TBO Tek Ltd

A) Company Overview:

TBO (Travel Boutique Online - http://tbo.com/) was founded by Gaurav Bhatnagar and Ankush Nijhawan in 2006, both of whom are Joint MD of company. Since then, TBO has evolved from a single-product air ticketing company into a leading Top 5 global travel distribution platform. TBO did IPO in May 2024 and got listed at MCap of ~ Rs15,250cr. Price has corrected by -15% since IPO.

| Market Cap | Rs 13000cr | D/E | 0.12 | |

|---|---|---|---|---|

| P/E | 59.5 | Debt | Rs 136cr | |

| EVEBITDA | 35.5 | Cash/Investment | Rs 1450cr | |

| P/S | 7.5 | OCF/PAT | 150%+ | |

| Div Yield | 0% | Promoter % | 44.4% |

TBO provides a B2B Travel platform/portal that connects Buyers and Sellers of ‘Travel Inventory’ like Hotels, Airlines, Car Rentals, Rail, Transfers, Tours etc. ‘Buyers’ are often local or regional Travel Agents, Travel Advisors, Tour Operators, OTA etc. ‘Sellers’ are owners/operators of Hotels, Airlines, Car Rentals, Cruises, Tours etc. TBO’s travel APIs facilitate connectivity and enhances efficiency across its network. They have a modular architecture that supports the integration of new travel products and enables expansion into new geographies.

TBO primarily focusses on ‘Outbound/International’ travel in the countries it operates, with minimal contribution of domestic travel within that region. TBO tends to operate ‘locally’ in a region/country to provide best offering to the local travel agents & operators. It has created a standard ‘playbook’ which it replicates when entering new territories, gain traction and then have its local leadership drive growth. They provide access to 10lac+ Hotels & 750+ airlines to 1.89lac Registered Buyers on their platform facilitating 1.32cr transactions.

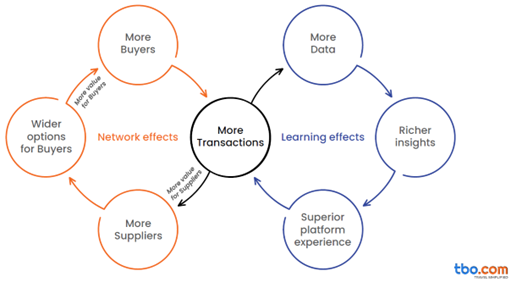

TBO does have some network effects as it onboards growing numbers of ‘Travel Buyers’, which attracts more ‘Suppliers of Travel Inventory’ to use its platform. But one needs to moderate expectations on this ‘moat’ since the ‘network effect’ is likely not as strong as that of BSE, NSE, Airbnb, YouTube etc. TBO has modest customer stickiness which is reflected in its customer retention rates. Business is asset light at its core as most investments are in technology and employees. No major PPE is needed making it relatively easier to scale. However, cash will be sucked by acquisitions as inorganic growth is part of strategy and nature of industry.

% of Retained Travel Buyers

Period: Retention

5-7yrs: 35%-40%

3-5yrs: 40%-60%

1-2yrs: 70%-100%

B) Financials, Business KPI & Growth Strategy:

Though Sales growth appears high, it is facilitated by frequent acquisitions. Without acquisitions and post Covid-19 travel boom, organic growth would likely have been <18%pa. Business has strong profitability but one needs to monitor its track record for longer term.

| Growth | TTM | 2yr | 5yr |

|---|---|---|---|

| Sales | 24.7% | 27.8% | 25.0% |

| PBT | 21.0% | 25.6% | 25.5% |

| Profitability | Min | Avg | Max |

| OPM | 6.6% | 14.2% | 19.1% |

| NPM | 6.0% | 11.2% | 14.5% |

| ROE | 14.5% | 26.7% | 42.4% |

| ROCE | 20.7% | 53.4% | 38.3% |

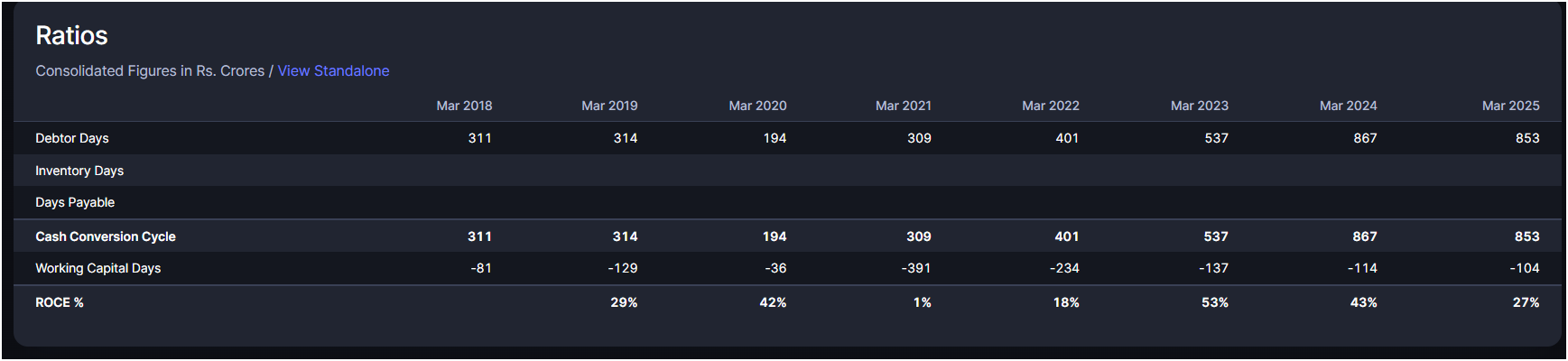

Note: Above calculations exclude Covid19 lockdown period of FY21 since it distorts data. TBO’s revenues tanked by -75% in FY21 during Covid19 lockdown period and company reported operating losses at OPM of (-15%)

| KPI | FY22 | FY23 | FY24 | FY25 |

|---|---|---|---|---|

| Revenue | 483 | 1065 | 1393 | 1737 |

| GBV-GTV (Rs Cr) | 10257 | 22324 | 26536 | 30832 |

| Take Rate (Sales/GBV) | 4.7% | 4.8% | 5.2% | 5.6% |

| # of Active Agent | 37037 | 42220 | 45029 | 48986 |

| Annual GBV/Active Agent | 2,769,393 | 5,287,541 | 5,893,091 | 6,294,043 |

| # of Bookings (cr) | 1.03 | 1.48 | 1.6 | |

| Value/Booking (Rs) | 9958 | 15084 | 16585 |

Core KPI of ‘# of Active Agents’ grew only 6.8% - 8.8% over past 2 yrs. Take Rates improving due to increasing share of Hotels segment.

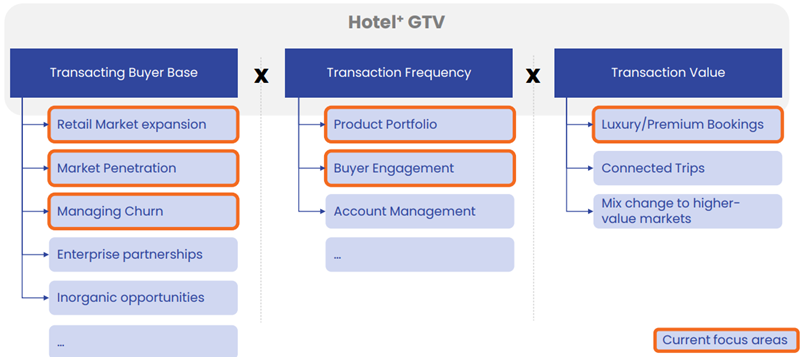

Unit economics of TBO are as follows;

- Revenue = (Take Rate) x (GBV i.e.Gross Booking Value)

- GBV or GTV = (# of Bookings) x (Cost/Booking)

- (# of Bookings) = (# of Buyers) x (Bookings per Buyer)

- Cost/Booking = Function of ‘Travel inventory supply’ and ‘Industry demand’

One could deduce that Key Variable to attain growth & scale is ‘# of Active Buyers/Agents’, which is where TBO management are focusing their efforts. This can eventually lead to improvement in Bookings/Buyer. However, considering TBO is tapping global markets, it will be hard to grow ‘# of Active Buyers/Agents’’ at 10%+ on long term basis. Remember that not all parts of the world (eg Tier 3 & 4 towns) are fertile grounds for tapping vast number of Travel agents who assist budding international travelers. As a result, ‘Organic GBV’ growth has been modest at 10%-15% and rest is coming from multiple acquisitions.

TBO’s Take Rates have been healthy, but will likely stay <9%. For comparison, Airbnb’s Take Rates are ~13%.

| Type | Take Rates |

|---|---|

| Hotels | 7% - 7.5% |

| Airlines | 2.5% - 2.7% |

| Total | 4.5% - 5.5% |

International Hotels segment offers most profitability to TBO. Hotel contribution in GTV terms is 59% (FY25) v/s 50% (FY24) and in gross profit terms is 84% (FY25) v/s 78% (FY24)

| Region | % of GBV |

|---|---|

| Europe | ~33% |

| Middle East | ~27% |

| India | ~13% |

| Latin America | ~10% |

| APAC | ~9% |

| North America | ~8% |

Most growth in ‘Active Buyers’ is from international regions which are more profitable than India. Europe market scaled up very well for TBO as it invested in regional languages, local currency payment capability and more localization when building its Buyer/Supplier network. Latin America and Middle East have been growing decently in recent times. But ‘Take Rates’ are better in Europe and N. America v/s Latin America and Asia. India has higher number of Travel Buyers, but their contribution to GBV is lower at 13% owing to low ticket size. Mgmt wants to keep Take Rates competitive to maintain existing buyers while attracting more to TBO platform.

Due to some level of operating leverage, asset light model and technological innovation, PBT growth > Revenue > GBV growth > Active Buyers growth as GBV/Active Buyer can potentially increase over time. TBO however tends to pass on most of price benefits to Buyers to maintain their patronage. To control costs, TBO has been building inhouse AI and Automation features/capabilities on its platform which will aid efficiency over time. Of the total ~2100 staff, around 300 engineers work in ‘Technology/Data/System/Engineering’ teams to support the enhancement of TBO platforms/portals.

Organic growth is primarily driven by on-ground Sales teams who go around a city/region signing up new Travel Agents/Operators/Advisors & Inventory suppliers. For remainder of the growth, TBO resorts to acquisitions as is evident below.

| Acquisition | Year |

|---|---|

| Island Hopper | 2019 |

| Gemini Tours & Travels | 2021 |

| Book A Bed | 2022 |

| Jumbo Line | 2024 |

Few acquisition criteria that management discussed in calls;

- Adds more Travel Agents to Buyer base

- Adds more to Supply base (eg JumboLine)

- Can be in any country or region

- Needs to be decently profitable and available at good valuations

C) Industry & Competition:

Global travel industry is massive at ~ $1.5tr and growing at 5%-8% pa. Due to social media influence and status signaling (Instagram, Twitter/X, Facebook etc) international travel is expected to grow at higher clip than in the past. Information availability has also provided tailwinds to industry.

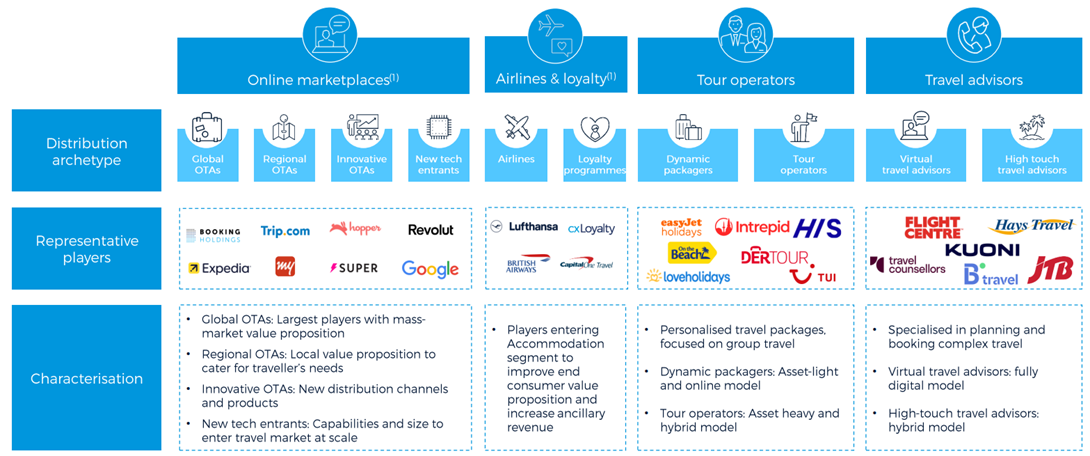

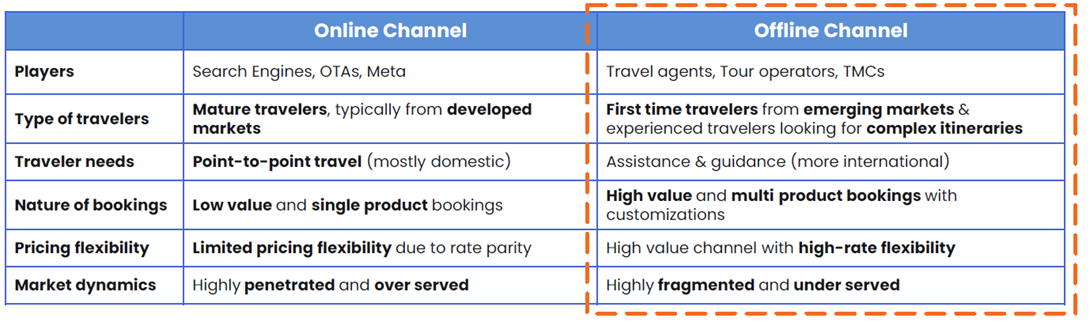

Though becoming a monopolistic market leader is tough, it is a huge playing field for a nimble and efficient company. Industry is very fragmented with 50,000+ Hotel providers and 5000+ Airline carriers. Add to this Airbnb Hosts and things swell up quick. Largest OTA has <5% share and Top 10 OTA only have < 10% of the market cornered. Online channel is super competitive due to huge number of global and regional aggregators (Priceline, Booking, Orbitz, MakeMyTrip, Travelocity, Google, Yatra, Agoda etc). While experienced ‘economical’ travellers prefer OTA, 1st time travellers or travellers needing customized trips outsource planning/bookings to Travel agents and advisors. TBO serves the later segment where competition is relatively low and booking value is high.

Direct major competitors are HBX Group ($8.7bn GBV), Expedia’s Partner Solutions, Web Beds ($3.2bn GBV). Other regional/local peers are Miki Travel, Restel, GO Global, W2M, Yalago, Didatravel, Travco etc. Largest player HBX Group recently did IPO and is valued at $2.45bn with Revenue of $721mn at P/S of 3.4x. In comparison, TBO is trading at more than double the P/S multiple (7x) of largest direct competitor. HBX however did report PBT losses, while its OPM is ~40%+

D) Promoters and Corporate Governance:

Founders Gaurav Bhatnagar and Ankush Nijhawan are 1st generation entrepreneurs in their late 40’s. Ankush has bachelor’s in business administration, with major in marketing and minor in psychology from Bryant University. Gaurav holds a BTech in computer science & engineering from the IIT-Delhi and had worked at Microsoft. Based on background, it appears that Gaurav handles the Technology/Platform aspects while Ankush takes care of the Business growth/Sales/Advertising responsibilities at TBO.

Since public domain track record is fairly recent, one would need to wait more time before making conclusive judgements on the management quality, capital allocation, shareholder friendliness, execution capability etc. But kudos to founders for scaling the business to Rs1700cr Sales in ~20yrs. Based on earnings call, they have been giving reasonably clear answers and seem to have good grasp of the business & industry.

E) Risks:

- Travel is a discretionary spend and gets severely impacted during economic downturns or just general unfavourable climate. TBO’s revenues tanked by -75% in FY21 during Covid19 lockdown period and company reported operating losses at OPM of (-15%)

- Travel industry is cyclical in nature and as such Q1 and Q3 are weak quarters. Q4 (1 qtr post Nov/Dec holiday period) and Q2 (1 qtr post summer vacations) are stronger due to higher travel incidences

- Since TBO is primarily into Outbound/International travel, this is an expensive activity for an average family globally. As such, gaining quick scale can be hard and company maybe limited in the areas it can tap for demand.

- Global Travel industry is highly fragmented with tons of players across the value chain and gaining or maintaining dominant market share organically is hard. Industry experiences relatively higher levels of entry/exit of players, but those in top quartile have a decent survival rate.

- Companies resort to acquisitions as is evident by Booking Holdings, HBX Group etc. Between 2019-24, TBO has done 4 acquisitions, and this trend will likely continue in future. This exposes the company to risks related to acquisitions like low base rate for success, overpaying, integration issues etc. Acquisitions will eventually bloat the Goodwill portion of balance sheet as well.

- Since TBO is a Tech player in Travel industry, it will be at risk of technological disruption and rapid changes in how Buyers/Sellers connect to transact travel inventory eg: Airbnb was able to cause a decent dent in the Hotel industry + Hotel OTA and Turo is doing similar to Car Rental companies in US.

- Since ~85% of business occurs in USD/GBP/Euro, company has natural hedge. For rest, TBO does basic forward contracts. However, TBO will be exposed to forex risks if not managed properly.

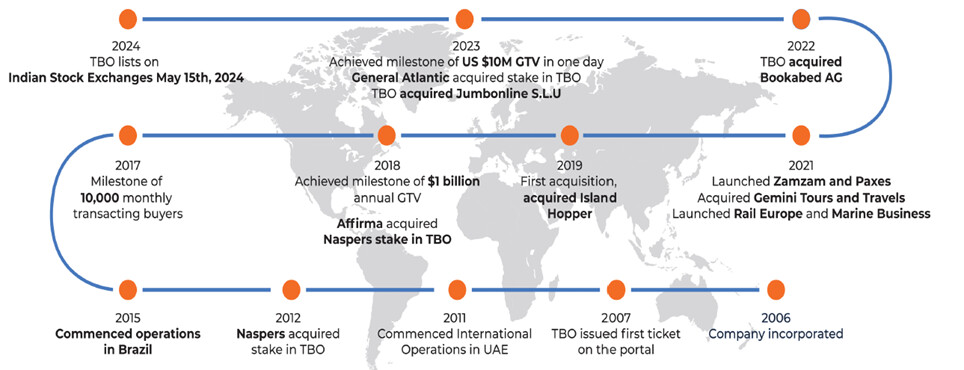

TBO’s journey so far:

F) Sources:

https://investors.hbxgroup.com/English/overview/default.aspx

Disclosures: I am not a SEBI registered analyst and above post is written solely for educational and discussion purposes. Please do not consider any content in the post as investment or financial advice. Numbers, calculations, insights and inferences are estimates and written from a learning perspective using information available across multiple sources. Please conduct own due diligence before investing or making decisions. I do not own this stock at the time of writing and am researching the company.