Hi Sarthak,

I am no expert on taxation. But my understanding for the low taxes is due to 2 reasons:

- Company is paying MAT

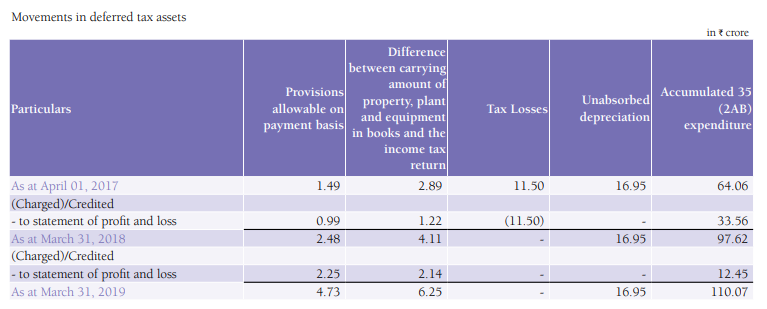

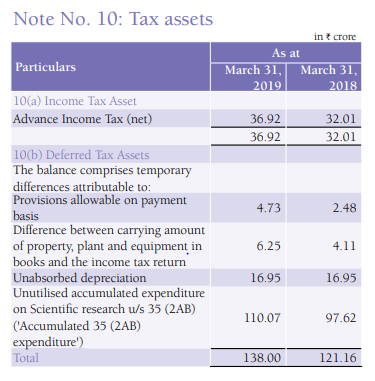

- Deferred Tax Assets accumulating from R&D Expenditure and Previous Year losses (FY15 and earlier)

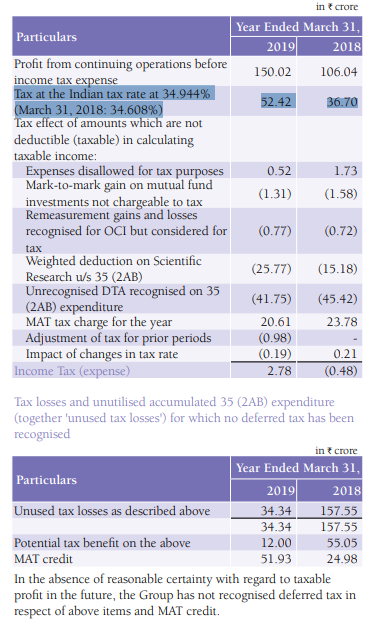

Attaching excerpts from FY19 AR

The Group has recognised deferred tax assets on brought forward depreciation losses and accumulated 35 (2AB) expenditure. The Group has estimated that the deferred tax assets will be recoverable using the estimated future taxable profits. The unabsorbed depreciation and accumulated 35 (2AB) expenditure can be carried forward indefinitely as per Income tax law and the Group expects to recover these through future taxable profits

Despite the P&L showing negligible taxes, they have accounted a reasonable cash outflow for it on the Cash Flow Statement: