Where’s Tanla heading ![]() Already rushing to 5 years’ low

Already rushing to 5 years’ low

1 Like

Is this the actual revenue earned by the company?

Their revenue recognition is inclusive of charges to be paid to Teleco, OTT, which includes their pass-through.

If you exclude that, their gross margins are roughly 20% (adjusting for the purchasing of messaging services). Hence, their revenue recognition is not actual revenue.

Correct me if I am wrong!

Indian CPaas market size is much more than 1bn USD. Tanla claims to have 30% market share with nearly 4K crore revenues. I would put the Indian market at roughly 1.5-1.8bn+ USD. There is lot of double counting in this market as same revenue can be counted thrice in some cases - example - small aggregators taking sms from Tanla in bulk. In this case three parties get included - Telco, Tanla and the small aggregators. In any case two parties are generally always there - Tanla/Route/others as aggregator and Telco/Whatsapp - the provider. The revenue counting is correct as Tanla/Karix bills to enterprises and therefore thier billing is thier revenue (just like a trader). They pay to Telco/Whatsapp nearly 80 paise of whatever they earn (on average) on the enterprise business, giving a gross margin in range of ~20% as an example.

Even manufacturing companies buy Raw material, do value add and sell, making gross margins of 20-40%. Their sales is their revenue.

The CPaas player also do a lot of value add - but not directly on the product (sms) , but on the way that product is consumed (solutions for OTP, marketing campaigns, platform for sms delivery within Pre defined SLA’s and tracking in huge volumes etc.). Think of Revenues of Dmart for example - they don’t value add on product manufactured by HLL for example , but the value add is in getting that product to consumers and associated supply chain and retail experience.

2 Likes

Tanla Q4 - a mixed bag.

Enterprise business growth taking momentum.

- Revenue increase means either or both of 1. Price stability 2. Market share loss reversed.

- Gross margins stability and increase over last 2 quarters.

- If it can continue the momentum for another couple of quarters, we can say enterprise business has turned around. Tanla seems to have got it’s act together on this finally.

Platform business - absolutely nothing to write home about. That’s the sad part. Tanla story in last few years hasn’t been about enterprise business. It has been about platforms. Few hundred crores have been spent on platform development. Yet other than DLT, rest don’t even likely return the salary cost of maintaining those. Tanla has so far been a miraculous failure on that. They create a product, take it to one or two customers and simply can’t scale it beyond that. Literally no geographic expansion at all.

I sometimes wonder if they are creating a point solution for a customer and calling it a platform without a proper market assessment of demand. Or they simply don’t know how to market ? Either way this endeavour is a failure kept alive from DLT revenues and maybe promoter’s ego.

I would love to change my views and see Tanla do well. I genuinely believe in the power of product and platforms. But Tanla so far, as I write this, between 2021 to 2026 has been a total failure in platform business if we exclude DLT. 5 years is a hell lot of time.

Also, Uday Reddy needs to utilise the cash flow better and acquire and grow, since they can’t create anything sales worthy on their own. He has to let go of this mentality that he can create better and genuinely explore adding capability and customers thru acquisition.

4 Likes

Hi @anna ,

Your analysis is quite on point. The enterprise segment recovery does look real. However, the platform business is clearly struggling to scale. I had expected ATP to see wider adoption across banks, so seeing only 3 banks in 4 years is a bit disappointing.

Uday did mention in the concall that a new platform will be launched next quarter, but how much one can rely on that remains to be seen. That said, to be fair, these products often take time to prove themselves in the real world. Once credibility is established, adoption can pick up, especially for something like ATP.

One positive is that the business continues to generate strong cash flows, which does provide some comfort from an investor’s perspective

1 Like

Yes, enterprise sales cycles are long. Telco could be glacial.

I believe platform growth could also start coming this year. Firstly, time has elapsed and from whatever funnel they have, something should start dropping. Secondly, the new platform is likely to have one or two anchor customers. Thirdly, Indonesia RCS platforms should start delivering some revenues in another 2-3 quarters as ecosystem steps up. Fourthly, even India RCS should start scaling up a bit.

All in all, I am optimistically positive about improving growth and solidity (green shoots, not some bumper Dhamaka).

Nonetheless, my criticism on Not doing acquisitions( for example, to improve reach into Telco market) and the lack in platform revenue growth remains. Long sales cycle , willingness to pay etc is not a new discovery. This was a known fact.

1 Like

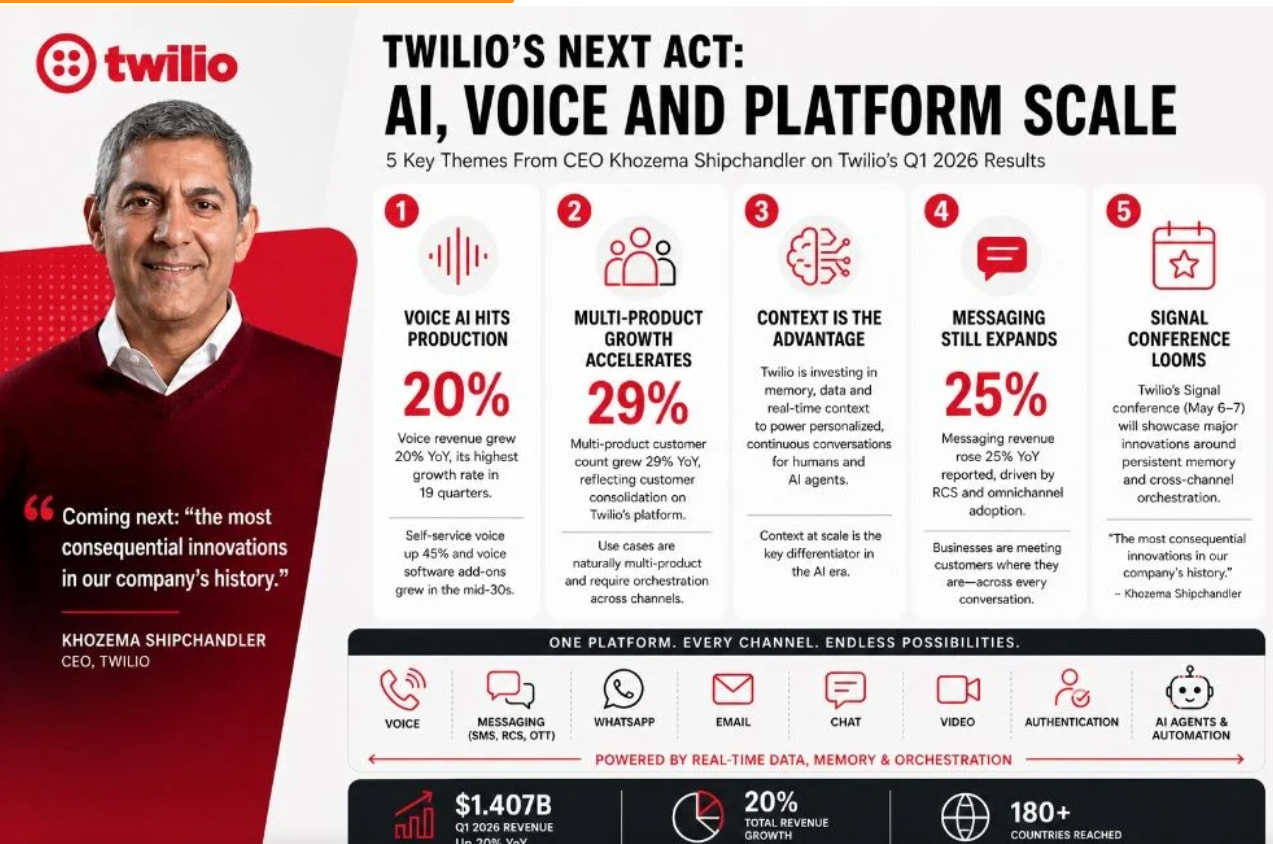

Twilio reported its earnings a few days ago, and what stood out to me was the strong emphasis on Voice AI. Here’s a snapshot:

1 Like

Voice is the next big thing in CPaaS. I think you can start hearing from Indian CPaaS players soon on voice. Have no idea of size, growth etc. But it is looming.

1 Like

how so? could you please elaborate if possible?

Can you explain the context of voice ai

Twilio’s AI/RCS Pivot — and What It Means for Tanla

Twilio is the best case study for what a CPaaS-to-AI-platform transformation looks like in real time. They’re the one company that’s actually pulling it off, and just last week (April 30, 2026) they reported numbers that confirmed it.

The numbers — Twilio is suddenly growing again

After years of being a “broken growth story,” Twilio just had its best quarter in 3+ years:

-

Q1 FY26 revenue: $1.41 billion — up 20% YoY, with non-GAAP gross margin of 50% Futurum Group

-

Voice channel grew 20% — highest growth rate in 19 quarters (almost 5 years) Yahoo Finance

-

Messaging grew 25% YoY, supported by WhatsApp and RCS Yahoo Finance

-

$132M free cash flow in Q1, $279M non-GAAP income from operations, $253M share buybacks Yahoo Finance

-

Stock up 53% over the past year, trading near 52-week high of ~$154 Investing.com

-

Market cap: ~$21.5 billion

Compare this to where Twilio was 2 years ago — declining revenue, mass layoffs, an activist investor (Anson Funds) pushing for breakup. The stock had crashed ~85% from its 2021 peak. Today the narrative has completely flipped.

What changed — three things

1. Voice AI became a real product, not a buzzword

This is the single biggest shift. Voice revenue grew 20% YoY, “the highest growth rate in that product in 19 quarters” — driven by AI use cases and accelerating adoption of software add-ons including Conversational Intelligence and Branded Calling, both of which grew more than 100% year over year. CMSWire

The mechanics: When you call Domino’s and an AI takes your order — that AI is increasingly running on Twilio infrastructure. When a healthcare scheduling AI calls patients to confirm appointments — that’s Twilio. Scorpion built an AI agent on Twilio’s ConversationRelay that boosted booking rates by 39%, captured 6,500 appointments, and generated $8.4 million in revenue in three months. CMSWire

This is fundamentally different from selling SMS at fractions of a cent. AI voice agents bill per minute and per outcome, not per message.

2. RCS is finally happening (but slowly)

RCS volume more than doubled quarter-over-quarter, though leadership also said RCS remains too small to materially move overall messaging results yet. Futurum Group

The big wins: Notable RCS deals with KPN Netherlands to power RCS across all major mobile operators, and with TeleVox to enable RCS for organizations in regulated industries. AOL

The honest version: RCS is doubling QoQ off a tiny base. It’s a future driver, not a present one. Same as for Tanla.

3. The platform pitch — “infrastructure for AI agents”

This is the strategic positioning shift. Twilio is no longer pitching itself as “we send SMS.” They’re pitching: “we are the substrate that AI agents need to talk to humans.”

CEO Khozema Shipchandler at SIGNAL: “introducing new capabilities that orchestrate context-rich conversations with persistent memory across every channel for humans and AI agents… Twilio is becoming the foundation for how businesses engage their customers in the age of AI.” AOL

The technical pivot they made: they completed a significant back-end re-architecture for Segment to enhance context and memory across all communication channels, repositioning data as central to the platform strategy. Translation — they’ve integrated their CDP (customer data platform, Segment, which they bought for $3.2B in 2020) directly into messaging/voice so AI agents have memory across conversations. AOL

The AI-native customer wins are real: AI-native companies including Sierra and Bland.AI deepened their Twilio relationships in Q1, with Sierra signing a cross-sell deal for global expansion and Bland.AI committing to a multi-year deal. CMSWire

The competitive threat Twilio is racing against

This is the part most analyses miss. Twilio’s voice AI play is happening while voice AI specialists are scaling massively:

ElevenLabs has scaled to $330 million in annual recurring revenue and an $11 billion valuation, with their ElevenAgents platform targeting customer support, sales automation, and internal enablement — the same enterprise voice AI workflows Twilio is now building into. Sierra (founded by ex-OpenAI/Salesforce executive Bret Taylor) has reached unicorn status. Anthropic and OpenAI both offer voice agent capabilities through their model APIs that any enterprise developer can build on directly. TNW | Finance

So Twilio’s bet is: “We own the telephony infrastructure layer that all these AI agents need to actually reach humans through phone numbers, SMS shortcodes, and carrier relationships.” The model companies build the brains; Twilio carries the voice.

Twilio’s framework: CPaaS 1.0 → 2.0 → 3.0

Twilio (and Infobip) explicitly frame this transition:

-

CPaaS 1.0 = SMS, voice (the pipe business — commodity)

-

CPaaS 2.0 = WhatsApp, RCS, email (richer channels — better margins)

-

CPaaS 3.0 = AI-orchestrated conversations with persistent memory across channels (software economics)

The thesis: Whoever owns 3.0 gets SaaS multiples (10x revenue+). Whoever stays in 1.0 gets utility multiples (1-2x revenue).

Now — what does this mean for Tanla?

This is the important translation. Here’s the side-by-side:

| Twilio | Tanla | |

|---|---|---|

| Q1 FY26 Revenue | $1.41B (~₹11,750 cr) | ~₹1,178 cr |

| Revenue Growth | 20% | 15% |

| Gross Margin | 50% | 27% |

| Voice AI Strategy | Real product, growing 20% | Limited; mostly Truecaller verified calls |

| RCS | Doubling QoQ, 40+ telco deals globally | India market leader (~40% share), Indonesia rollout |

| AI Platform Story | ConversationRelay, Segment integration, AI agent infra | Wisely AI (anti-spam) + Trubloq AI |

| Market Cap | $21.5B (~₹1,80,000 cr) | ~₹6,800 cr |

| P/S Ratio | 4.27x | 1.5x |

Three takeaways:

1. Twilio’s recovery validates the bull case for the entire CPaaS sector

If Twilio can grow 20% and re-rate from $30 to $150 (5x in 2 years) on the AI-native pivot, it means the market does eventually reward CPaaS players who successfully transition. The CPaaS-is-dead narrative was wrong — or at least, “CPaaS 1.0 is dead, 3.0 is a SaaS opportunity.”

2. But Tanla’s playbook looks weaker

Twilio’s AI play is horizontal — an infrastructure layer for any AI agent that wants to reach a human (Sierra, Bland.AI, ElevenLabs build on Twilio).

Tanla’s AI play is vertical-specific — Wisely AI is anti-spam/anti-scam for telcos. It’s a great product (the Indosat case is real — 100M users protected, 10% ARPU growth), but it’s a single use case sold to a small number of telcos. It doesn’t have the network-effects flywheel of “every AI startup builds on Tanla.”

Tanla doesn’t have a Segment-equivalent CDP. It doesn’t have a developer ecosystem like Twilio’s. It doesn’t have voice AI infrastructure that competes with Bland.AI. Its moat is in the Indian regulatory pipe (Trubloq, telco DLT), which is valuable but geographically capped.

3. The valuation gap reflects this

Twilio at 4.27x P/S vs Tanla at 1.5x P/S. Even after Twilio’s AI re-rating, the gap to Tanla isn’t because Twilio is overvalued — it’s because Twilio’s AI thesis is more credible to investors.

For Tanla to re-rate similarly, Wisely AI needs to expand from 1 marquee customer (Indosat) into 5-10 telcos across SE Asia, Middle East, and Africa — and ideally turn into a platform that ISVs build on, not just a product Tanla ships. Management has set a 20% EBITDA CAGR aspiration. That’s the bar.

The honest summary

Twilio is the proof that the AI/RCS pivot can work. They had a worse starting position than Tanla 2 years ago (declining revenue, activist pressure, mass layoffs) and have come out the other side with 20% growth and a 5x stock recovery.

Tanla is following the same playbook, just smaller and earlier. They have the right ingredients — AI products (Wisely), RCS leadership in India, telco relationships in SE Asia, debt-free balance sheet — but they haven’t yet shown the inflection that Twilio just did. The Q4 FY26 results (15% revenue growth, 14.5% PAT growth) are a step in the right direction, but it’s not yet the “this company is fundamentally different now” moment that Twilio had this quarter.

If you want a leading indicator for Tanla’s re-rating, watch:

-

Wisely AI new telco wins (target: 2-3 announcements per year)

-

Platform segment growth rate (currently slowing from earlier 50%+ to ~9.8%)

-

Whether Tanla announces an AI-native developer platform comparable to Twilio’s ConversationRelay

-

Any partnership with a foundation model company (OpenAI, Anthropic, Google) for Indian-language voice AI

The bull thesis for Tanla isn’t broken — it’s just unproven. Twilio just proved the broader thesis is real.

Some cotext on twilios voice agents