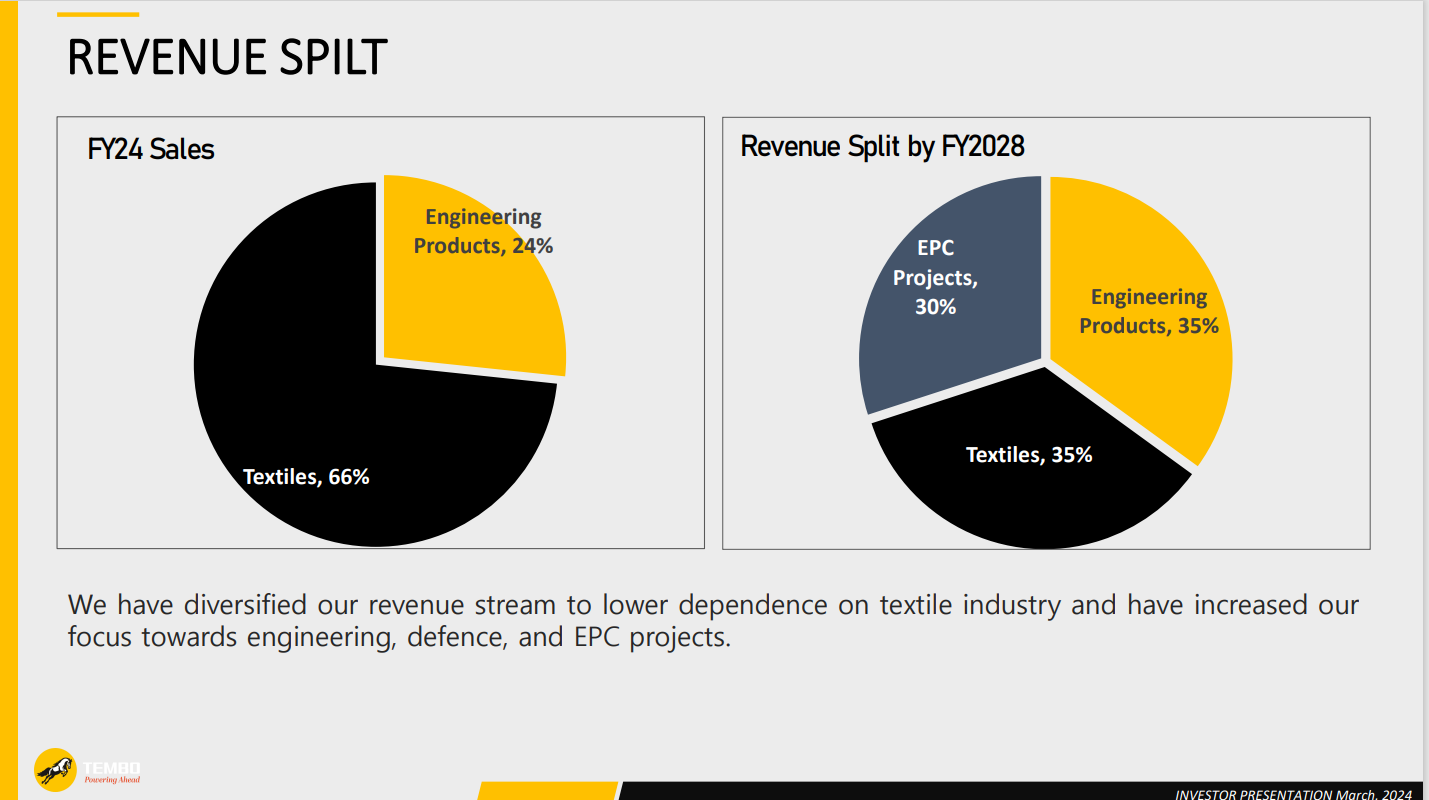

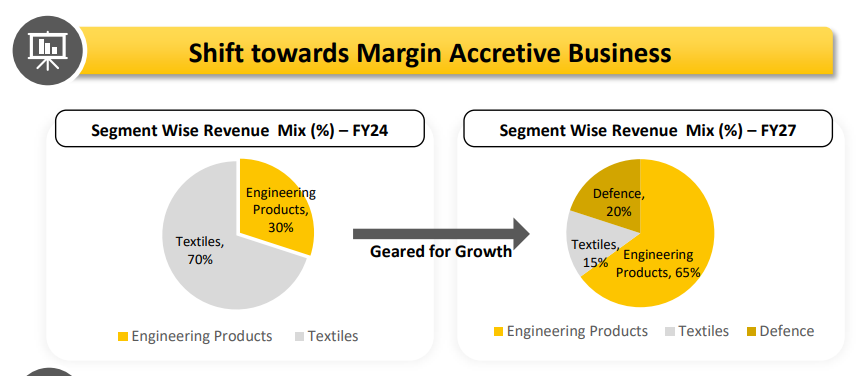

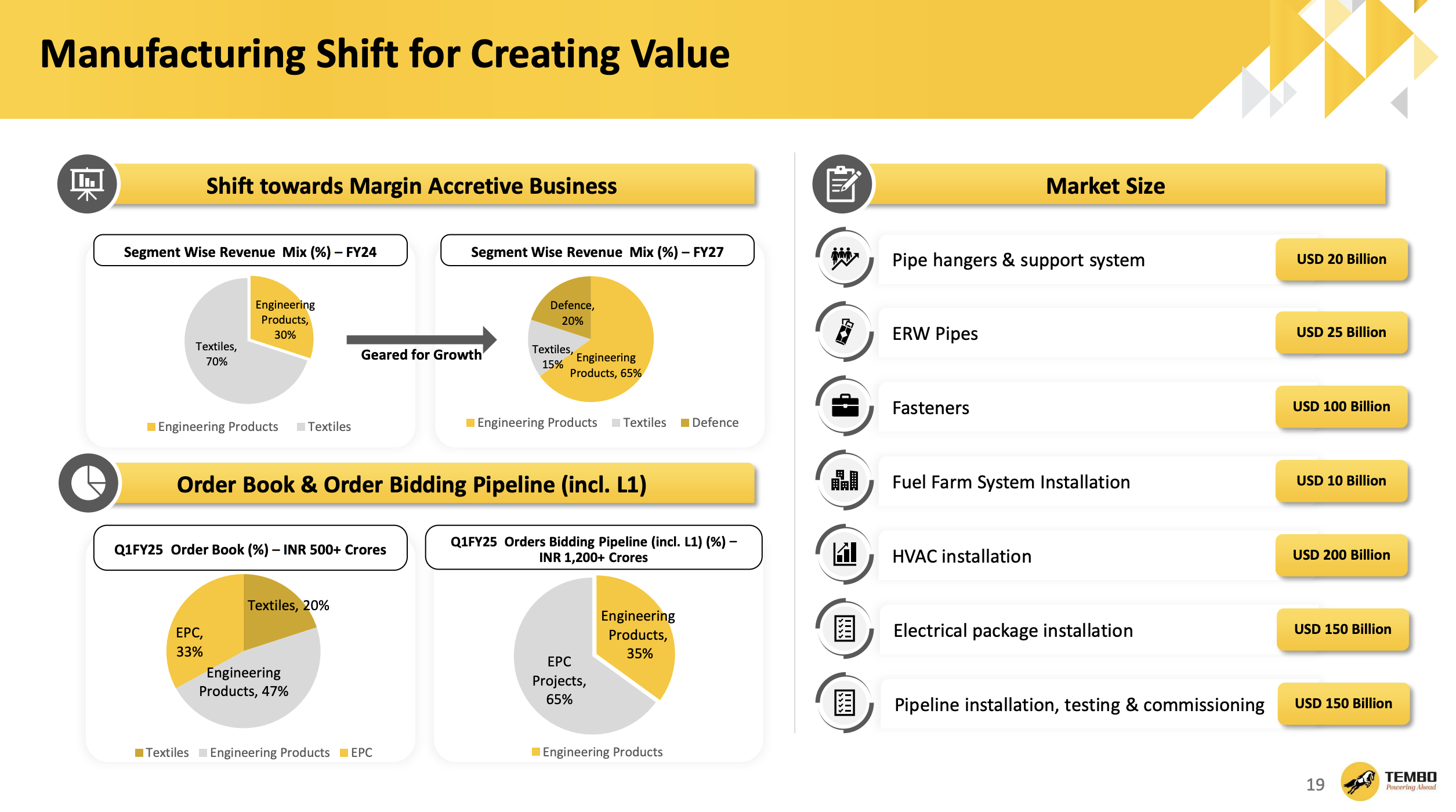

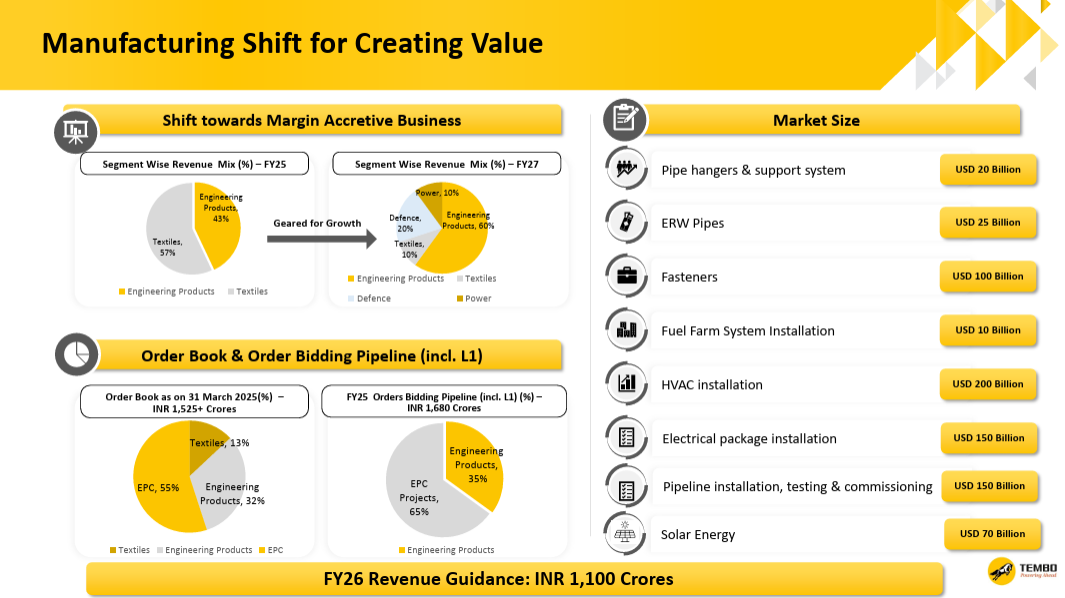

Tembo Global is a New Mumbai based company involved in manufacturing & trading of metal items for supporting of pipes, HVAC ducts, solar panels. They make various types of supporting items like hanger supports, U-Bolts, anchor bolts, saddles etc, anti-vibration systems. They also make forged fittings and flanges which are used for completing the piping installation. This company is also in trading of textiles. The current MCap of company is 266 Cr

With the ongoing infrastructure work and capexes in varous industries, there seems a good opportunity for such a company to grow it sales. For example let’s say an apartment building is being built, it will need fire hydrant piping. This company makes supports on which fire hydrant piping is installed. Or let’s say a hotel or a company is built which also has HVAC (this is a centralized air conditioning and ventilation system) in addition to fire hydrant, then this company also makes supports and slotted channels for the installation of HVAC duct in addition to floor and shower drains that are required in each residential apartment/hotel room. In chemical or oil and gas industries lots of pipes are installed for material movement. These pipes need to be suitably fixed during installation using U-bolts, anchor bolts, hangers. This company manufactures such items.

The major raw materials are MS strips, MS rods, steel alloys. Change in prices of steel would have an effect on the input cost, but I have generally seen that the product prices fluctuating along with steel prices.

From screener, I found below:

Sales growth 3 years: 47% and profit growth 3 years: 43% compounded.

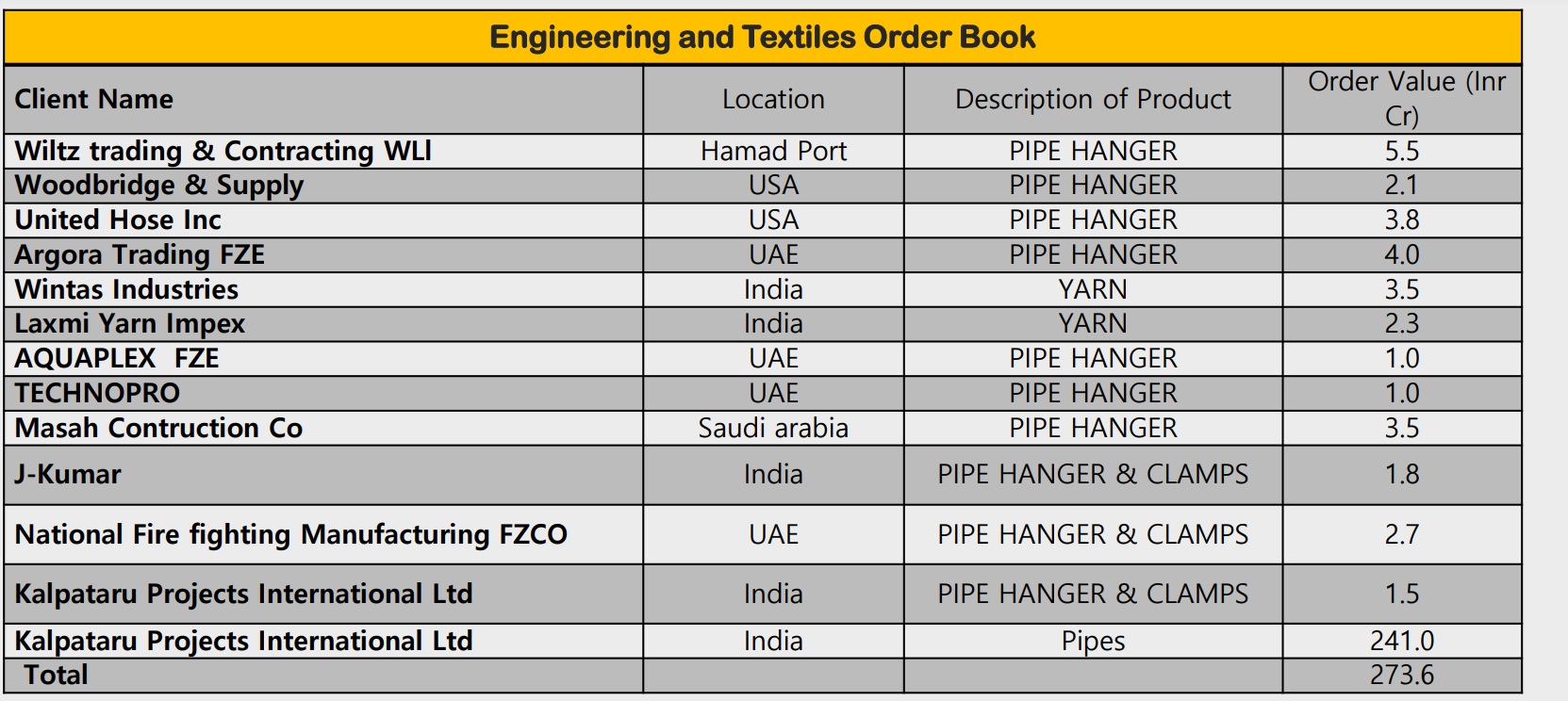

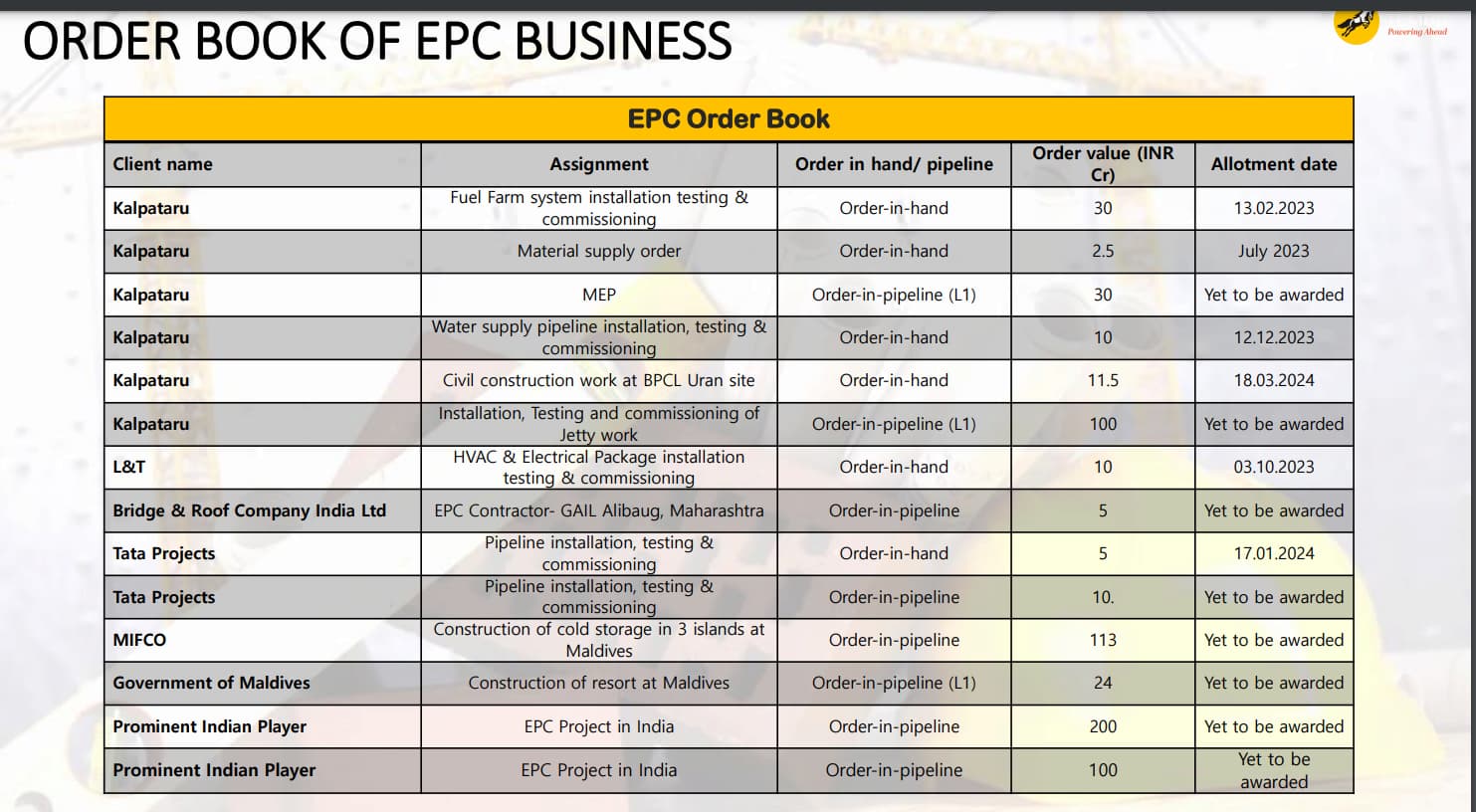

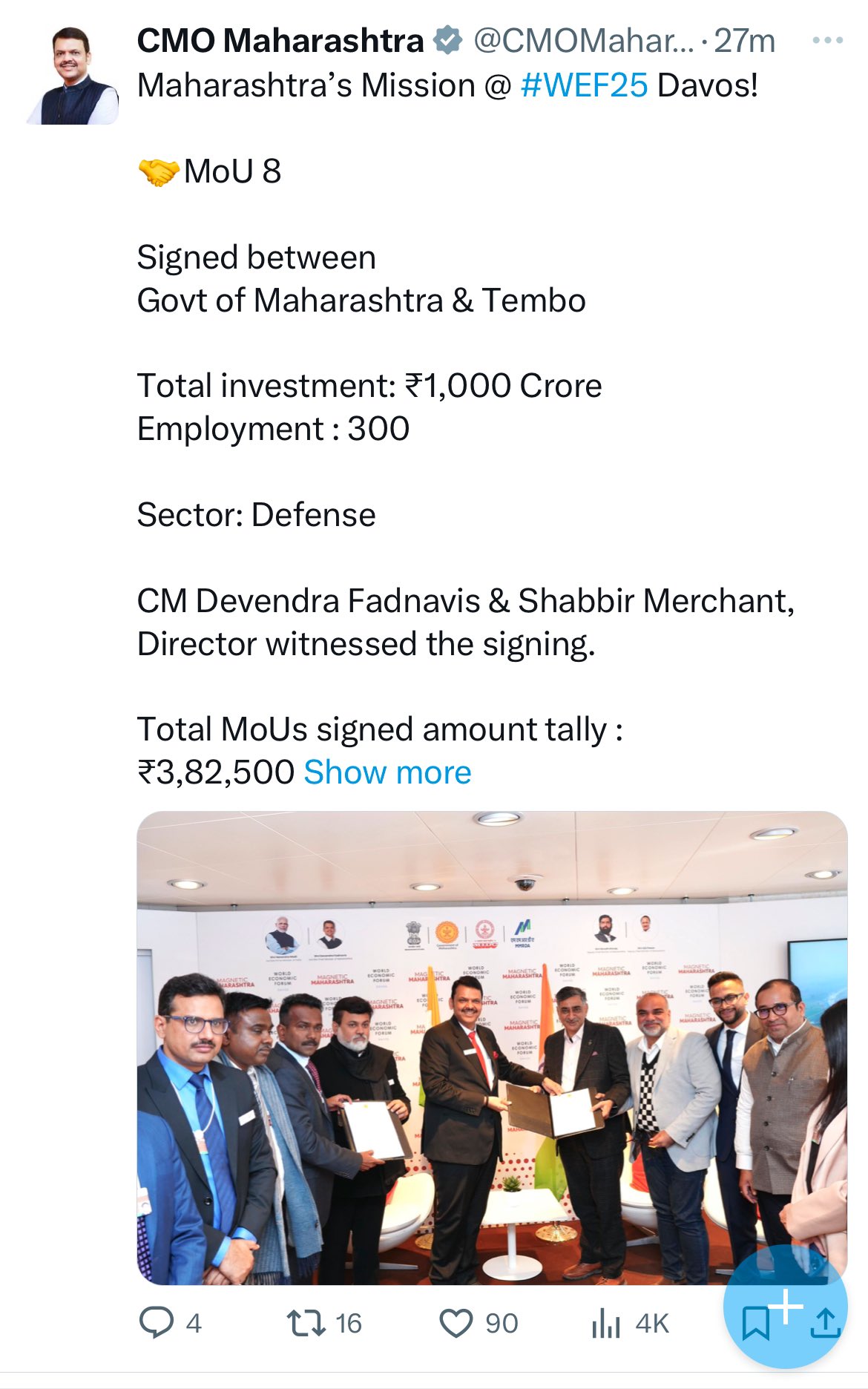

However, the operating margin is very less (approx. 5% for last two years) which means they make commodity products. However, what brought this company on radar is the sales growth and growth in fixed assets (plant & machineries was 5.74 Cr in Mar’20 and 7.29 Cr in Mar’23). I do not remember the screener filters I made, but was now trying to understand this company better after their announcement of order wins of about 241 Cr on 10May24 (https://nsearchives.nseindia.com/corporate/TEMBO_10052024145728_order.pdf).

There is no mention of customer in the announcement so I believe this is their cumulative order wins over some time. (They also had announced an order receipt from Kalpataru of approx. 9.45Cr for a civil contract work of BPCL, but withdrew it on 15Feb24 after Kalpataru delayed the civil contract order.)

Other quick information:

Below is renumerations of promoters from their FY22-23 annual report.

Mr. Sanjay Patel is 42 lakhs

Mr. Shabbir Merchant is 49 laksh

Ms. Fatema Shabbir is 33 lakh and 0.1 lakh for sitting fee.

Total renumeration (except sitting fee) is 20.8% of their net profit for FY23-24.

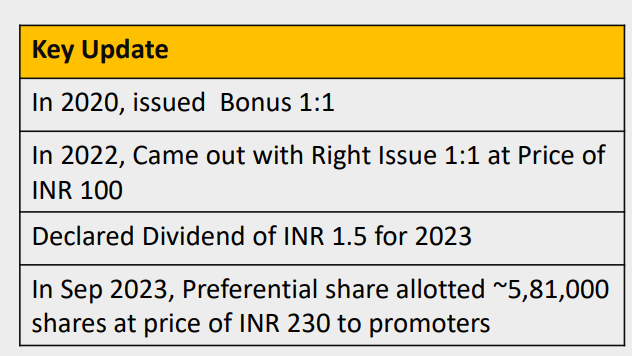

As for the promoter shareholding, the promoter shareholding as start of FY22-23 was 72.7%, at end of FY22-23 has gone down to 55.4%. The company had brought a rights issue in Aug’22.

Summarized thoughts:

If the government policies change or there is a pandemic like Covid, it will affect the growth of company.

With increase in government focus on infrastructure, government and private capexes, there will be growth in new buildings/hotels/airports/factories etc. all of which need the products that are made by this company. Their sales growth of last few years, increase in fixed assets and looking at their balance sheet and cash flows I am trying to understand more about the robustness of the business of the company.

What are the pointers that would indicated robustness of the business of this company?