very interesting read on tasty bite from stalwart advisors

http://stalwartvalue.com/tasty-bite-eatables-turning-tastier/

very interesting read on tasty bite from stalwart advisors

http://stalwartvalue.com/tasty-bite-eatables-turning-tastier/

q1’17 results uploaded. awesome no sales up approx 60% n eps by more than 150%.

Disc : Holding 3% plus of portfolio

Brief write up on Tasty Bite in today’s ET - Gaining some visibility.

This is clearly the kind of reporting that does not add any value with a possibility that gullible investors may get trapped. I am not sure who the analysts are (I wish there names were mentioned), I am not sure what analysis they have done and arrived at 100% growth trajectory. Although the company as a whole has done very well but the sales growth in QSR has been tepid in last 2 years and as far as I know this management never gives out forecasts.

The best way to get information and reach a conclusion is to read the AR attend AGM and the best thing to do with such articles is to ignore them.

Discl: Invested. More than 10% of my portfolio.

@Anant When i see PAT margin improvements from sub 5% to 8,5%, i see falling inflation benefits (55%+ COGS is inflation related if i am not wrong) and economies of scale contributing to it. I am not able to model how much of margin expansion can be contributed to inflation which would/may be cyclic and how much can be sustainable. Also, I remember somehwre in annual report they have mentioned that they would be ensuring COGS stability through contracts. What is your view on PAT margins? Any way to dig for sustainability of margins from inflationary perspective. For next few years , hopefully with falling inflation, this should not be an issue

Disc: Invested more than 3% of portfolio

From what I understand the company does re-negotiate contracts with the QSR folks (mainly sauces and frozen foods). These re-negotiations happen once a year and in some cases if the fluctuation is very high it can happen mid term. So on an average the QSR supplies cost are mostly pass through and the management does not work below a certain threshold gross margins.

On the packed food side I do see some impact of crude (packaging) and raw materials along with operational efificency combined.

The management did say last year that they are working more towards value additions and recipe discoveries in their R&D Kitchen and this should contribute to higher margins.

Ya, main concern is towards export to parent holdco.also, off late , I realized in fy18 there would be doing preferential share redemption. Need to understand this in terms of impact

Not sure how much of a value addition it would be but I could not resist myself from commenting here as a consumer of tasty bites ready to eat packs. Being a graduate student here in New york, I like to sometimes get something quick from the supermarket near my campus instead of cooking from scratch. If I estimate correctly, I must have already spent more than 300$ in the last 6 months, eating tasty bites ready to eat packs. And sometimes I have to buy in bulk because some of my favorites get over so quickly.The supermarket is very slow in re-stacking their supplies. From what I understand, there is no alternative I could rely on if I have to eat Indian food. I wish there was some competition as a customer.

PS: Missed the rally completely. Could have applied “buy what you see” strategy to get handsome returns. Not invested.

Thanks for the feedback Nishant. Can you find how your other mates mainly the Americans find them? In a discussion during last year’s AGM they said there sales to the diaspora is very less and they do not position themselves as an Indian foods company but as an ethnic food company. Also how is your feedback on Kitchens of India, Haldiram, MTR etc.?

In another discussion the company said that their complaint response time is one of the fastest in Industry. Did you get a chance to try that?

Anant, I could do some scuttlebutt asking the cashier how many Americans buy the same products. I personally go very late night (the supermarket is 24*7) to buy so I don’t encounter many American shoppers buying the same stuff.

I stay in upper Manhattan where the nearby supermarkets (3 of them which are close by to the Columbia campus) only stack Tasty bites in the Indian curries section. No Haldiram or MTR. The taste is very “americanized” though: not as spicy as we Indians expect to our standards, but spicy enough for Americans I reckon.

I would rate MTR and Haldiram much better as an Indian because the spicyness matches my standards, but I guess Americans don’t like that spicy ( and hence no demand for haldiram maybe?)

If I have to buy haldiram products then I have to order them online through third party seller at a huge premium. Or I have to go to Long island (the most far away section of new York where more Indians live).

What I feel is that Tasty bites has penetrated those areas where there previously was no demand for Indian foods. So they must have tapped the untapped potential.

I haven’t complained anything yet gladly. hah!

PS: Special request for the amateur investors who might get excited reading these kind of posts, to take all my data inputs with a pinch of salt as it is coming a single entity. There might be huge inaccuracies.

Clicked @ Target store, Allen, TX 75002, US (couple months back).

Tasty Bite’s Indian entrées were at the top shelf. Could not find TB’s Thai entrée or Asian noodles range. No MTR and no Kitches of India around. Others include www.atasteofthai.com, www.thaikitchen.com, www.simplyasia.com, www.lotusfoods.com, www.anniechun.com, www.marionskitchen.com and Patel’s RTE.

Disc: Invested

Key pointers in Tasty Bites AGM – 19th September 2016

RTE Business

4) The consumer/RTE business has had a 21% consumer growth last year. Market shares are difficult to estimate as your market share changes depending on how one defines the market. However, as a ballpark, Indian Entrees have a 60% market share. In Organic Rice, the leader is a $250M player whereas we are probably less than 1% than the leader but growing quite fast

5) RTE business is in US, UK, Australia, New Zealand, Canada and Japan. Japan and UK are the new markets this year

6) In the RTE business, we have 4 categories (Indian entrees (oldest), Asian entrees, Rice and Spice & Simmer (newest)) across 3 channels (Grocery, Club and Private Label)

7) We have grown across all these 4x3 this year and will continue to grow in the next few years

8) There are 35,000 doors nationally available for distribution, of which Tasty Bites is present in 20,000 doors. There might be 7-10000 doors which we may not want to go (India-centric, low-income, sparsely populated etc.). We took 15 years to get to 10,000 doors and another 3 years to get another 10,000 (total – 20k now).

9) Organic rice as a segment has significantly exceeded the management’s expectations in terms of growth. It has grown across Grocery and Club – the two major channels – both last year as well as the latest quarter (Q1 FY17)

10) Spice & Simmer – a new category has just been launched and will roll out nationally by end of this year. This is a $7.99 product compared to $2.99 product that we currently have

11) The new market – UK – we have launched Asian Noodles in Grocery (Tesco) while we launched Indian Entrees in Club (Costco) and evaluating which way the market is moving

12) In Australia – there are only 2 major retail chains – Kohl’s and Wolly’s (predominant markets being Sydney and Melbourne). They had a major dysfunctional competition in the last year or two due to which all consumer brands have suffered in profitability. Things have returned to normal in the early part of this year and we are seeing very good growth in Australia as well.

13) RM and Packaging costs are equally divided (50:50)

TFS Business

14) We aim to be the Brand behind Brands. We are not a supplier but a partner. We do not intend to be in an RFP bidding process.

15) We have almost all the QSRs procuring from us. In fact, they co-innovate with us on most of the products. Due to our Chinese wall approach in not sharing product recipes between competitors, all the QSRs now have a tremendous trust in TBEL

16) We are very clear that we don’t want to do commodity products in our TFS business. Innovation and co-innovation are the only ways we can survive and have a margin accretive business. Else, there will be lots of business but no margins.

17) We are the No. 1 supplier to all the Jumbo Kings/Fasoos/Goli – all these emerging businesses who procure a lot of stuff from us apart from the well established players.

18) We design the product recipe along with the QSR partner and for products for which we design the recipe we are the sole manufacturer for those products. Although this is not a contractual obligation but this is how it works.

19) We are not satisfied with the Quality Certificates we go beyond. We want to be the gold standard.

20) Using our partnership with the QSR guys we are looking to foray into international markets.

Capacities

• RTE – 150,000 meals/day – utilization 100%. Spent 6-7 cr for a new line (brownfield expansion) which will push up our capacity to 180-190,000 meals/day. Test batches running now. Full commissioning in October

• Sauces – 8000 tonnes – utilization 100%. Kagome’s other plant (Ruchi Soya JV) has 18,000 tonnes. The management doesn’t foresee much of capex in Sauces due to this availability

• FFP – 8000 tonnes – utilization 60-65%. The focus in on getting margin accretive business

Increasing capacities in any of these three segments will not be an issue.

Conversations post AGM

On the UK foray:

The question was that management has been mentioning about the UK market for the last 2 years and this is the first time they have launched products in the UK. Why such a major slip?

Most of our products (esp, Indian Entrees) require a spoon of milk. The UK authorities don’t allow import of diary or diary related products from some countries (India being one of them). TBEL had to pull off products off the shelves post a soft launch 2 years ago. The UK authorities were ok if TBEL could import milk from the EU and re-export it. However, India doesn’t allow import of dairy (especially milk) from outside India. This led to a complete logjam and a loss of business for TBEL in the UK markets. Over the last year, the Indian govt. has given an exception to TBEL to import (albeit only small quantities) milk that can be used in products (and can ONLY be exported – cannot be sold in India). Given this scenario, TBEL was finally able to launch Indian entrees in the UK market while it was able to launch Asian Noodles (which doesn’t require any milk) slightly earlier this year.

Longevity of sales growth:

The question was – we have about 130 cr of export sales in FY16. Looking at the longer term, can we do a 10x sales in 10 years – as in, can we do a 1000-1300-1500 cr sales in the next 10 years or is our market not that big?

The answer rests on three legs –

a) Depth of old products: Our Indian entrees are our largest selling segment as well as the oldest in the U.S. We have been experimenting with various packaging options as well as tastes in the last 10 years. We have been slowly increasing the number of packets in a package from 1 to 2 to 4. Recently (over the last year or so), we experimented with a 6 packets in a package in our key markets. The hypothesis was that we would get 30% more volume and probably lose 20% of our customers, leading to an overall growth of 10% in this new package segment. However, to our surprise, we have lost only 5-7% of customers and have received a lot of positive feedback on the 6-packets-in-a-package deal. We are now launching 8-packets-in-a-package and the sales team as well as the consumer research team is looking forward to a successful launch. If we are able to sell more in a single ‘moment of truth’, I am making the customer eat more of Tasty Bites in a single purchase (which reduces my costs as well as gives me the upside of volume), and once the customer has a hang of Tasty Bites, he is never going to go back to another brand. We think we can replicate this strategy across our product range slowly in all the geographies we enter

b) New products: We have launched and continue to launch new products for our consumers. Our latest product, ‘Spice & Simmer’ – we have got outstanding customer feedback in our customer research trials. This product is priced any where between $7.99 and $10.99. If this product clicks with customers in the US/UK, this product alone has the potential and should possibly bring the entire current export revenue (130 cr). The deal however is, we don’t know which product would succeed. We thought Asian Noodles will do very well in the US, but it didn’t (it’s not like the product didn’t succeed. It’s just that the growth was not too high and because of the limited shelf space, any product which doesn’t compete well with our other products is pulled off the shelves). Organic Rice, which we thought will do decently has done very well. Asian Noodles didn’t succeed in the US but has been very successful in the UK so far (we have observed the same phenomenon in Australia as well). Ultimately, we innovate and try to create new products with the best minds. Even if one product category/product is successful, I don’t see a reason why we should not hit the number that one mentions (1300 cr) sooner rather than later

c) New markets: We will continue to explore new markets, new high potential markets to be exact. UK fits in that strategy. Japan fits in that strategy. These are all very big markets. If we can succeed with even one product category in these markets, the number (1300 cr) seems very much plausible

We have the capabilities and innovation building blocks in place and don’t see a reason why we should even see the number (1300 cr) as a big challenge.

Thanks to every one who helped compile the notes :).

Thanks Anant for the exhaustive summary - was very useful.

Top line due to QSR should increase nicely for TB

Thanks Ananth for the summary, reading that one gets a sense that TB has a long way to go yet.

UK launch alone should be a game changer as Indian food and RTE meals is a part of the cultural milieu there.

Have to wait and watch on the execution , Though that has not been lacking so far.

I have heard management is a penny pincher , hope that does not impact their R&D or lead to attrition in the R&D dept.

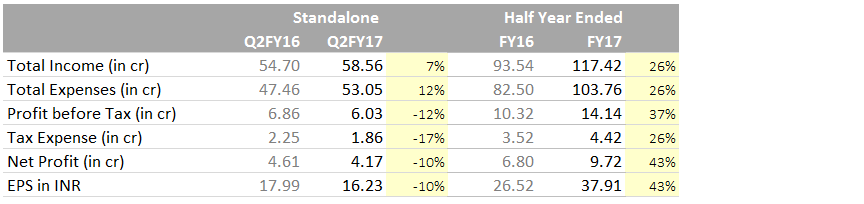

Tasty Bite Q2FY17 results out. Hopefully will trade at sane valuation now.

Discl: Holding

I also noticed a huge amount of Trade receivables of around 2500 Lakhs in the statement today. Is it normal to have such high receivables?

Revenue side:

Any idea in which quarter they would be entering into UK market as they seem to have regulatory approval if i am not wrong?

Possible to get revenue numbers of some of Indian B2B clients to get a sense. Dominos I am not counting as they are facing stangnat growth from last 4-5 quarters. This will give some indication on India b2b revenue. Considering sine of clients sales numbers mentioned above , this looks odd.

Cost side:

With food inflation going down, was expecting expenses to be on lower side (60% of cost being COGS which ideally should be food grains), so, not able to find reason why there is an increase.

As management does not hold any conference calls, is there a possibility to collect our questions, research and whatever is difficult to find, we can try to get a view from management.

Agree, it is good that some correction is happening. Post Q1 results, it had jumped from 37 pe to almost 60, total non-buy zone

Saurabh,

TB has entered the UK market. More details in the point number 11) of AGM 2016 notes by Anant Jain above.

Cheers

Oh, sorry, though, had gone through, had forgotten. then, despite of UK entry (in case they entered at the start of 2nd quarter), one reason for lower double digit revenue growth can think of is point no 20 mentioned by Ananth - 100% capacity utilization. May be that is the reason for increase in loans in Q2