Yes Bhai. Deleting my post.

Have pasted it on IEX forum.

dr. vikas

Yes Bhai. Deleting my post.

Have pasted it on IEX forum.

dr. vikas

Sorry, I got carried away… Deleteting

Hero position I have completely moved to my parents portfolio, since it was low cost high dividend yield.

Auto strategy I am still figuring out. PV and CV sales are gaining traction while 2Ws are still muted compared to 2019.

Some of the auto anc stocks have shot up a lot and this could be just mean reversion but the shoot up has been too fast in some names.

I want to take my time understanding this sector before making any allocations.

I donot believe we will see the raging bull market we saw from second half of 2020 to Oct 2021. The next 12-18 months will be tepid, so a lot of time to research and accumulate stocks.

Hi Tariq sir. Been following you and learning from your threads for quite some time now. Would like to ask you when you have time can you tell me whats your investment framework? I know the steps you follow through the bloomberg video, but was interested in knowing whats your perfect stock?

Any Reasons for exiting ZEEL ?

Hello Tariq,

Thanks for sharing knowledge and PF.

Gone through podcast - Stock Talk With Tar 💰| wealth Podcasts - YouTube.

Like your thoughts on an index fund along with others.

Just want to know (or you can suggest your blog write-up or video etc).

Investment Framework is evolving. I do not like to stick myself to a particular philosophy within investing and over time learning a bit of everything (Technicals being the latest).

My goal is simple, to reach x amount in net worth. The delta between where I am today and where I need to be is fixed and I am slowly chipping away at the gap. I dont have any ambition to become the richest man in India or be among the greats of the investing world.

I, simply, am in the market to make money equivalent to my goal. Now whenever an opportunity arises to help make money I take it (whether its momentum, value, growth, technicals, break outs, shorting etc ), it doesnt matter to me.

Once I have achieved my goal of x net worth, all my investments will be passive and I will go about living my life.

The idea is always to have enough money to reach the stage in life where I can ‘buyback my own time’, i.e. dont have to work for a living.

Same as others, consolidating the portfolio.

Hi @Tar

In the SOIC Q4 results webinar, you mentioned that Aarti Industries is expensive, and you will be looking to buy it after the demerger, due to single-digit EBIDTA growth in the near future. May I ask what was the thesis to take the position already now?

Thanks for your articles and all your contribution to the investing community.

Hi! It was purely based on technicals.

678 is a strong support and demerger is ~2 months away so I took a call and invested.

Having said that, just a little below the 678 support is my stop loss, so if it does break down from 678, I will be out.

By investing now, I am just trying to reduce my average cost of Aarti Pharma. I do not expect price of Aarti Industries to correct much post demerger, so I should be able to sell Aarti Industries share at cost or even a profit (if market sentiment stays strong in second half of the year) and use the proceeds to further average down my cost in Aarti Pharma.

Thats the entire game plan.

Hi Tar, I see you have made a substantial position in Piramal-PEL. Now, i came across the valuation report of Pharma business as part of the demerger which values the Pharma business around 645 price. Anyone buying PEL is essentially paying ~ 70% to the financial service unit and only ~ 30% to Pharma unit. I wanted to know your thoughts on this- after demerger there are high chances that piramal finance will continue to go down and Piramal Pharma will continue to go up … ultimately leading to loss for anyone holding PEL before demerger.

Jumping in here with my 2 cents before @Tar as I have also recently taken a position in PEL because I feel the company in undervalued/fairly valued

@645/share, the demerged Pharma company will be valued at 15500Cr. Let’s look at the constituent businesses in the Pharma vertical

At 15500Cr, the Pharma business will be valued at 2.3x current sales. Do you think a business with such high quality as PPL’s deserves a 2.3x P/S multiple? In my view, even conservatively the CDMO, Complex generics and OTC businesses should be valued respectively at 6x P/S, 3x P/S and 5x P/S for a total conservative valuation of ~35000Cr. Considering Carlyle owns 20% of PPL, the market cap of PPL ex-Carlyle ownership would be ~28000 Cr.

That leaves about 13000Cr MCap for the finance vertical. The book value of that vertical is north of 20000Cr. So @13000Cr MCap, its valued at 0.65x P/B. Do you think its likely to go lower? Given the track record of Piramal as a business house, I am also quietly confident that they will turn around the Finance business, stabilize DHFL and actually be close to where they aim to be in 5 years in that business. However, I have taken a position mainly with the view to own the Pharma subsidiary.

Even if you consider holding company discounts while valuing PPL, I don’t think the overall business is overvalued at current prices. Its either fairly valued or undervalued (I am leaning towards the latter)

As always position size matters. Won’t increase position size beyond 5% before demerger.

Agree with @nirvana_laha, will just add the technicals here.

I dont think it will go down below 1630 and stay there, just based on price action of last several years.

So whenever it was below 1630, I was buying.

A good way to trade current markets is to buy fundamentally good companies at their long term support and place stop loss below that. If market sentiment sours further from here, you will be stop out of the position. If market sentiment is good, you stand to make good returns.

No one knows where the exact bottom is, so in my view this is a safe way to play the markets.

Look at it the other way, you are getting primal enterprises (pharma + finance business) for the same valuation you did in 2016. A lot has changed and improved in the business since 2016.

Hi Nitin, it’s mentioned in their latest investor presentation.

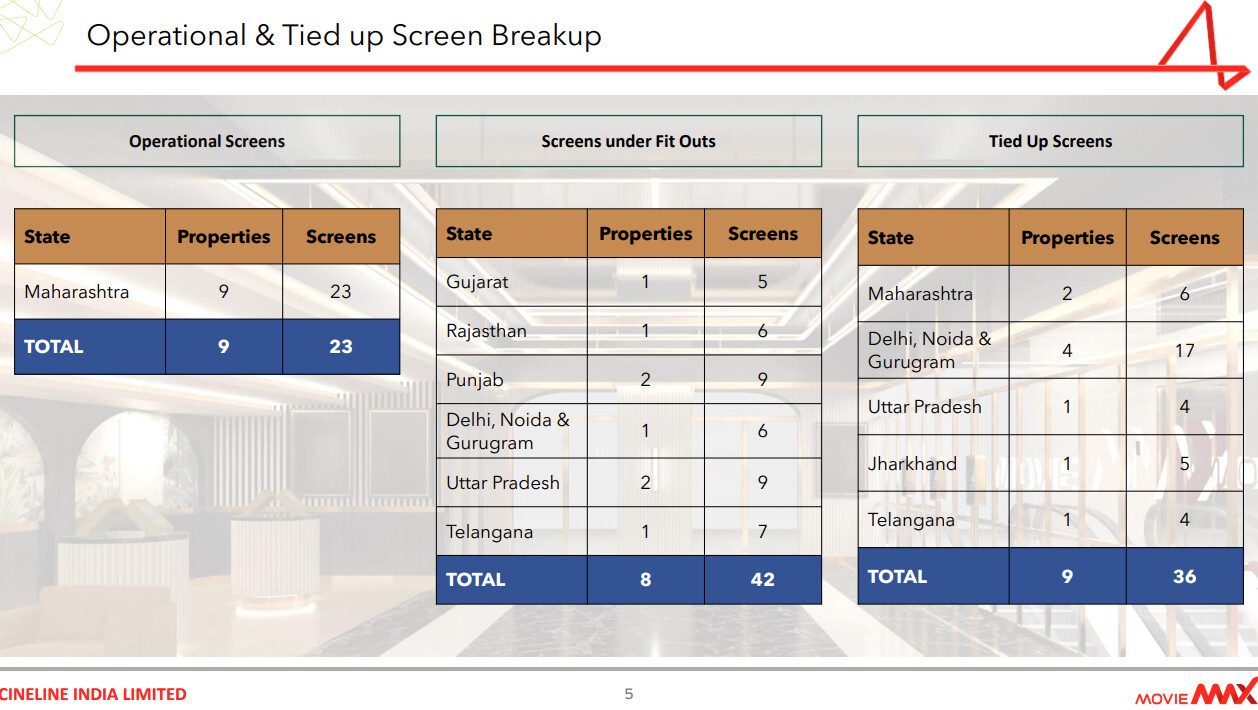

The non compete was valid till 31st Mar 2022. Company took over the leased screens back and had renovated 23 screens (9 properties) by April. So full quarters revenue of 23 screens should start flowing in from this quarter onwards.

By end of the year their plan is to make 101 screens functioning, so each quarter from here on there should be some bump up in revenues.

Edit: Adding Screenshot and Link to Investor Presentation, changed screen number from 26 to 23

Hi Tariq sir. I remember reading that you’re willing to do a 10-year experiment with IEX. Was curious to know your reasoning behind this experiment and what you feel will be the outcome?

Hi ,

I recall that regarding another special situation(MSUMI maybe) , you had written that after listing of the new entity it goes down for a few days because the funds sell the newly listed smaller entity from their “Largecap\midcap” or “Bluechip” funds to meet the guidelines. This causes a few days of selling pressure and the lowest possible entry point .Infact, it did actually happen that way for Motherson sumi demerger .

Any reason why this will not be the case for PEL pharma stock ?

Shareholding pattern and type of demerger. Every special situation is different.

In MUSMI, a smaller business was getting demerged. Those institutional investors didnt buy Motherson cause of its domestic wire harness business.

In case of Piramal, its a demerger of equals if not of the better business. Most institutions have bough PEL for the pharma business, not the financial one.

Very few companies that can keep growing at 20%+ for a decade. I also entered in IEX at its lowest price. So seems like a perfect candidate for an experiment.

I will let you know in March of 2030.

Also Tariq sir, just caught up with all 208 posts. I saw you were very bullish on RACL. In one instance you said you would hold it for 10 years. How come you sold it? What changed/ What went against your investment thesis?

Tariq sir, I know you start with studying the industry first and then go into the companies. You like mega-trends with alot of tailwinds. How come you don’t want exposure to EV theme or QSR? Its so talked about everywhere (a main reason one should def not buy into) but just trying to understand your thoughts on it,