Will this satellite make Tejas’s Direct to Mobile communication possible?

ISRO to Launch BlueBird Block-2 on LVM3-M6 Rocket Shortly ISRO to Launch BlueBird Block-2 on LVM3-M6 Rocket Shortly

Will this satellite make Tejas’s Direct to Mobile communication possible?

ISRO to Launch BlueBird Block-2 on LVM3-M6 Rocket Shortly ISRO to Launch BlueBird Block-2 on LVM3-M6 Rocket Shortly

It is good to note that, Khush Tech, a Tejas partner for D2M mobiles, is exploring online e-commerce distribution opportunities, talking to telecom service providers for bundling D2M mobile devices with their services and creating an integrated UPI payment mechanism on D2M-enabled mobiles, tablets, and laptops. This will definitely increase revenue potential for Tejas Networks in the coming years.

Tejas networks shares have fallen long enough and deep enough for me to finally take some time and do some work on it. Here is my understanding of the situation. I can be completely wrong and the following is certainly not a recommendation to buy, sell or hold.

Currently, we are seeing 90% yoy revenue fall due to the BSNL work being finished(almost). The market is treating it as a spent force. There is a leadership vacuum since the last CEO resigned. Receivable are very high, which has lead to heavy debt, and interest burden is like 300 crores per year. So, things are bad. On top of it, management is very reticent. They do concalls, but are shy of giving any future numbers. But are there some hopes for the future?

They have recently got their 500 crore commercial paper rated, so I think they will be able to continue without dilution.

The way I understand, BSNL is key for 2027 revenue. I think the lack of PO is because they have no budget for 2026. The budget will likely give them space for releasing funds and the PO. BharatNet too will start coming in 2027. I think we should see bigger numbers that in FY24 but lower than in FY25. However in 28-30 is when a new capex cycle in 5G and 6G will perhaps start. That is also the time when BharatNet will end and Kavach cycle should be at peak.

I cannot comment on the valuations as of now and the work continues. However, it looks like we might be trading at 20x 2027 PAT, which seems to be fair value to me. Will try and do some more work on that and post.

Disclosures : I have recently started buying Tejas Network shares, and will perhaps continue to buy in coming weeks. I am biased and above information is not a recommendation. I am not a SEBI registered RA and above is not investment advice.

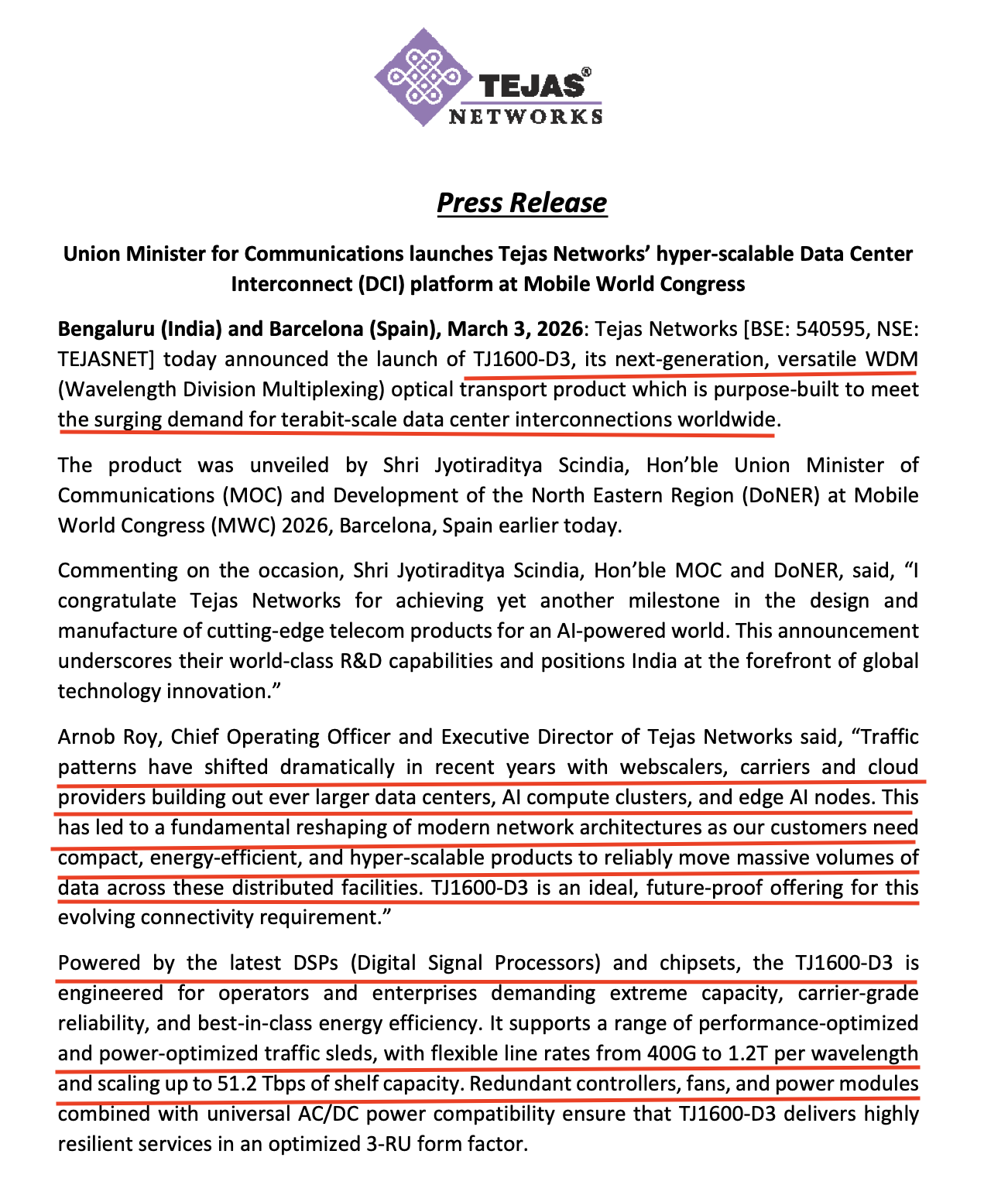

Tejas Networks has been on steroids in the last week. For the lows of below Rs 300 it is already breached 480 levels. In the Q3 investor call , they mentioned their intention to go inside the hyperscaler data center ,besides their capability in networking between Data centers. Below is their most recent filing regarding launch of DCI platform in the World Mobile Congress in Barcelona

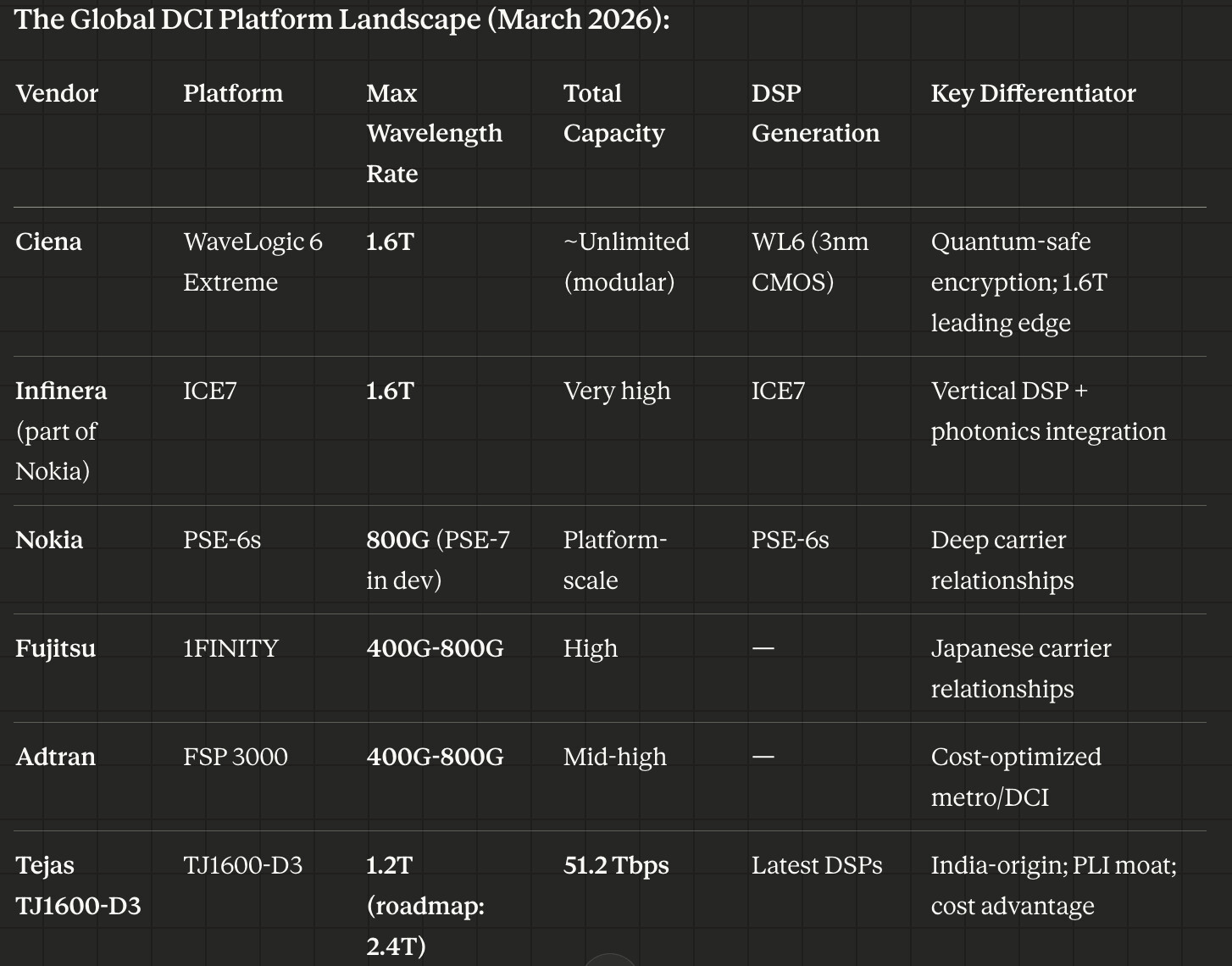

Please find below a capability comparison (AI generated) between TJ1600 -D3 with other global competitors.

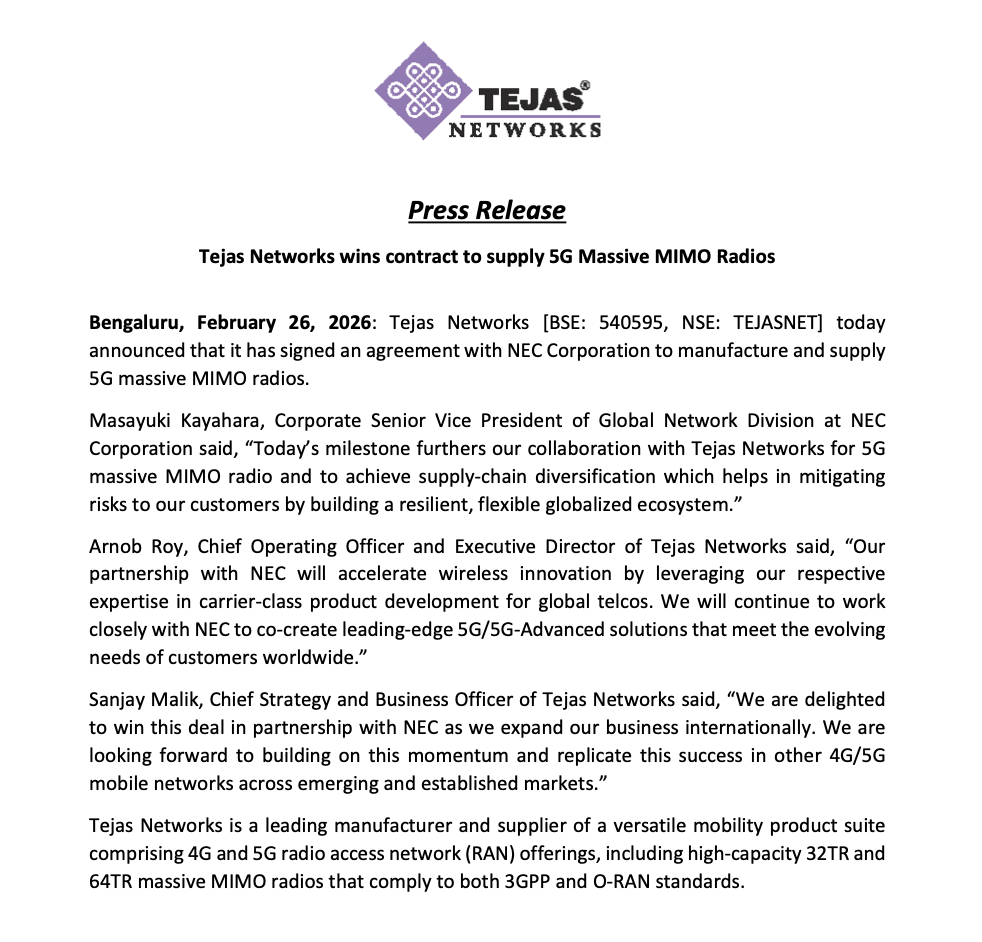

Recently Tejas came out with an announcement of tie up with NEC to supply 5G wireless Massive MIMO radio equipments which is also significant. This too was highlighted by the management in the concall (Iminent tie-ups with NEC and Rakuten).

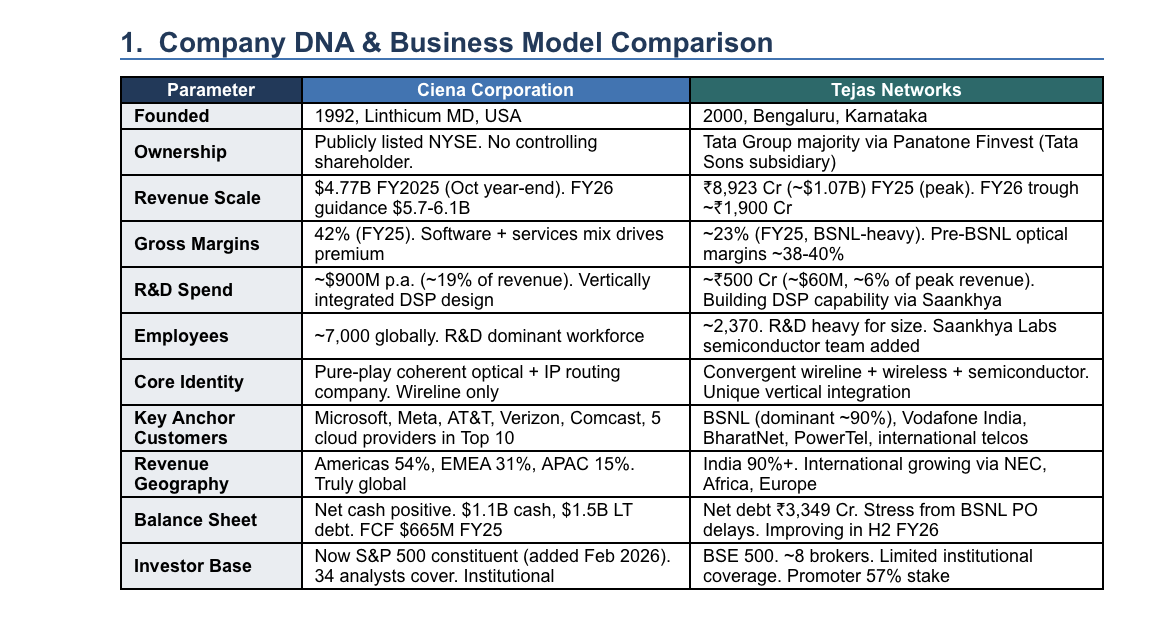

Attaching a research report (AI generated) , which talks about Tejas with its parallels to networking giants in the US like Arista networks, Ciena (8x in 2yrs ) .

Tejas_Networks_Research_Report_March2026.docx (36.1 KB)

Request domain experts to pitch in and share their views .

Disclosure: Invested recently, have been tracking for many years. Invested previously also and had exited at a loss.

Although tracking passively, it seems it had fallen badly as no revenue visibility and revenue crashing after earlier orders ran dry…it started rally after NEC news maybe because of some revenue visibility…btw its scary to see such huge fluctuations in revenue. I liked this company brcause of obvious Tata connection, decent tech in hardware infra/digital but last Q revenue huge crash and volatility kept me away from it so far… What are your & others thoughts on this huge revenue volatility and future stability, if any?

I maybe wrong in my assessments & not eligible for any advice.

Sir, kindly share the prompt if possible ![]()

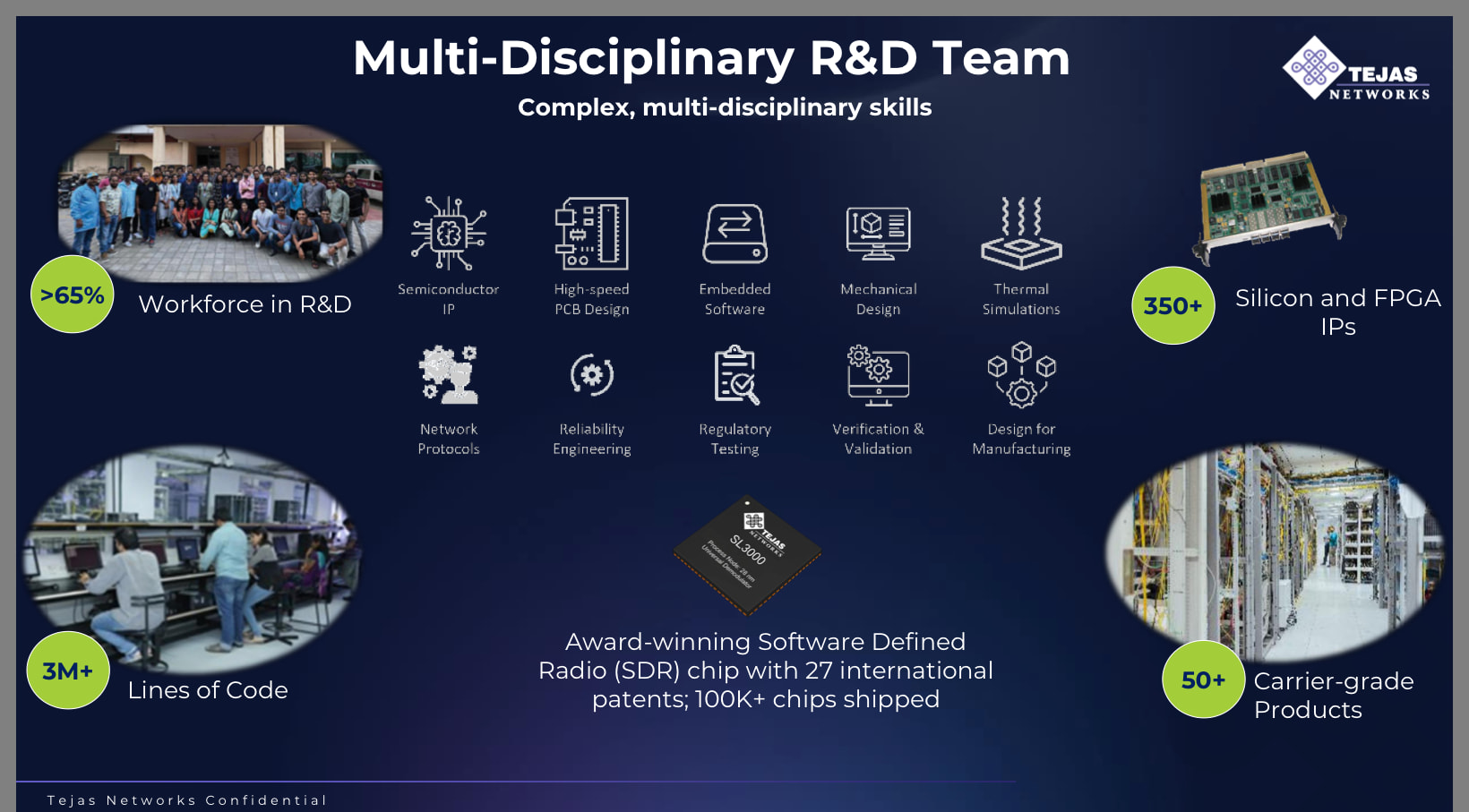

Buying Tejas is a leap of faith based on the capabilities, the patents they hold. How many companies do we have in India with > 65% of workforce in R&D ,meaningful numbers of patents and IPs.

While the market thus far has been valuing it basis the BSNL order or the lack of it , in recent times I feel they are considered as an AI and Data Center proxy . Tejas themselves considers Ceina as their closest business in the wireline space. Ceina is up 8x in last 20 months .

There are not many AI and data Center proxies in India and the obvious ones like MTAR, AEROFLEX , Sterilite etc have run up quite a bit in the last 30 - 45 days .

P.S : Please do your due diligence . This is a high risk bet with high probability of failure as revenues this quarter also might be a washout…