For Q3FY18, excluding Russia, revenue from operations grew 3% YoY, attributable to improvement in India and UK with underperformance mainly in non-branded business.

Everyday Black Tea category declined and retailer pressure continues in developed markets.

As per Nielsen data, Tata Global Beverages (TGB) is gaining traction in volumes of tea business—45% of total tea consumed is unbranded and the company expects some shift.

Within the domestic branded business, volumes have improved. Post GST, growth has been in high single digits or double digits in a few months.

UK’s market share continues to expand, predominantly in non-black tea category.

In the Starbucks JV, total number of stores stands at 106. From six cities moving to seventh city—Kolkata. Top line run rate of INR3,000-3,500mn p.a. Starbucks JV is now EBITDA positive.

Nourish Co achieved break even during the year.

Exit from China, restructuring of Russian operations and internal restructuring have been completed. Divestment of holding in its associate EMSPL, Sri Lanka in Q3FY18, was part of the company’s overall strategy.

Yes, but I am not sure if that merger would actually happen. The results have been very subdued for past 3 quarters even though everyone was expecting good results. It’s still more of a commodity business than an FMCG one. It gets affected by crop produce, rains, etc. which does not make it a consumer business. The Starbucks story is going to take a lot of time to make a noticeable impact on bottomline or even on the topline. I am very critical about TGB, they have a very good company in front of them and they should make good efforts to grab the opportunity. Saying so, I am keen to get on this stock but I want a valuation cushion. The cash position is bad, 50% of which is in goodwill. I think I am positive on long term but it still is a risky bet. I might enter around 200-210 levels if it corrects that much otherwise I will simply pass. Let me know if there are any other views from people invested and interested.

TGBL is a good company with a good product basket. Product and market rationalization is happening, but a bit slowly in my opinion. That has been the problem with this company for many years. It has over-promised in terms of potential but nearly always under-delivered.

We need to keep tracking the Starbucks JV and also how they are able to improve overall margins.

Disclosure:

I am a SEBI Registered Research Analyst - Registration Number: INH300006607

I have booked profits earlier but continue to keep track.

@basumallick Could you please share your profit booking strategy ? Though I am holding TGBL from Rs 125, I didn’t book the profit when it touched Rs 300+ .

There is no easy answer to this question. Strategy varies from stock-to-stock and also on my conviction levels. So, I have been lazily holding some stocks for 8-10 years and others where I have sold within the year. In addition, I sometimes consider technical cues into consideration.

Disclosure: I am a SEBI Registered Research Analyst - Registration Number: INH300006607

Sir Tatas have had few JV in consumer space and they ended up in them selling their stake. If Starbucks performs excellent but the big daddy from US decides he has had enough of Tatas JV and want to go full throttle on its own or for any other reason puts pressure on Tata and they end up selling their stake and get decent cash but end up buying another Tetley - Is my biggest fear for this company, considering its management’s past. However, being an optimist I have been holding it since almost 8 years, did not sell a single share at 300+ and looking to add more near 200. Not sure if I am doing the right thing though…Why I do it is because I see huge potential for this business in India, only if I get he right management and vision. Pls let me know your thought on above and specially Starbucks JV long term future. (Btw this JV has equal stake, I think none has a majority stake here)

Starbucks is present in 130 odd cities in India (its a 50:50 stake). Most important thing is that all cities are profitable.

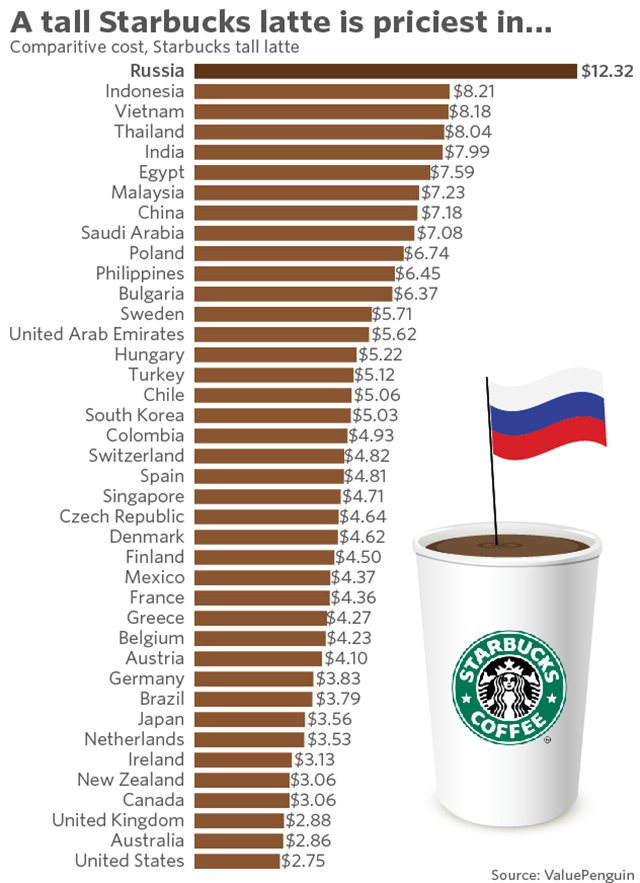

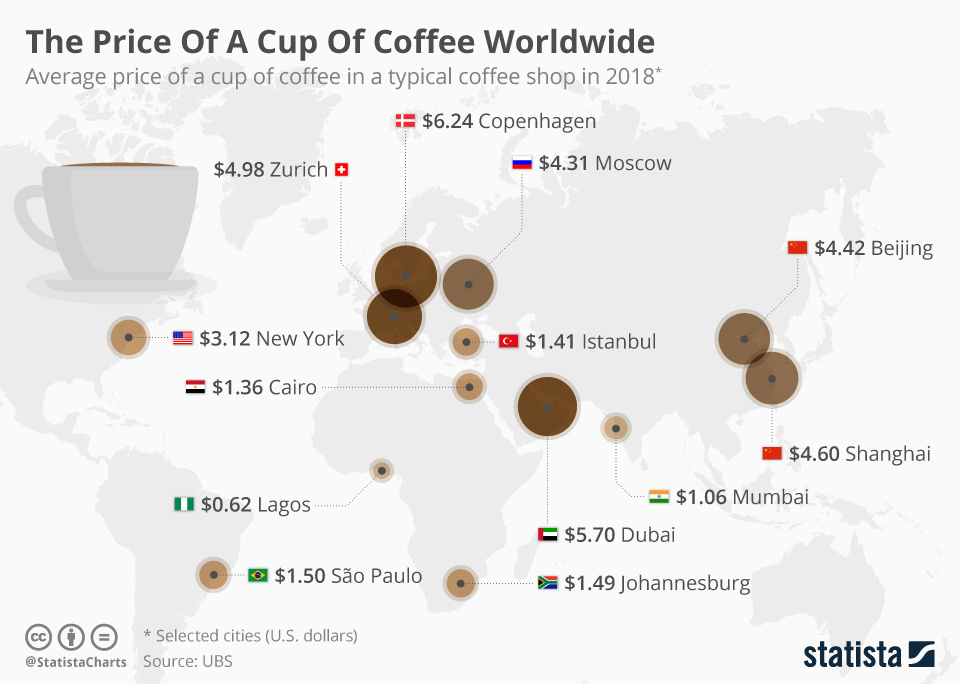

With the kind of cities Starbucks is present in currently and the density in some of them I am not sure how would the sales/footfalls be increasing. This is more so because an Indian doesn’t buy a Tall Latte from Starbucks for breakfast as in the US but rather for a meeting/passing time/hanging out. Also a cup of coffee is quite premiumly priced in India when compared to other geographies.

The explanation given to Analyst’s yesterday was that these are premium brands in Rajasthan market ,having market share of 6 %,where as Tata Global is having only around one -one & half % market share there.Further it seems they got this on very favorable terms.