Some things that stands out in business model

-

Large no of SKUs and product categories- reaching 2000 and 300+ respectively. This when seen from sub 350 cr revenue, doesn’t make entry for new entrants attractive, which in turn means current customers will likely go back to Tarsons for incremental orders. AR further emphasize mkt share and wallet share focus. How many companies can boast of newr 80% GM and come out unscathed in last 2 years of insane commodity+ logistics issues.

-

Start small and do it well before scaling big - Tarsons despite 30+ years history have not jumped all over at one go - now pushing pedal on exports( that too with clear startegy of ODM in developed mkt vs Own brands in emerging) and foray in Cell culture- thus past Tarsons opportunity size was X and now it is multiple timesof that number.

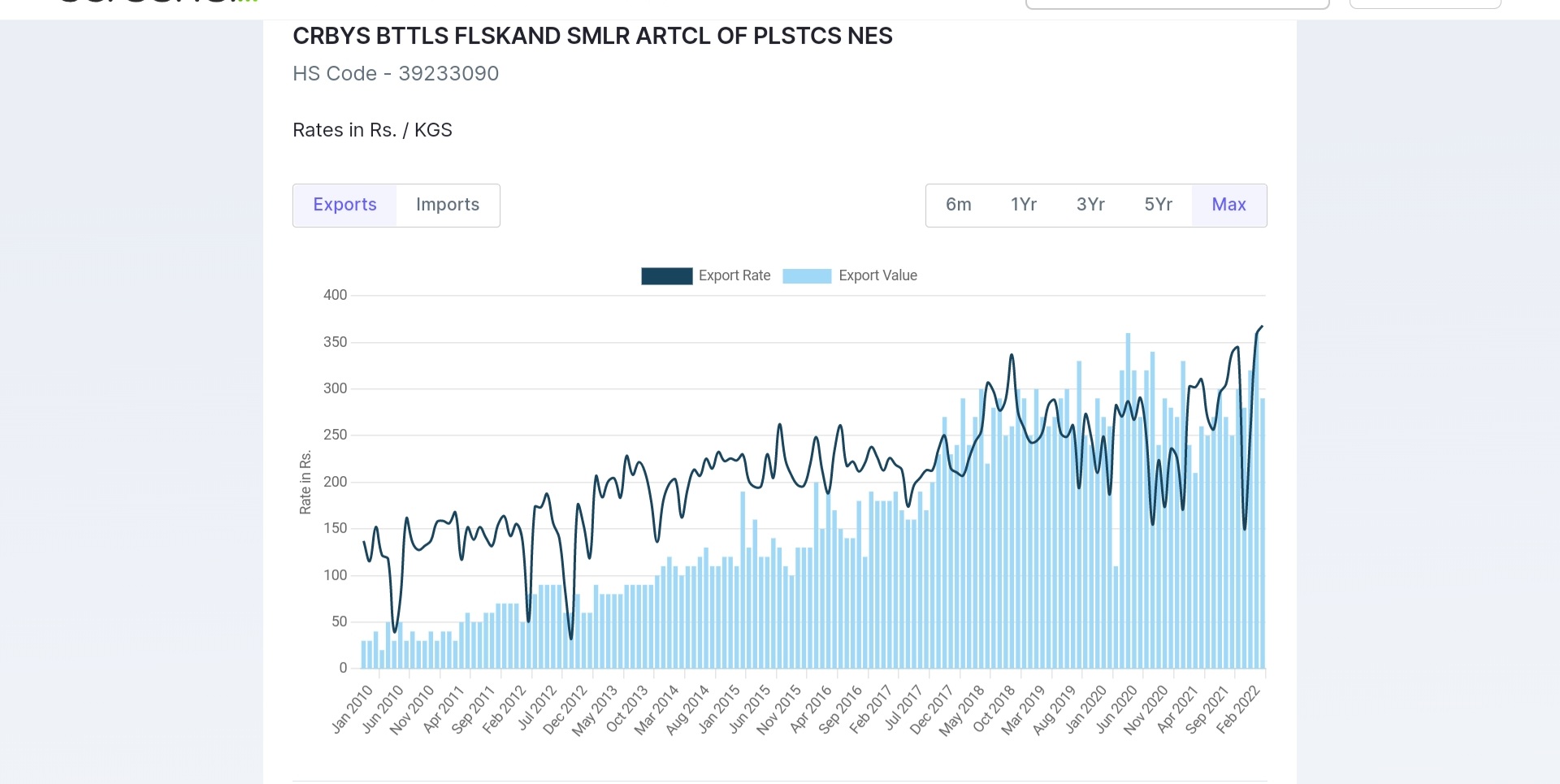

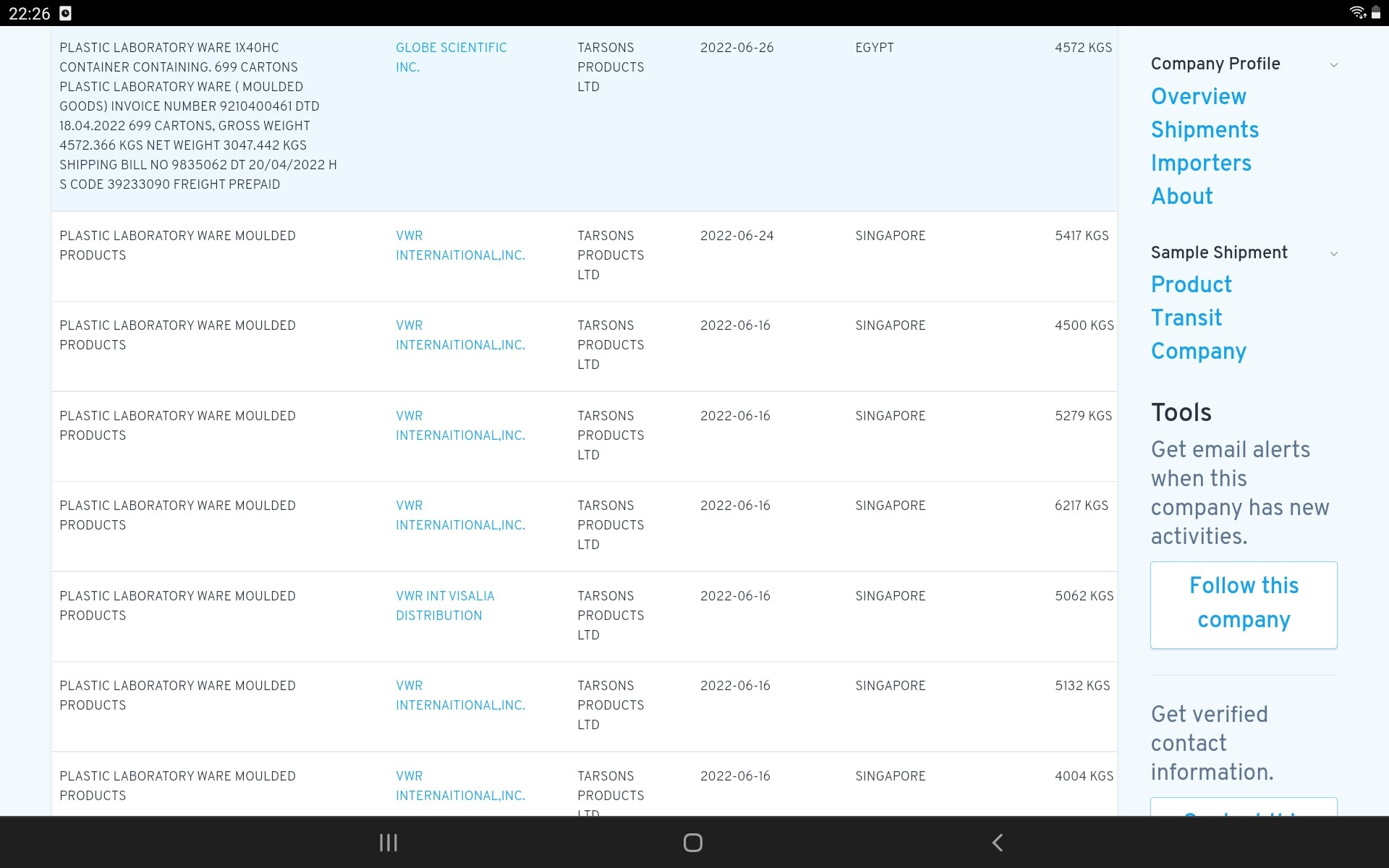

Lets see how both exports and Tarsons doing - industry exports and recent month deliveries from Tarson looks encouraging ( data may not be comprehensive but point is trend)

-

When industry itself is going to grow in high teens / early 20’s ( AR 22) , with some efforys, Tarson can continue its trajectory of 30%+ growth - as articulated in Mgmt commentary as well - retain or exceed past growth rate. We all know market likes high growth and award valuations accordingly, high margins and biz quality is bonus.

-

Part of capex is for sterilization capabilities in house, that adds few% margins and from customer angle one place to get it all.

-

On mfg location - two ways to look at it, pre IPO some of the mfg location were on lease, with new capex and new owned facilities its easier to extend where you are already part of eco system( approvals, people, moulds, upcoming sterilization etc). Given distributor led model, company focus is to ensure channel is well covered as demand is from key demamd regions and that doesn’t seem like a challenge esp logistics costs not affecting margins etc. As their export biz picks up( whitelabeled) - it would be easy to decouple at some point and look at near port type setup.

-

This is one of very few companies ouside auto sector/ capex plays which is closer to ATH even before mewningful mkt recovery, strength suggests good demand from participants, esp strong hands.

-

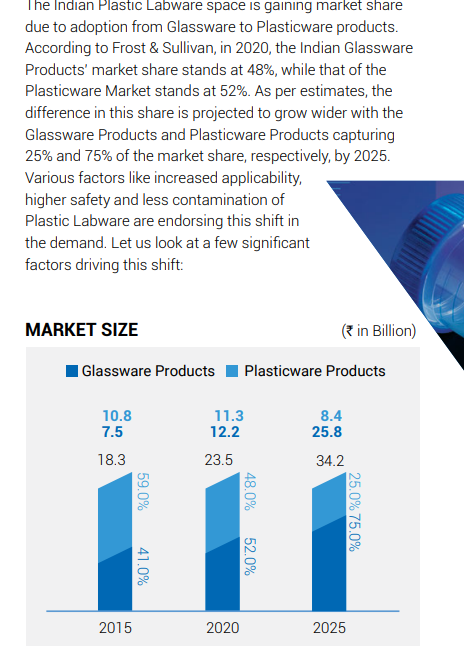

Not going into china+1, current energy crisis affecting competetion in EU/ US etc, glass to platicware transition but again tailwind helps.

-

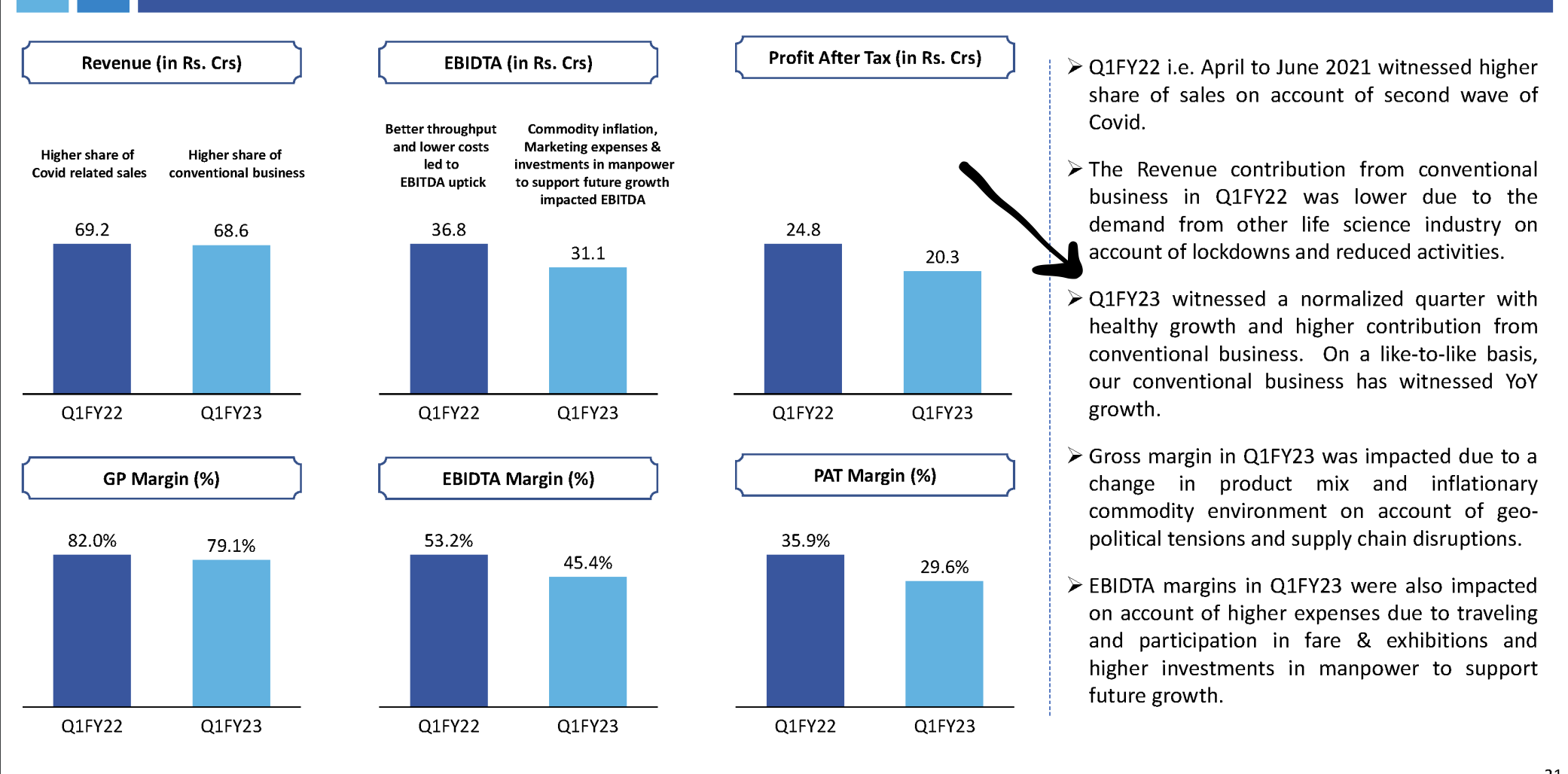

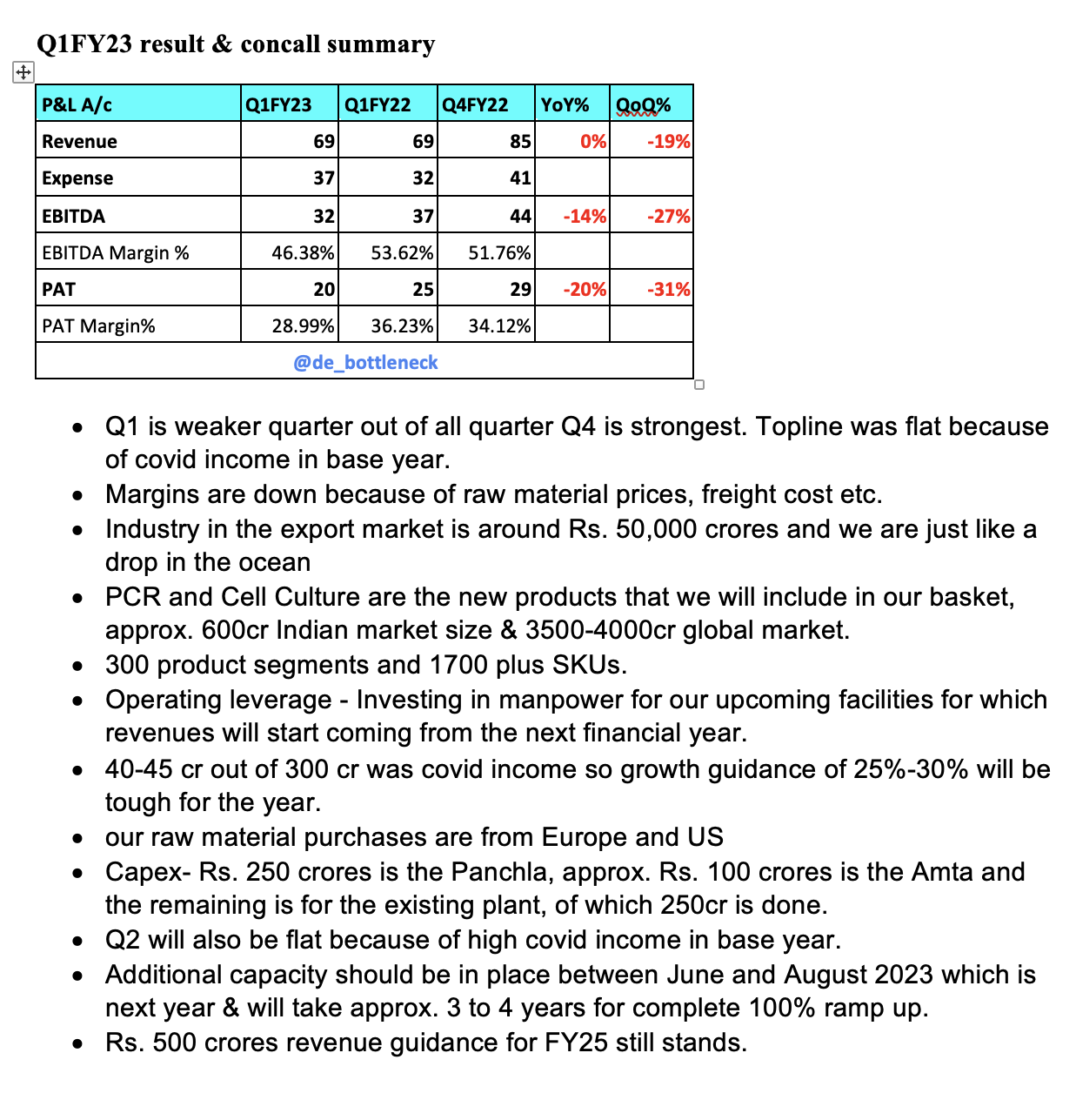

Though RM is linked to crude and generally company takes price hike once a year( if not mistaken Q1) - broadly they have maintained insanely high GM and increased EBDITA over last crazy year - one less key variable to worry about on supply side.

-

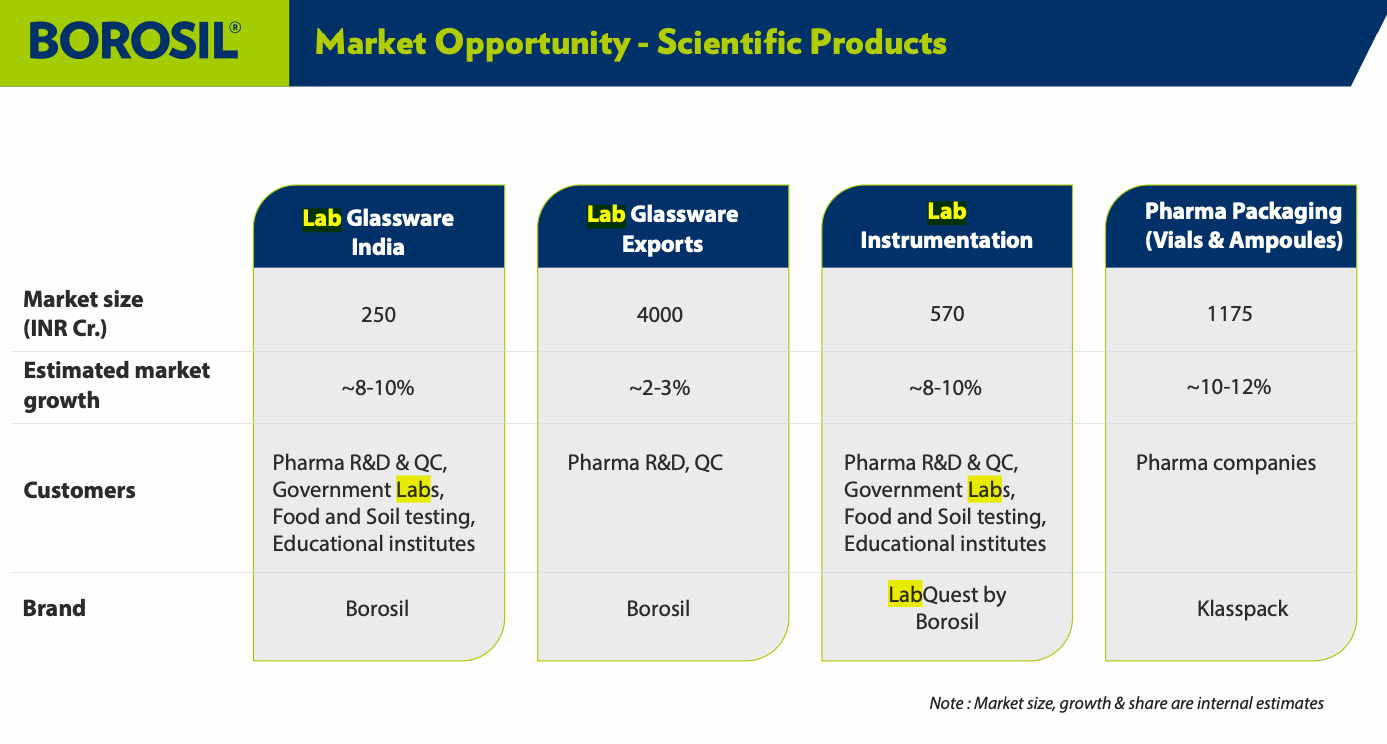

One can also look at Borosil capex & commentary on labware( though there focus is glass)- another validation of high demand from labware.

Invested