PP Gupta from senior management had given a bullish commentary on revenue guidance. FY 23 will have about 1250 cr topline with 500 cr for Q4 projected. This essentially means, Q3 will be 350 cr abouts.

FIIS have increased stake, so have the promoters. These are good signs as well.

I did some more digging into the operating profit martins for a Data Centre Infra company. Equinix seems to have about 15-20 percent OPM. However, they are operating in developed markets, all outside India.

Does anyone have an idea what operating margins are being made by Indian market players in DC space? I tried getting data for CTRLS but nothing comes up. I am guessing the margins could be higher.

● Due to supply side constraint, this quater had revenue problem. EPC business should not be judged on QoQ results.

● Revenue guidance cut by 100 cr. For this year.

1000-1100 Cr. Revenue guidance against 1200 Cr. earlier-

●Q4 will be about 500 Cr. Revenue - best for the company

● Guidance of 1600 Cr. EPC Revenue for FY24 , & target of 2000 Cr. By Fy 25

Next 3 years will be best for the company.

● Guidance of 14.5% operating margin going forward

● Company has 1200 Cr. Cash/ Cash equivalent ( 110 rs/ share ). Payout/ buyback from cash surplus will go up higher & our investors will be rewarded well in the future.

● On wind power sell - Sold wind power asset at 80% purchase value, after 12 years of use. - that was the best possible deal.

● You will see magical growth in this company! - Mr. Gupta

● On data centre - First datacentre (4 floor ) should be operational from sep 2023.

JV partner search for datacentre is going on. Already received some term sheets from some parties.

With guidance of 14.5% operating margin going forward, there won’t be much increase in profits since OPM used to be between 21-25% earlier. Correct me if I’m wrong.

Company didnt have revenue growth since last 5 years. However, now company is targeting high topline ( with data centre & FGD business at the centre ). Even in concall, Mr. Gupta talked about possibilities and vision of 10000 Cr. Revenue by 2030 - thats a strong call.

High receivable business of wind power is out of the way.

Even at 2000 Cr. Revenue in FY25 - it will be 300 Cr. Operating profit.

Current mcap - 2200 Cr ( ex cash/cash equivalent )

EPC business is very high ROE, which should give the company much higher multiple.

Company has lot of surplus cash, which will be very rewarding for the shareholders by means of dividend/ buyback.

Data centre business is going to be a game changer and high revenue growth driver, in my view.

All in all, if you dont have topline growth, the company doesnt get attention from investor. That was the case with techno earlier.

I for one think thay Techno management is on the right track and their TOPLINE execution is what I will be keenly watching. If company executes 25- 30% kind of revenue growth for a long time ( they are guiding for 30-40% for next 3 years ), then this is the company is to watchout for.

Agree to everything you said. Except that “EPC business is very high ROE, which should give the company much higher multiple.”.

Comparable EPC company Powermech trades at a similar TTM multiple. There too, they have big targets in the coming years. I don’t think Techno will get a multiple rerating. Having said that, the stock is showing good accumulation and made an awesome comeback intraday today. Technically looks good

Topline guidance for fy 24:

● EPC: More than 1500-1600 Cr. + data centre revenue

● EBIDTA Guidance: 12-13% for full year.

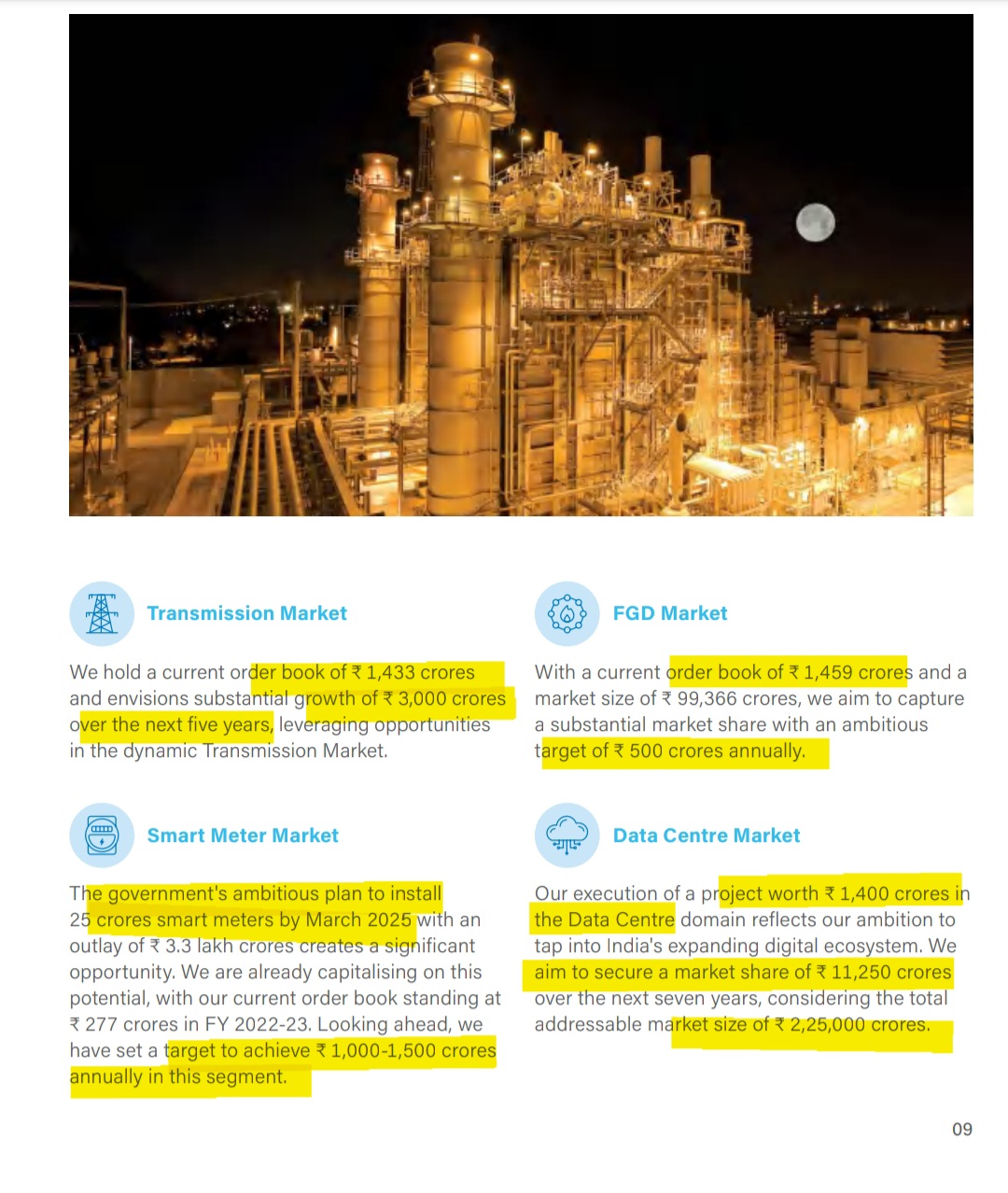

● Current Order book of 4000 Cr.

L1 status of 1150 Cr. in transmission

L1 status of about 2350 Cr. ( AMI ) For about 20 lakh smart meter installation - Jharkhand & Kashmir

Expecting another 2000 Cr. of new Orders apart from L1 orders.

Cash/ cash equivalent on books: 1500 Cr.

Phase 1 of Data centre ( Chennai ) to be commissioned by March 24

Plan to Develope 250 MW of data centre by 2030 ( include ourself & third party ) - Chennai, Kolkata & Hyderabad are some of venues for plan of data centre.

Consol. figures include expenses of Data centre & AMI, but Consolidated topline number doesn’t include AMI & DATA CENTRE revenue. So Consol. Margin looks weak.

What’s you’re rationale for being invested in this stock? If it’s because of the Datacenter tailwind then how would you compare this to Anant Raj (another big name emerging for the Data Center play)?

I have alreqdy mentionedy rational for investment in techno electric here

Apart from that, techno is a debt free ( 1500 Cr. cash/ cash equivalents ) company and data centre requires big early stage investment. So that was one of my reason for investment as well, as Balancesheet for techno should not deteriorate even after large investments.

Also please find article below which is helpful in understanding data centre.

Some points from this article…

● 5000 MW of data centre - investment of 1.5 lakh cr. expected in In next 6 years

● Predicted to grow at $ 10.09 BN in 27’ from $ 4.35 BN in '21

● Goverment providing all possible help to the sector

I havent studied Anant Raj well ( started tracking it recently ). However they also do have big plans for Data centre business.

There is enough room for growth for many companies in data centre sector in india.

KKR to acquire 20% stake in singTel’s data centre business. - Attached article.

As per article, this deal is valued at 4.03 Billion USD. And singTel is planning to expand their datacentre business from current 62 MW to 200 MW in future.

So as per rough calculation of 4.03 Billion / 200 MW, it comes around 160 Cr. / MW deal. This is a very high end deal, as generally, new data centre cost is about 50 - 60 Cr/MW in india. So there must be some kind of brand value / country specific value / some kind of long term confirm revenue value may be taken in to account in this deal. ( this is my assumption )

However, point of interest for me is that Techno electric is currently building 24 MW data centre in chennai. ( phase 1 in commissioning stage ). And their plan is to build 300 MW by 2030. Having said that One has to keep in mind that Techno may not build all datacentre for themselves and may build some of these projected data centre for their clients as an EPC player.

Even then, at current MCAP of 5500 Cr. ( debt free balancesheet, includes 1400 Cr. Cash & EPC business ) it looks like market is either not factoring in / giving very little value to their data centre business segment…

Having said that, there has been appreciation lately in price of about 30% or so, but in my view its is mainly because of their increasing orderbook in epc segment and anticipation of good orderbook in smart meter segment.

Market may be waiting for

completion of their first phase of data centre to see their execution capabilities

Who will be their strategic partners in their JV & what valuations/ terms assigned for chennai data centre…

All in all, data centre business for techno electric looks good for a business rerating opportunity in time to come.

Disc: Invested since '22 ,one of my top allocation in portfolio. Biased views.

Not a recommendation to buy/ sell. Do your own research well.

Regarding company, i’ve one more investing rational,

as company mentioned in last earning call, apart from Smart meters, major focus is on Transmission. In this field, Techno has great experience and will be fastest growing vertical of company.

With 1400crs cash equivalent , Billing of Data -centre and Robust order book, it can be a good candidate for re-rating apart from growing EPS.