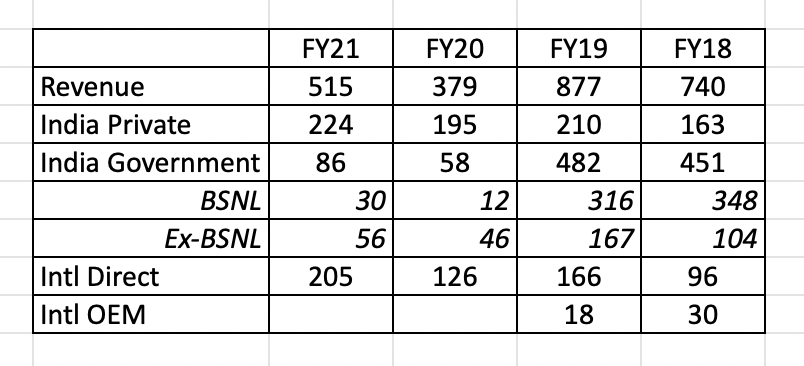

Tejas revenue split over last 4 years, India Government business is split into (BSNL and ex-BSNL) →

-

As mentioned before, India government business fell off clip from 482cr in FY19 to 58cr in FY20.

-

It is good to see run rate of 200cr business with India private. With some order wins and Huawei exit, we need to see if this business can double in size in next 2-3 years.

-

International business has also reached the size of 200cr+ in FY21 and management expects this business to growth faster than other businesses to reach 50% of the revenue. International business has bettor DSO and better margins.

Company used to do International OEM business till FY19 but that business has gone to zero now. Scale up in International direct business is exciting. -

The order book at the beginning of FY22 is ~680cr and management has guided that 50% will get executed in FY22. If I find the order book split in above segments, I will update.

International and India private orders get delivered in 8-12 weeks and hence orders executed within same quarter do not show up in order book.

Let me talk a little bit about FTTH business now.

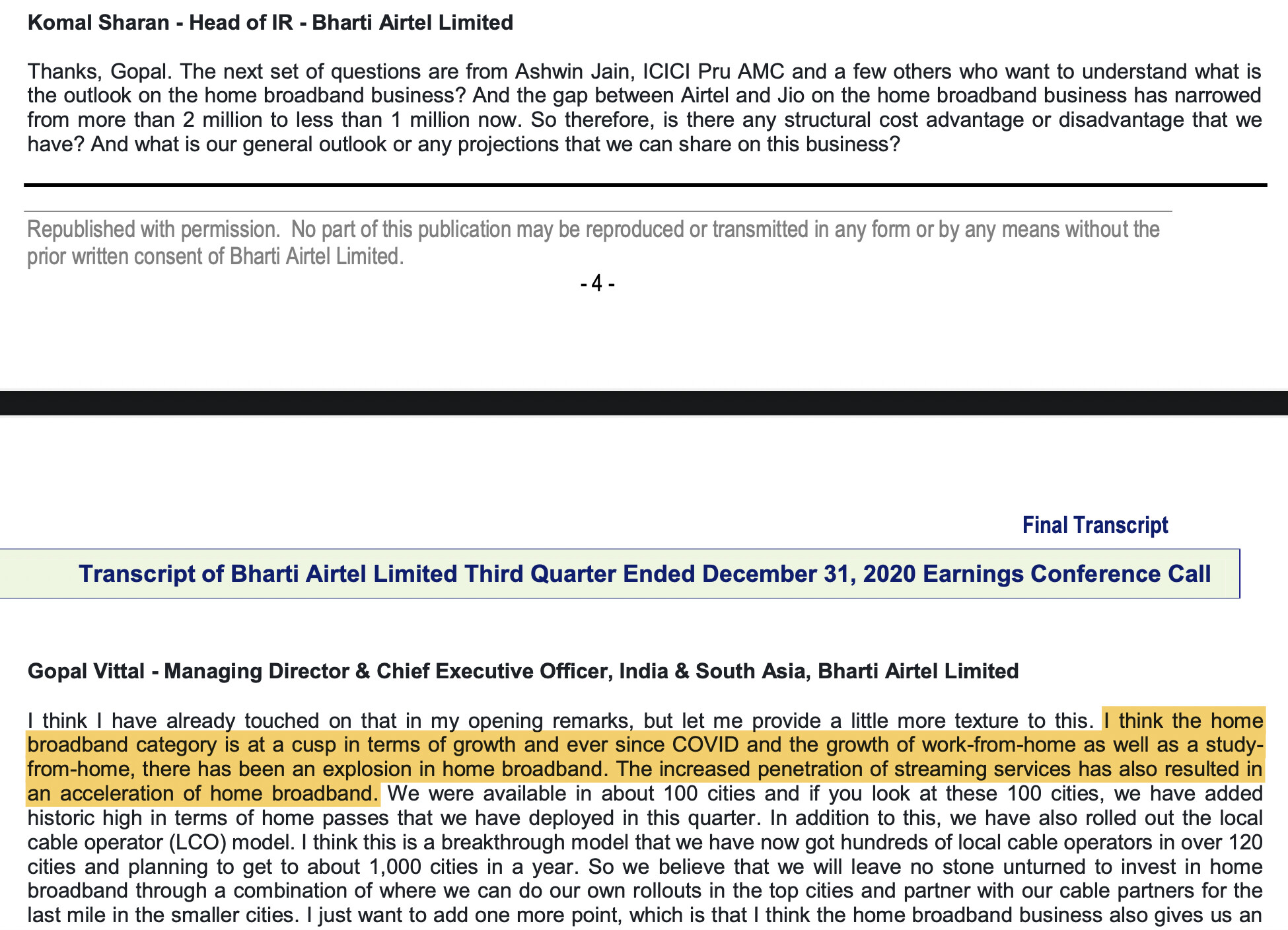

From Airtel Q3 FY21 Conf Call →

In home internet business, entire copper infrastructure will be upgraded to FTTH. How big of an opportunity is this?

Airtel being bullish on home broadband growth →

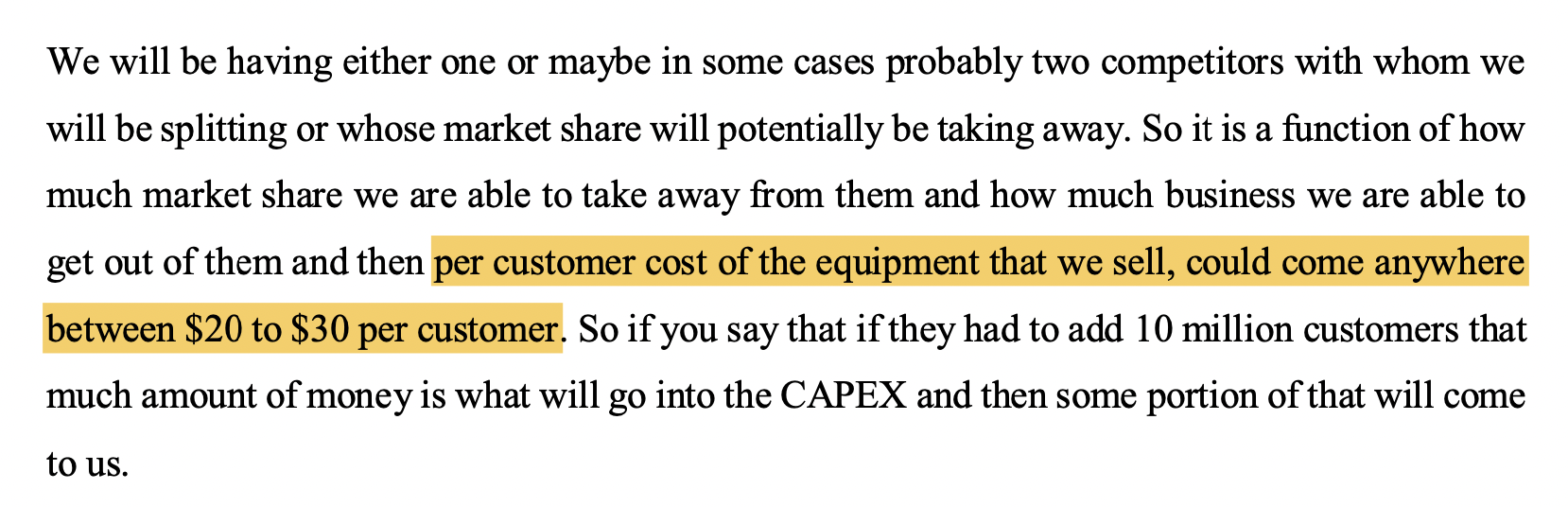

Tejas Q2 FY21 Conf Call, per customer equipment that Tejas can sell in FTTX is 20-30$ per customer. If 10mn customers get added over next 2-3 years, opportunity size comes to 200-300mn$.

Larger operators usually buy customer premise equipment directly (like Jio Fibre) and hence smaller opportunity size for Tejas. Smaller players buy both - infrastructure as well customer equipment from Tejas.

Will do another set of posts on customers and deal wins (all 3 segments), Backhaul/Metro/5G and also product comparisons as we go along.