https://twitter.com/ETNOWlive/status/1699680342775582865?t=u5LImc0RSoatVmYUaUwGGA&s=19

Sebi new consultation paper for holding companies, some interesting points

Thanks

https://twitter.com/ETNOWlive/status/1699680342775582865?t=u5LImc0RSoatVmYUaUwGGA&s=19

Sebi new consultation paper for holding companies, some interesting points

Thanks

Here is one interesting tweet discussing the possible reasons for the suden upmove in Tata Inv

https://x.com/iKrishnaAppala/status/1726574056936513797?s=20

Hope you find it helpful

dr.vikas

Is it worth to invest now as discount shrieked close to 25 % and if they want to liquidate all holdings that may cost taxation of around 20 % , please advise .

Discount is very low which does not merit buying at all. Company has said nothing on liquidation.

Is there a specific reason except for the results for this move, it’s going above its book value ?? Don’t understand how can that be , anyone is aware or has a thesis??

Today, I sold my largest holding in my portfolio, which I had held for over three years. The reason for selling was that the discount had narrowed to almost nil and the largest holdings held by Tata Investment Corporation, such as Titan, Trent, Tata Consumers, etc., are very expensive, which in turn made this stock even more expensive to hold. Although I was hesitant to sell at the time, I may have been emotionally attached to this scrip. Now, I am looking for alternative investment options for the proceeds from the sale.

I was holding these shares since 2011, It has never touched the number that i saw today and hence after deep thoughts i decided to part ways with the script today. I am hopeful that it will give me another opportunity to jumpin. That being said, I don’t see any reason for the stock to move up except momentum and i cant understand that, hence the decision.

Book value shouldn’t be applied to measure valuations of holding companies like Tata Investment Corp. Better way to value them is to calculate the market value of their total investments (in both listed and unlisted companies) and then apply say 20% discount to that to derive target market cap of Tata Investment.

I did this calculation before listing of Tata Tech and found the stock to be overvalued which I guess got addressed after bumper listing of Tata Tech. Today’s price move of 20% could be something to do with valuation trigger in of one of their unlisted companies that may not be a common knowledge.

Same thing. Divide the total market value by total outstanding shares and that gives you the book value.

That’s not how you derive book value of a company. Sorry to state the obvious but in case you don’t know, book value is your asset minus liabilities (or equity capital + reserves).

Tata investment market cap is 27584 crores while its book value is 23000 crores. If you divide them by outstanding shares you get current share price and book value per share respectively.

In my opinion, stock might enter heavy distribution phase soon. Price has gone above book value. Even after considering all the unlisted investments they have, this is still highly irrational. No other holding company has shown this kind of run up.

Disc. Not invested.

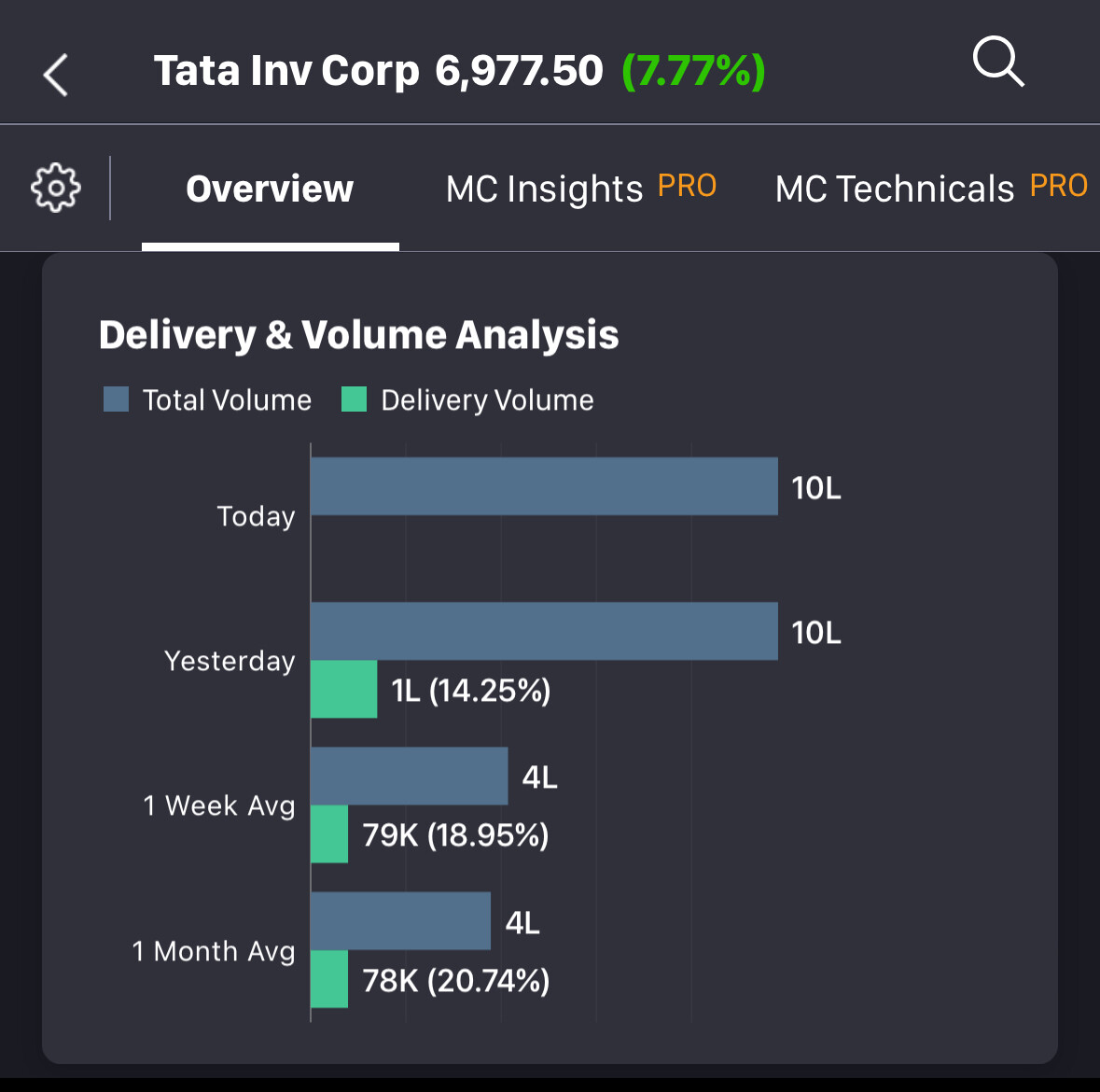

Considering such huge volumes and positive closing, something interesting is going on that we retail investors are ignorant about

Just a personal opinion

Disclosure - Invested and Biased. The average price is 2800.

Maybe some news on Tata Asset Management is possible as it owns 32% in TAM.

No other reason i can think of.

This is really interesting. Most of the trading volume is in intraday and delivery volume has been consistently dropping. Seems like a clear case of stock manipulation by generating artificial demand considering the float is low. The next few weeks should present some answers. The stock can’t keep going up forever.

Just a wild guess.

Is this the reason for the recent run-up in Tata Inv ???

Again just a guess.

What is our leaning here, I don’t know , I was holding this stock for 13 years and sold it at all time high , not only that considering holding companies valuation we sold it at a considerable high valuation yet the stock moved 2x from there, I just wanted to ask the community what is the leaning , no regrets just want to know how can we learn from this ?? What should we consider in the future ?

I am on the other side of the spectrum. I bought TICL a little over a year ago and sitting on ~5x return whereas my return expectation was 17-20% (HoldCo Return = Underlying Portfolio Return + Dividend Yield ± HoldCo Discount). So fundamentally I got 9/10 year returns in a year.

I think I got lucky and due to some bad luck. Now when that bad luck strikes is anyone’s guess.

Although there are a few triggers which market participants are giving certain weightage (less or more, time will tell):

Maybe a few more unexpected +ve triggers on the upside perhaps. maybe!

My current rationale from the portfolio level is to trim the position (soon) from purely reducing concentration risk. However, I think it’s prudent to hold since there’s nothing that fundamentally has changed i.e. it’s still an optimal way to index the TATA group of companies (my primary thesis) which still pays around 80% of earnings as dividends (a bird in the hand is worth two in the bush).

But definitely, CMP is over the top and due for some correction (as I mentioned I am due for some bad luck anytime).

Please correct me if I made any wrong assumptions above. Happy to learn and course correct.

Disc : Invested from early 2023 levels (position size here). No transactions in the last 30 days.

I recently sold a small portion to avoid concentration risk and bring down the position to below 10% of my PF. However, since the underlying fundamentals of the stock hasn’t changed, I will continue to hold till the proposed IPO of some its group companies plays out.

Disc: Invested.

Kind of same pinch from my side. It has become a 5 bagger from initial purchase price and 3 bagger on my average holding price. Now it has become 25% of my total stock holding.

All the returns of future years are baked in for sure.

But one should know the recent meteoric rise in share price ( 2 continuous 5% UCs). We retail investors may be missing something.

I still think it has to do something with the Tata’s semiconductor business. Otherwise it’s very difficult to explain such rise in share price of a HOLDING company.

Though it has become 25% of my stock portfolio, still its less than 5% of my total net worth. So as of now I am not willing to sell it. But this thinking may change in future.

Just sharing my personal thoughts.

dr.vikas

Normally when Tata plans to venture into new business, it needs capital. So it asks cash rich companies to pay dividend. Foray into Semiconductor will need lot of capital. Some of it has to come from internals. So If companies pay dividend then Tata Investment will play pass through.