This is my analysis on Tata Motors :

TATA MOTORS

Tata motors today = JLR+TML+TMF (Tata motors finance)

80% of Revenue comes from JLR, 12% from Commercial Vehicle and 6% from

Passenger Vehicles. Rest from TMF.

KEY PERSONS

Jaguar - Mr. Thierry Bollore (CEO)

Passenger and Electric Vehicle Business- Mr. Shailesh Chandra (President)

PB = 3.3

Mcap = 1.6 Lac Cr

MARKET SHARE % = 13.84%

Concall Highlights (12th Oct 2021)

In the past few years, the industry has been growing at the rate of 1.5x to 2x every year

since FY17 and this year we are expecting the industry to grow by 2.5x to 2.7x.

Reasons: 1. Favorable govt incentives 2. Launch of better EVs 3. Hike in prices of ICE

vehicle along with fuel prices

We started with a 11% market share in FY18 and now it’s 71% which is still limited due

to supplies

There is a very steep increase that we are seeing in the demand, but we are fast trying to

ramp up and catch up on the supply side versus the demand

Demand drivers that we see is one, the stringent emission norms from 2022 April, we are

going to see the introduction of CAFE which will drive all the OEMs move towards

electric vehicles to offset the emissions coming out of the ICE, so that itself will create

some push factor

We have planned for introducing 10 electric vehicles by FY26 in the next 5 years which

would be in different body styles, in different price points from affordable EVs to EVs with

higher range, more sophisticated technologies and on the sales and marketing side, we

are also going to increase the micro markets where we are present today as you saw that

today we are present in 60 cities, but we will continue to expand every year into more

cities, also as we are introducing more electric vehicles and different models.

We are coming with more options to access the EVs through subscription model which

will allow those customers who are still vary to adopt the new technology an option to go

for a 12-month or a 24-month subscription

Subsidiarization of the PV business is confirmed by 1st of January next year, that

will be fully operational and that is done with a focus to actually to ensure that we are

able to drive a differentiated focus between CV and PV

PV strategy is to win sustainably and with that in mind we had called out in our investor

day as well that we definitely want to go after a double-digit market share which we are

happy to confirm, we are there, high single digit EBITDA, which is still a journey, we are

progressing well and we want to be FCF positive by FY23 which again we are progressing

well.

EV will require at least to begin up investments, 16,000 crores plus kind of investments

will be needed over the next 5 years and PV will definitely be fund constrained to support

this aggressive EV aspirations

Helios is the project name for this transaction. First, create a pure play EV company to

focus on passenger mobility. This will be created as an asset light subsidiary of Tata

Motors, will house all the dedicated EV talent and design capabilities of TML and we will

really aim to attract top notch global talent into this particular company

We will want to leverage the existing PV assets and investments to drive efficiencies as

well as drive speed to market because this we need to ensure that we stay ahead of the

curve on this one and the PV company will therefore be a toll manufacturer, we will

provide all the services to EV company to make it stand up on its feet

PVCo will become a 100% subsidiary of Tata Motors in January 1st 2022.

EVCo, the new company, we have not yet named it, will focus squarely on the future EV

products, will build and own the future IPs of EV and we will also catalyze the creation of

the charging infrastructure in the country

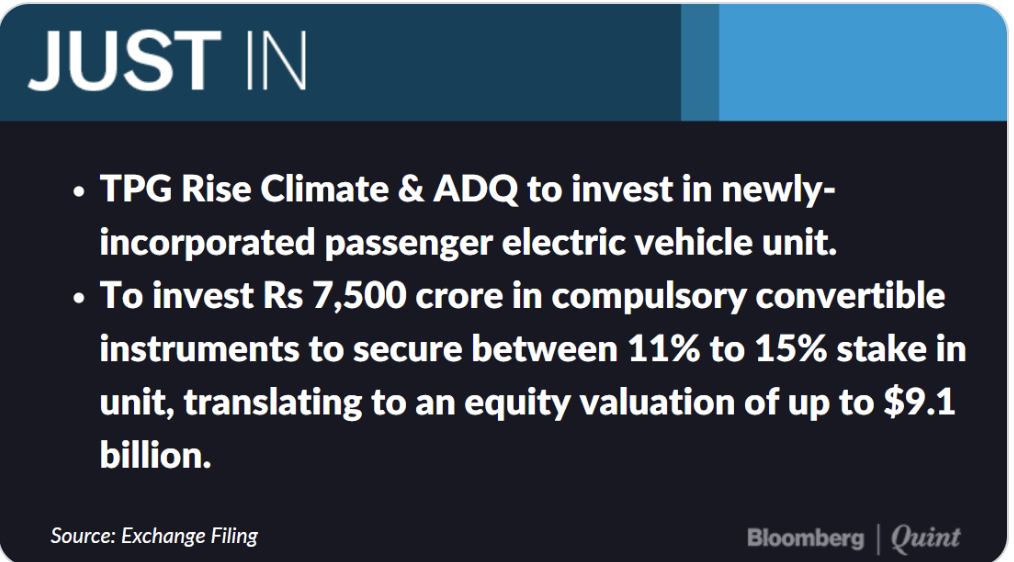

External investors will take 11% to 15% in the Company and we have Tata Motors Listed

Company having the ownership of 85-89% in this company

TPG Rise Climate which is a new fund of TPG Rise will be investing a billion dollar at a

valuation of up to 9.1 billion

It is $1 billion equity funding, where TPG Rise with a commitment of Rs. 7500 crores, $1

billion. 50% of this will come by March 22 subject to post conditions being met and also

post set up of the EV company, one of the conditions prevalent as well and the balance

50% will come by Q3 FY22 on achieving Go-Live actions

For Tata Motors, we have specifically taken a target of penetration of 20% plus with the

10 products that we are planning to launch in the next 5 years

Revenues in the region of about Rs. 500-600 crores and we aim to hit an EBITDA

breakeven in this business next year

What is actually happening is a full access to the full PV ecosystem in terms of factories, in

terms of sales points, management bandwidth, design, all that is going out, their brand,

name plate, everything, so therefore we are actually wanting to use everything that has

happened in Tata Motors and gives EV its full support to ensure that it is able to take off.

EV valuations globally work on a different logic and we had Morgan Stanley and JP

Morgan as our advisors and we had put the overall business plan in front of them and of

course there was a view in terms of what could be the kind of valuation that is there, so

comparable multiples have been used. It is comparable with East Asian peers.

Next 5 years, I already answered this question a while back. From an industry

perspective, the EV industry in India is expected to be in the early double-digit

penetration as what we expect. From a Tata Motors perspective, we are aspiring to be

20% plus

Total investment in EVCo = Rs 16000 Cr

As far as batteries are concerned, right now, we have already localized the backend

module in India and this is being supplied to us by TACO. Going forward, as far as cell

manufacturing is concerned, it is something also which is under consideration by the Tata

Group and that decision will be taken

Even if subsidy goes away in the next 2 to 3 years, it should not impact because by that

time, the cost structure would have come down significantly

No asset, no liability moves from Tata Motors PVCo into EVCo, it is an asset light company

Comments:

- As of now there is no near competitor in EV segment. In future also Maruti has declared

that they are not launching any EV based vehicle by 2025 at least.

- Demand supply gap as of now which will increase exponentially in future due to multiple reasons like high fuel cost, stringent norms etc.

After the investment by TPG the structure now looks like this:

DECODING THE VALUATION

The analysis shall be based on TPG investment of 1B$ for the stake of 11-15%

which brings the valuation of 9B$ which comes approx . INR 67500 Cr.

Some Facts and Figures

EV Car sales in 2021 = 4% of total car sales in numbers

In terms of Revenue = 3.75%

Let’s say 4 % which is 1/25th of total PV sales.

Now TPG is valuing this 4% segment, as of now, to Rs 67,500 Cr.

Whereas Total MCap of Tata motors (100%) is just 1,60,000 C r which includes

EV+PV(with brand lik e Jaguar)+ CV!

Comments :Huge Valuation gap considering the fact that Jaguar ’s revenue = 80% of total

revenue

Now by 2025, EV = 20% of total PV sales (as per Tata motors target)

P/B of TM = 3.3

Whereas P/B of Maruti = 4.5 with no EV plans by 2025

PE of Maruti = 50 with decreasing car sales and no futuristic plans

Now by 2025, TM EV’s MCAP will be = 5 times current Mcap = Rs 3,37,500 Cr (as per their target)

PV+CV in 2025 = 2 times current value = Rs 3,20,000 Cr (growing at normal rates)

Total Mcap = 6,57,500 Cr

Which means it shall be 4 times appox. in 5 years in earnings and assuming Tata motors

meet most of its targets, its PE re-rating will be definitely on cards to at least double of current

or say past value which makes total M cap = 8 times of current value.

This is the min. value as per Indian market and if in future Tata Motors EVs compete with the

likes of Tesla then PE of 100+ is also reachable easily making its value 16 times of current

value. Needless to tell that EV industry itself will be at least 10-20 times by 2025.

This is with assumption that TM will not take any significant market share from the market leader

which may happen looking the recent trends and hence it can take a huge chunk from Maruti

in future.

Charts and figures attached in my analysis as attached here:

TM Valuation.pdf (1.1 MB)

Disc: Invested

In that case, as Tata motors is talking about being Net debt free by 2025, that means the Market cap can virtually catch up with EV by that time (if they are able to take off that much debt from the BS), right??

In that case, as Tata motors is talking about being Net debt free by 2025, that means the Market cap can virtually catch up with EV by that time (if they are able to take off that much debt from the BS), right??