based on my limited understanding, MF had no tax implication from this merger (as against retail investor who were facing significant tax) hence they probably didnt intervene. As to the merger ratio, I think the discount narrowed to 30% only after merger was announced…so they didnt have much to complain on that front either.

3 Likes

According to this article, only Tata motors spokesperson, PWC, Citi and Axis capital, all funded by Tata motors, feel it is fair deal ![]()

The article says otherwise with these points…

-

The retail investors and mutual funds are set to get a raw deal in the proposed conversion of Tata Motors DVR (differential voting rights) to ordinary shares.

-

The public DVR holders and mutual funds will lose about ₹15,568 crore and ₹3,000 crore of economic value, while the promoters will gain 1.4 per cent economic share valued at about ₹5,000 crore, per the April 18 closing price.

-

Post conversion, the promoters holding in Tata Motors will increase to 42.62 per cent from 41.23 per cent, while that of public will slip to 57.38 per cent from 58.77 per cent.

-

Both type of shares have equal economic right and after accepting that DVRs have traded at sharp discount due to absence of proper market, the company has taken the market approach to ascertain higher weightage for ordinary shares, said Sivakumar R, a retail investor.

-

Globally, the shares with reduced or no voting rights trade at premium or about the same price to ordinary shares. For instance, the class C shares of Alphabet (Google) with no voting rights trades at a premium to ordinary shares.

Anyway it is not very intelligent to cry over spilt milk. This is just a lesson learnt that Tata group is no Saint either.

5 Likes

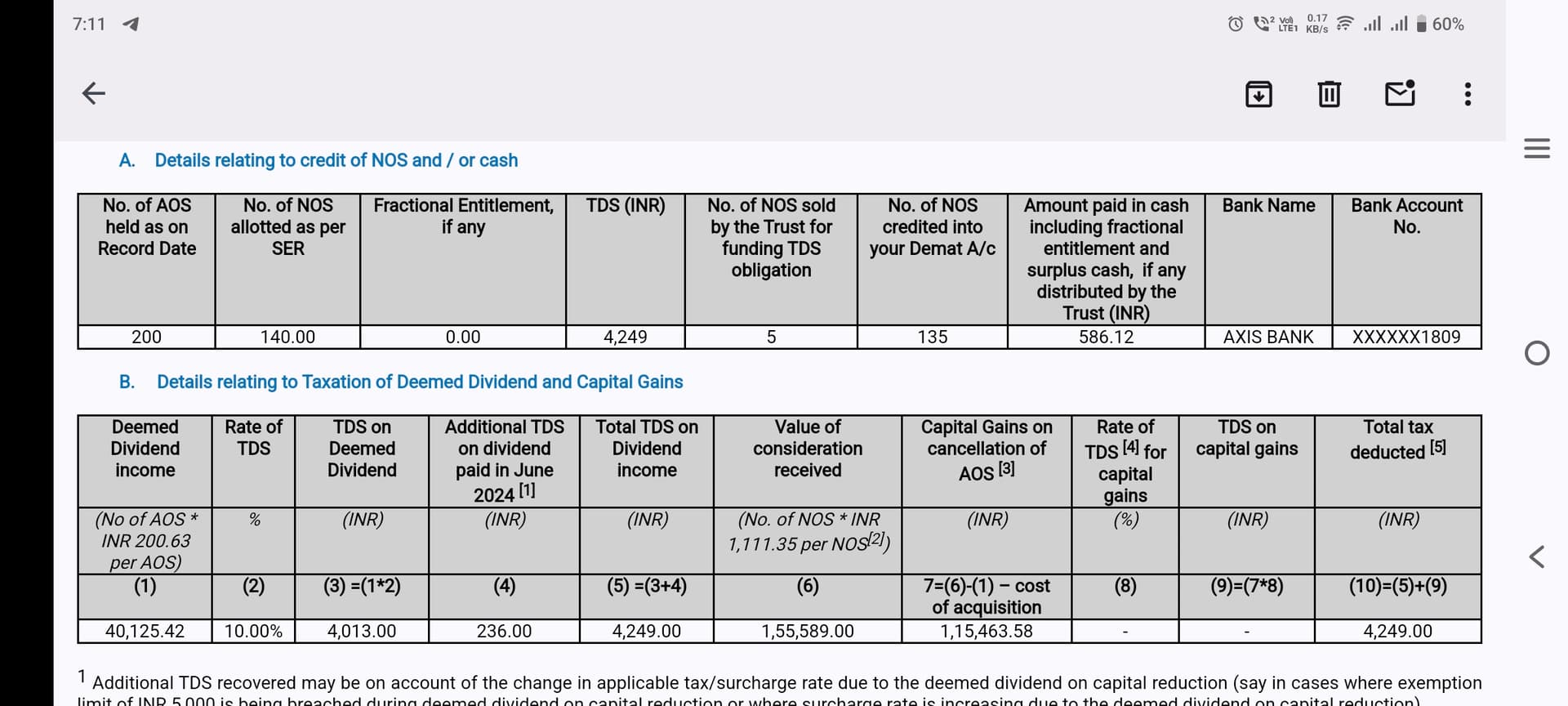

I had 230 shares, they credited 155. What’s the calculation here? It shd be 161, right?

It is to pay the TDS on deemed divident,for the conversion of the shares from DVR to main shares.To pay the said TDS, Tata Motors very going to sell the shares equal to the TDS amount. Please refer the excel shared by tata motors earlier.

Tata motors should share the exact calculations hopefully as profit as the delisting day is not disclosed.

2 Likes

I think part of the reason that nobody is talking about unfair price of DVR is because most people including mfs bought when there was 40-60% price discount so when they gave 7:10 ratio, they happily accepted it. Not saying it’s fair but seems like that’s the case.

The biggest con was taxation on deemed dividend of 200 or so. For 35% bracket, effectively means I am paying 70 bucks for each on conversion from DVR to normal. That brings conversion ratio to 60%…

1 Like

Net swap was put at 68.1% to pay for TDS - a tax incidence created on retail investors by swap scheme (technically this swap was designed as liquidation)

1 Like

All,

Quick question…

Has everyone who had opted for DVR swap (not sold in market) received email confirmation of swap and shares credited to demat?

Just that I haven’t - i am still awaiting email confirmation and new shares in demat

Shares credited in Upstox. Held 230. Shares n got 155 credit. Mail or excel calculation not received

1 Like

There would’ve been an email sent to you abt this before the whole process initiated.

There is a problem with ICICI Direct because I still haven’t received the shares in my demat account, and Tata Motor DVR is still showing in my demat account. Can someone help me?

New shares are seen in my sharekhan demat account. But I didn’t get a confirmation email. I too wanted to ask this here yesterday.

The below article explains nicely everything about the share swap but it assumes 200 per share as deemed dividend. The last trading price of dvr share was 768. Dividend of 200 is 26%, this is insane.

2 Likes

Yes, I too received similar mail with lot of details. 26AS will be available once tds is deposited.

Does it mean you need to pay tax on applicable tax slab on 40,125.42?

1 Like

Looks like flat 10% from the screen shot

That is TDS, not actual taxation ![]()

1 Like

check demat holdings ,not the stock portfolio page. It will appear in demat holdings. I do not know the proess to remove from portfolio page. May be icicidirect doesnt know it either,because this sort of event has taken place for the first time.

2 Likes

Yes. You’re right. Somewhere around 14k+ at my tax slab. This is the fees I need to pay for being long term investor in DVR share.

Over that, I also have other LTCG as well. So I have already breached the miniscule 1.25L limit. The entire sale proceeds will be taxed at 12.5% for LTCG.

So the absolute returns is not much ![]()

2 Likes

You will get some setoff on LTCG against the deemed dividend calculation. Check the sample calculator they had shared before the conversion…it should help you arrive at right tax outgo.

However, at an overall level it still is a lose lose situation for retail investor who held on to DVR vs selling before conversion.

4 Likes