I too noticed the same thing few months back , when I was choosing which one to buy amongst TATA motors and TATA motors DVR. I bought DVR considering the greater fall and expecting higher rise . As far as I know the difference is voting rights only. Sooner or later it should move in line with TATA motors and generate higher returns than TATA motors.

The fact that the DVR shares have 5% higher dividend rights, so once the company starts paying regular dividends, it can even command a premium to the ordinary share.

Barring voting rights there is absolutely no difference between the regular and DVR shares. In the Indian market may are not very conversant with it, DVRs are treated as untouchables. 40% discount is too large for DVR. But if someone has a long term outlook, it’s fine to expect the differences to even up to a good extent.

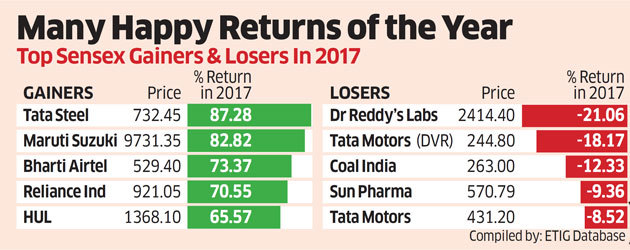

Thank you guys for responses. These thoughts reassure as I am still positive on this story. My initial buy thesis remains. But I overpaid and on loss, then I saw that my decision to go with DVR. So far returns were negative and got amplified due to DVR as my notional loss is higher than what it would have been if I had purchased Tata Motors shares. See the attached pic shows the loss in DVR for 2017 is 18% vs 8% in Tata motors.

Inviting your views on bull case and bear case.

I know that I don’t know much and this forum was very helpful. But I do not see as much interest in this counter by many. I hold this considering recent setbacks of last 2-3 years especially in domestic market are transitory in nature and Tata under the new chairman and pruned/renewed management focus will bounce back.

My effort to reduce stocks in my PF, brought back focus on this story, so was trying to understand better.

“Watching out for stocks like Tata Motors, SBI , Larsen and Toubro, M&M , Bharti for leadership. After long time would have to focus a bit more on largecaps”

Nooresh the technical analysis expert considers it as a big contra bet of 2018 and I assume if Tata motors outperform, DVR would be outperforming better than main stock.

I did not very closely track monthly sales metrics of Tata Motors, so I cannot tell for sure if it only due to last years demonitisation effect or not. Experts, please enlighten on that.

November sales:

October growth was only 5% in terms of numbers. But this two months figures may indicate good quarter results from domestic front.

Liquidity cannot be a concern if you rely on valuation and ignore market mood swings.

In case of dividend, it is a common issue for both ordinary and DVR shares. One can not expect a company to pay dividend and lose 20% in DDT when Debt:Equity ratio is 1.3 unlike Maruthi, M&M,Eicher,etc., which have negligible long term debt. Tata motor should concentrate on repaying debt even if cash flow increases in future. If one is not willing to buy tata motor DVR, there is no logic in buying ordinary shares, paying 70% higher than DVR. Also, for a legitimate promoter like Tata group, does voting right matters?

DVR shares are common in US markets. Companies like Berkshire and Alphabet have DVR shares listed. Take an example of Alphabet, there is hardly an discount in class C shares, (which have no voting rights) compared to class A shares, although class C shares are clearly inferior compared to class A shares, as the underlying value is the same. In the case of Tata Motors DVR not only the discount is egregiously high but i don’t believe that the shares are inferior as the voting rights are compensated by 5% higher dividend. As the company has been making standalone losses it has not been paying dividend. So in my opinion the price of DVR should at least be equal to the price of ordinary shares if not more. I think the anomaly will correct over time, when people will develop liking for Tata Motors in general. As people are pessimistic about the business in general, the discount has just become larger.

JAGUAR LAND ROVER reports muted growth for the current quarter and reports good sales from China, "But we are facing tough times in key markets such as the UK where consumer confidence and diesel taxes will hit us.”

Disc: Have started buying Tata Motors DVR and intend to add more

I am not getting into detailed financials as that is available in public domain.

I want to look at this as very high level valuation exercise as market seems to be mis-pricing future opportunities.

It is JLR’s electric vehicle i-Pace which seems to have already achieved a booking of 20,000 vehicles and is likely to give a tough competition to Tesla. This compares very well with Tesla selling 30,000 every Q.

Now Google has tied up with JLR to launch a driveless version of the vehicle, and this will be Google’s premium driver less car.

Tesla has a MCap of 50B USD. Assigning even one-tenth valuation to Tata Motors for i-Pace makes it approximately 30,000 crore.

Now at 1.13 lakh crore TataMotors+JLR+Investments-Debt itself appears undervalued valued due to concern around JLR future volumes. Let us not forget that even Ashok Leyland is valued at 43,000 Cr and Mahindra at around 1 lakh crore.

So, i-Pace just seems to nice optionality on already undervalued stock.

I think Tata Motors is a fairly valued stock.Their elevated debt levels also provide no relief.

Instead of a comparison with Tesla a fair comparison would be with manufacturers like Ford or General Motors. On those parameters the valuation accorded is fair.

That is why I am talking about “Optionality”. If i-Pace were to do a volume of 5000+ every Q, market will accord it a suitable valuation. Google backing can be a powerful driver.

Not sure you track Biocon. Market re-rated it from Tier2 generic company to BioSimilar company in just 3-4 Qs.

Electric vehicles sector is definitely going to be one of the most promising sectors in coming years for stock investors. In the Indian market,Tata motors and Mahindra & Mahindra are the front-liners. Maruti will begin in 2020,and I think that may be a bit late,because the first mover advantage will go to M & M and Tata motors.The question in my mind for months is which among these two. M & M is also going for many collaborations (Ford,CIE etc.). Hence, I think a little more research required before betting heavily.

But what I wanted to highlight is Tata Motors’ JLR emerging as a Tesla competitor with Google’s backing in US market. This can be big. Tesla is valued at 50B USD and does around 30k vehicle every Q. Google itself intends to buy 20000 cars over next two years. Now if they clock same volume from other sources over next 2 years, we are talking about 5000 every Q.

We should also consider the possibility of car ownership going down over the next decade. And, I’ve personally witnessed people decide against spending money on a car and commuting by pooled cabs.