Sixth out yesterday. Among other things, it primarily focuses on Tanla-Microsoft partnership. Details Wisely and, importantly, shows how this partnership is a win-win for both Microsoft and Tanla. Microsoft sub stack AZURE hosts the Tanla Platform and that in is to raise AZURE usage to new highs. The entire series makes a very interesting read for anyone learning CPaaS and Tanla. Invested. CPaaS, Twilio, Blockchain and Tanla - Part 6 - Breezy Briefings (substack.com)

4 Likes

Now the latest is, today Azim Premji had invested in Tanla Platforms worth 250 cr. That’s massive investment.

4 Likes

I am sure his team has done due-deligence. I am still not sure what they saw to invest at this price, but I hope it is not some marketing ploy by the parties involved (aka sell the news).

Still holding onto about 50% of what I had, since my entry is very low.

1 Like

Latest good article to read.

“Tanla case study - combining value, momentum and insider buying” by Abraham George. https://breezy.substack.com/p/waga-waga

4 Likes

Continuing the trend, Tanla logs in very strong Q3 results with strong growth on both y-o-y and q-o-q basis

TANLA. Q3 :

CONS. NET PROFIT UP 69 % AT 158 CR (YOY), UP 16 % (QOQ)

REVENUE UP 35 % AT 885 CR (YOY), UP 5.1 % (QOQ)

EBITDA UP 60 % AT 202.7 CR (YOY), UP 13.4 % (QOQ)

MARGINS AT 22.9 % V 19.4 % (YOY), 21.2 % (QOQ)

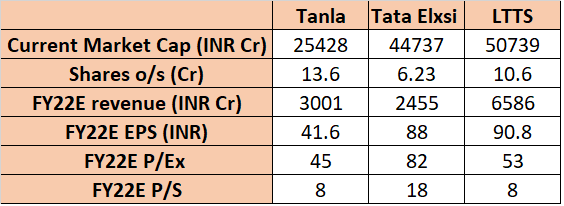

Tanla’s 9M EPS is 29.4/share, expect it to close the year with 41-42 EPS. At CMP of 1875, that will give it a PE of 45-46x . Comparison between valuations of Tanla, Tata Elxsi and LTTS are below (Q4 rev and EPS assumed to be 5% higher than Q3 nos. for all 3 companies):

Q3 Investor presentation - Good disclosures and new focus on ESG

Tanla Q3FY22 Investor Presentation.pdf (2.6 MB)

Tanla Q3FY22 Press Release.pdf (302.9 KB)

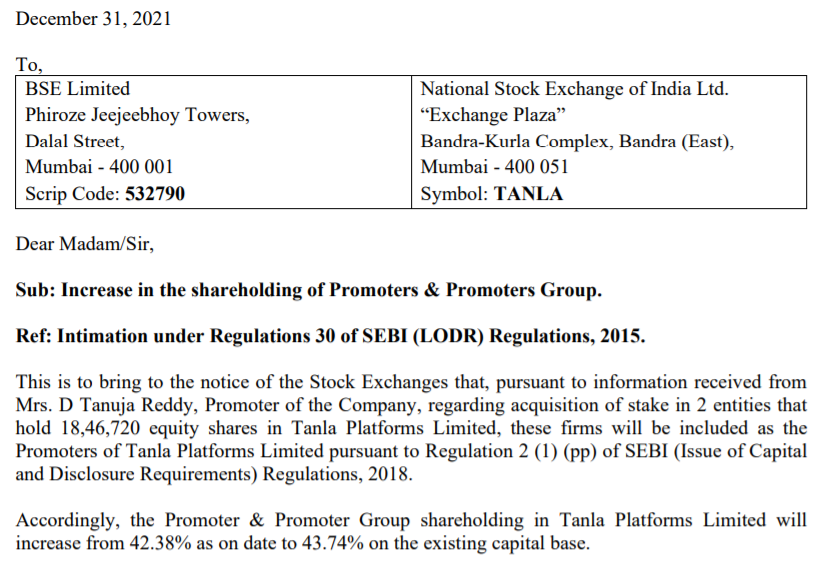

Q3 shareholding pattern - Shareholding Pattern

Promoter and promoter group controlled stake increased by 1.36% to 43.74% during the quarter. As highlighted before in this thread, during the Qtr Premji Invest picked up ~1.5% stake in the company.

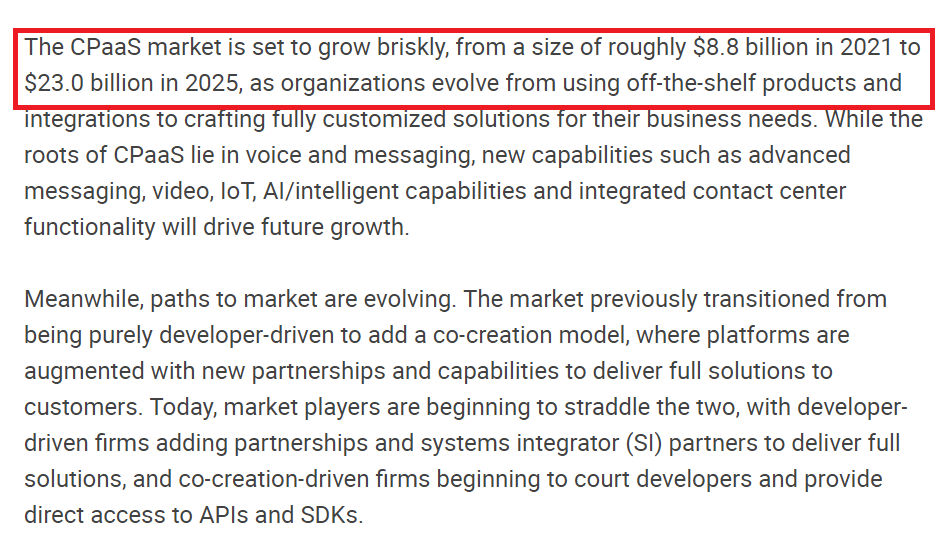

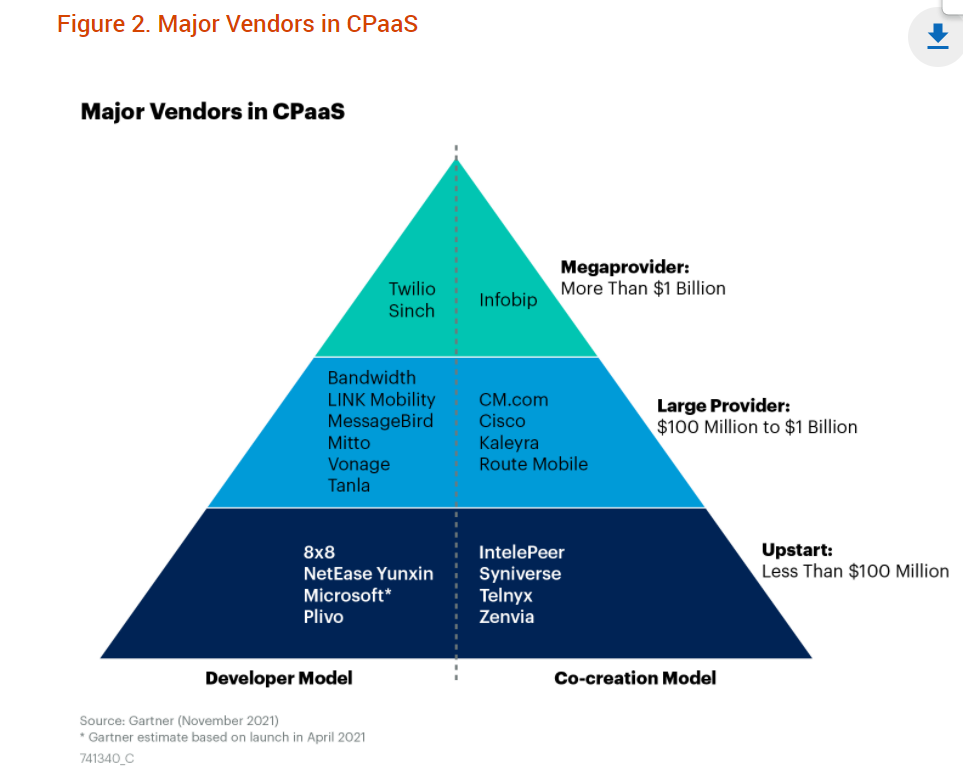

Tanla was prominently featured in this Nov 2021 Gartner report as one of the largest CPaaS players in the world along with the likes of Twilio and Sinch -

Gartners CPaaS report Nov21.pdf (387.8 KB)

A few key snapshots from the Gartner report

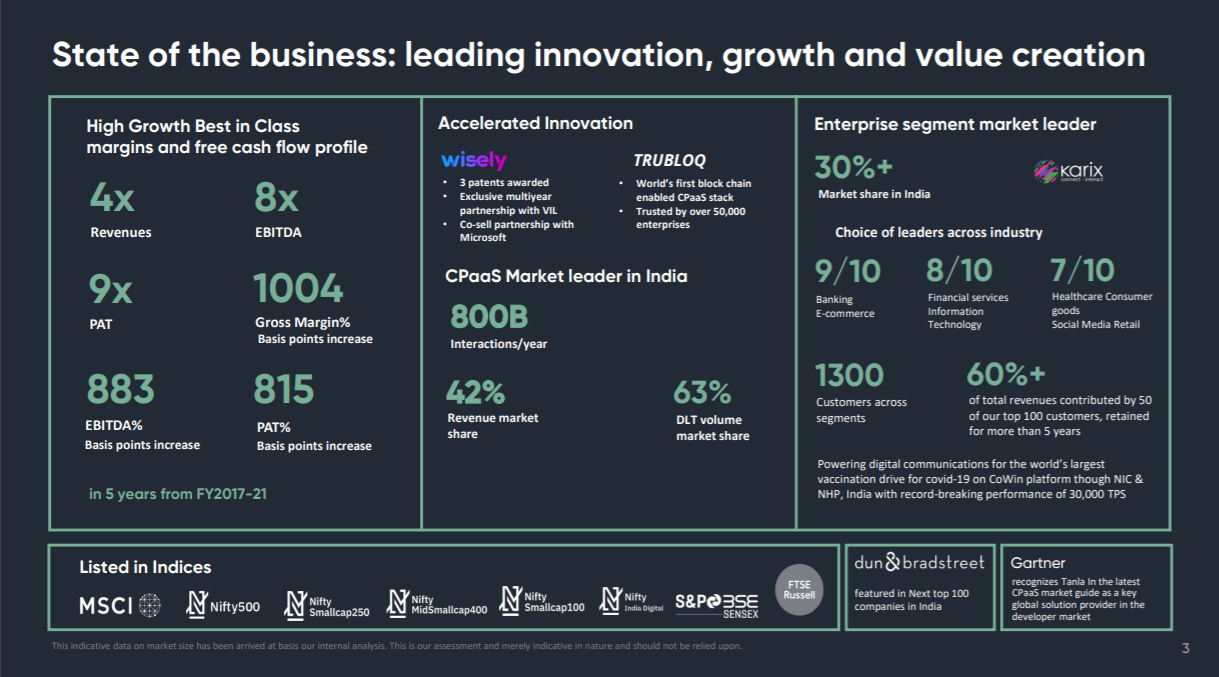

Global CPaaS market is slated to grow at a CAGR of 27% between FY21-25 and Indian market is expected to grow much faster given low adoption base. Tanla is the undisputed CPaaS market leader in India with > 40% revenue share of the market. Tanla processes about 60% of the A2P SMS traffic in India. Its recent platform launches of Trubloq (FY 21) and Wisely (FY 22) take it to the next level in CPaaS landscape alongside the likes of Twilio.

Trubloq - Tanla's DLT platform Trubloq built to enforce TRAI regulation | Business Standard News

Few key metrics for Tanla

Disclosure: Invested and biased.

9 Likes

Tanla has indeed posted outstanding Q3 results across all the metrics. Also I see this time, the company has put more detailing on ESG front too.

Discl: Invested at lower levels

1 Like

Q3 Management concall summary:

-

Wisely beta launch for Vodafone Idea in Feb, commercial launch from March 1st (One month Wisely revenue contribution in this FY)

-

Wisely global launch planning complete with leading management consulting firm. Roll out will be done post May. Strategy is to release a case study of VIL performance improvements via Wisely from March-May and use the case study to leverage global launch

-

Q3 gross margins @ 29.5% and 9M FY22 gross margins @ 28.2%. Management hopeful of taking up gross margin to 50% levels at par with global CPaaS players like Twilio as platform revenues scale via Wisely and Trubloq. Platform business has 90% gross margin and contributed 23% of Q3 gross margin even though topline contribution of platform business was only 7.5%.

-

Management continues guidance for growth as per Rule of 40 i.e. sum of Y-o-Y revenue growth % and EBITDA % for quarter = 40. Number for present quarter was 58 (YOY topline growth 35% + EBITDA margin 23%)

-

2nd key Wisely partnership after VIL is in beta stage right now and is expected to be announced in February 2022

-

Trubloq continues to have 63% market share in DLT (Distributed Ledger Technology for telemarketer registration as mandated by TRAI - TRUBLOQ | EMPOWERING CHOICES) business in India (Voda-Idea, BSNL and Airtel partially. Other competitors are IBM (Airtel part business) and TechM(Jio)). Trubloq deployment in UAE is complete. Trubloq revenues to keep growing as new features get released on the platform such as consent management.

-

Company has 846 Cr cash in books. It is not looking to do any large acquisition as its plans to grow in International markets largely by scaling Wisely (Big bet by management on its Wisely platform and is contra to major M&A action and consolidation happening in global CPaaS markets currently). It seemed from management commentary that one more round of share buyback highly likely in Q1/Q2 of FY23.

-

Investments to be deployed in 4 areas - platform and products, customer success, brand and hiring talent for global scale up.

Current valuations - After today’s drop, TTM PE is 48x and FY22E PE is 43.5x. One of the cheaper high growth software (product/platform) companies in India right now. Indian CPaaS peer trading at 68x TTM PE.

Disclaimer - Invested and biased.

13 Likes

Couple of points/queries:-

- While Tanla may adopt the rule of 40 (applicable for Saas players) its business model does not seem to be truly Saas. While their enterprise segment is transaction based, their platforms segment is based on revenue sharing. Also, their current tie-ups with UAE telecom comprises of on premise solutions(license based).

- Any idea on the pricing strategy for channels other than SMS e.g. whatsapp and the percentage revenue share on the platforms segment?

As far as I have understood, all their future enterprise revenue will be routed through their Wisely platform. They have already migrated some of their key domestic clients (HDFC, Kotak) to Wisely in India. The tie-ups with the UAE telecom companies are for for a DLT implementation using Trubloq and are indeed on a license basis and are not going to materially contribute to revenue and bottomline as mentioned by Uday in yesterday’s call. However they will be cited as proof of international adoption of Tanla’s self developed tech platforms while pitching to International clients.

The deal with Vodafone Idea for Wisely appears to be a 1000Cr per annum deal. While Vodafone was already their customer, Idea wasn’t and thus this deal alone should contribute about 450-500Cr incremental topline to Tanla from FY23 onwards. No idea on pricing for SMS vs other modes, only thing I know is Whatsapp and similar channel margins are higher than SMS.

I am new to the CPaaS space and still learning. If you have details or insights about Twilio or Sinch’s pricing or business model in contrast to Tanla, please do share!

1 Like

Any Paas/Saas/Iaas is a volume game. Higher the volume, higher is the contribution to the top line and bottom line of the service provider and at the same time higher discounts to the customer. Some details around pricing are available on Twilio’s website while Sinch has not disclosed upfront but it should be around similar lines.

While Tanla’s overall strategy of establishing itself in the Indian market and gradually aiming the global market makes perfect technical and economic sense, the successful execution of its strategy is a key factor here. At some point in time, in the future, Tanla’s ultimate aim seems to be having the entire market (globally) on Wisely. At the end of the day, this is what even Microsoft would aim - to get volume on its platform (wisely is hosted on azure for which Microsoft charges hosting/cloud charges to tanla). However, what is wisely’s pricing as a CPaas offering and who controls it is a key question here given the revenue sharing model. Probably, a question to the management in the next concall.

7 Likes

Is Tanla too much dependent on VI for Wisely and other product revenues? Is market not considering the potential impact of VI going down on it’s impact on Tanla or is it already factoring that explainingthe reasonable valuations? (VI: Vodafone India)

I have realized that Tanla is not yet a “darling” of the Indian stock market in spite of stellar growth in topline, bottomline and great platform/product deliveries over the last 3 years. Maybe its because there were some Corporate Governance slip-ups in the past or maybe because its competitor in Indian markets - Route Mobile - made a big splash with their IPO in late 2020 (They claimed they did not have a CPaaS peer in Indian markets, something that many business publications and DIIs think till this date). Tanla went under the radar and its transformation to a CPaaS solutions platform went relatively unnoticed. That reflects in its valuations compared to other fast growing tech stocks.

Valuations will level up if a few more quarters of stellar growth continues. VI is Wisely’s first newly acquired customer (Voda was with Tanla, but Idea wasn’t). Tanla has already migrated its existing Indian clients to Wisely - HDFC Bank, Kotak Mahindra bank etc. Tanla will announce its second major client win for Wisely in February for whom beta testing is going on right now. These are big deals. The VI deal is likely to bring Tanla 500 Cr of new revenue annually, hopefully the Feb deal will also be large. VI’s performance on Wisely will be used as a launchpad by Tanla for launching Wisely in International markets. This will be a critical development as its success can unlock a completely new phase of growth for the company. Almost all of Tanla’s present revenues come from India.

Tanla’s numbers speak for themselves - 5 year sales CAGR of 40%+, PAT CAGR of 100%+ and current year 9M ROCE of 70%. 800 Cr cash balance, huge free cash flow generation every quarter and indications of another buyback by Management. Don’t know when market will re-rate the stock but right now its trading at ~40x FY22E EPS. Its for every investor to study and decide for himself/herself whether that’s a fair valuation or not for Tanla.

13 Likes

An interesting read " Tanla is in a league of its own" , which was released a few couple hours ago (in a series of articles by Abraham George)

Discl: Invested at lower levels.

6 Likes

Hi,

Thanks for the concall extracts.

Fairly comprehensive, i would say.

1 Ques: Which is the other Indian CPaaS peer you are comparing it to?

there r only 2 listed players…

Tanla and Route mobile

2 Likes

Thanks. But isn’t this just a miniscule addition to his existing large position?

2nd partnership for Wisely revealed today and its truly global. Partnership with Truecaller.

Will await more data about the partnership to assess revenue impact. But in terms of global credibility, partnership with Truecaller is big.

6 Likes