Current Market Cap = ₹ 9,000 Cr

Overview :

TMB Ltd is one of the oldest regional private sector banks. It was founded in 1921 and was named as ‘Nadar Bank’ . The name of the bank itself suggests that it is a community based bank. Nadars are an entrepreneurial south Indian caste ( predominant in the districts of Kanyakumari, Thoothukudi, Tirunelveli and Virudhunagar ).Later in 1962, the name was changed to Tamilnad Mercantile Bank Ltd. The bank is headquartered at Thoothukudi, Tamil Nadu. It came up with an IPO in Sept 2022 and was subscribed 2.86 times.

Financial Performance : (From FY23 Annual Report)

At the end of FY 2022- 2023,

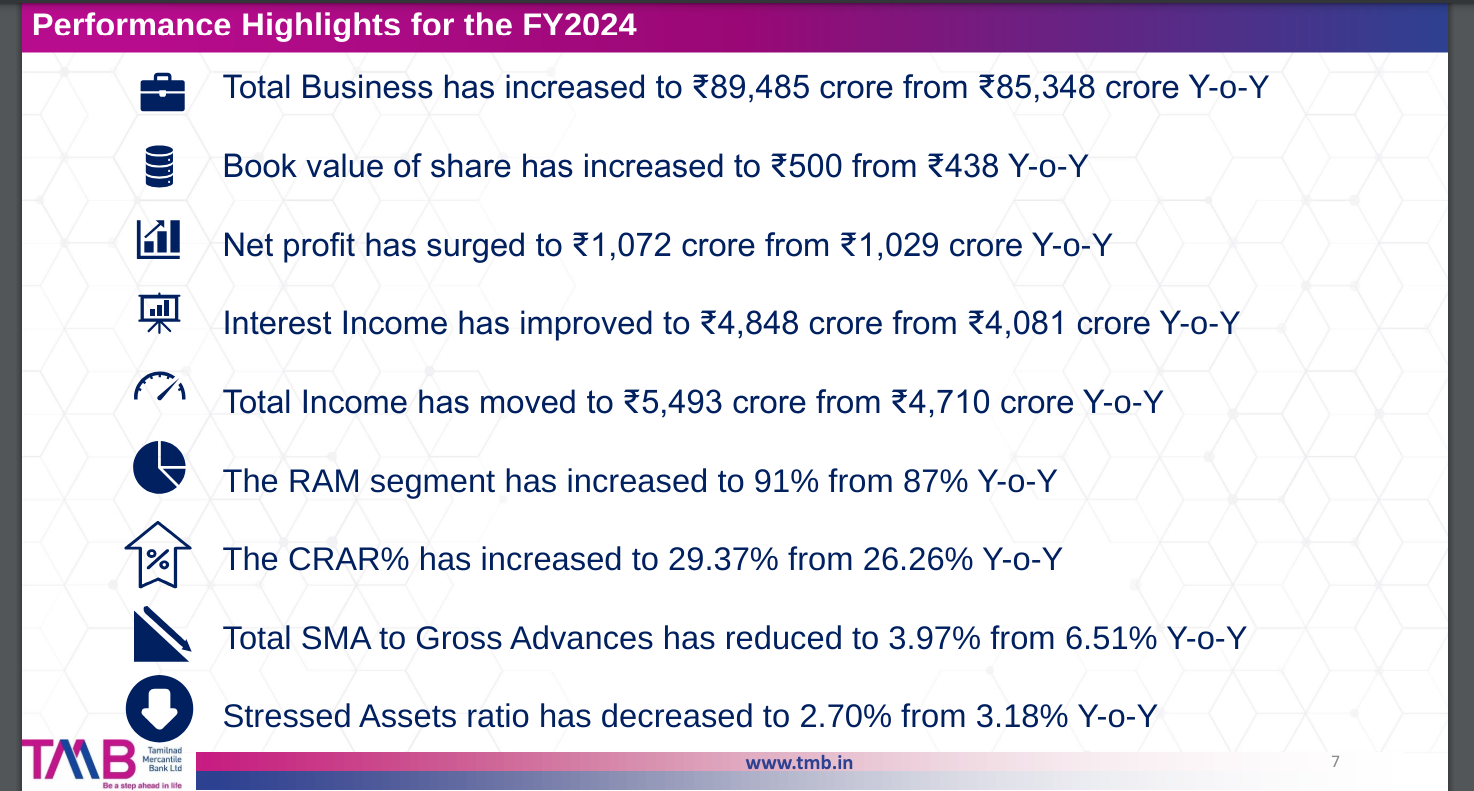

Revenue stood at ₹4,710 Cr ( CAGR of 4.63% in the last 5 years )

Net profit stood at ₹1,029 Cr ( CAGR of 33.17% in the last 5 years )

Advances stood at ₹37,289 Cr ( CAGR of 9.43% in the last 5 years )

NIM is at 4.46%

ROA is at 1.97%

The book value of the bank is ₹6,928.34 Cr, which gives an ROE of 14.86%

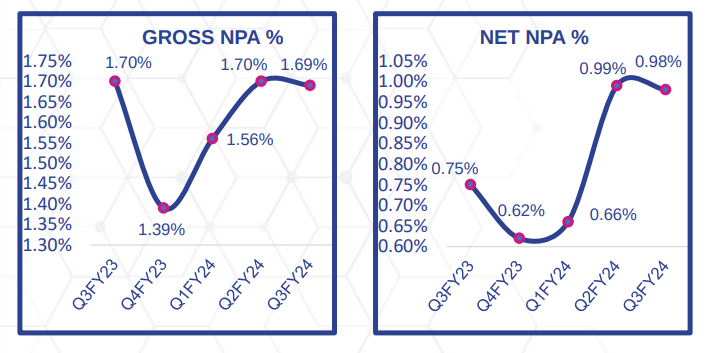

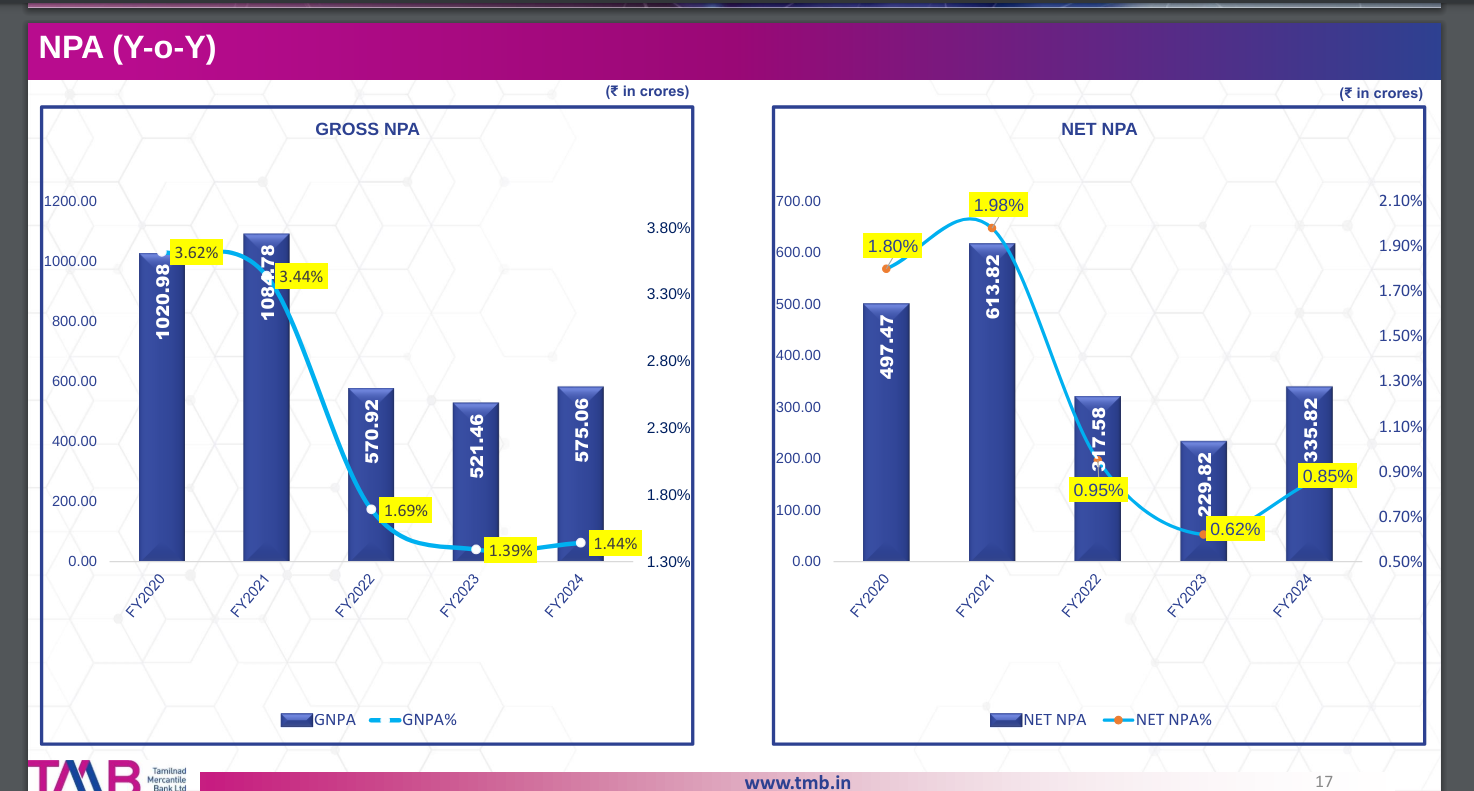

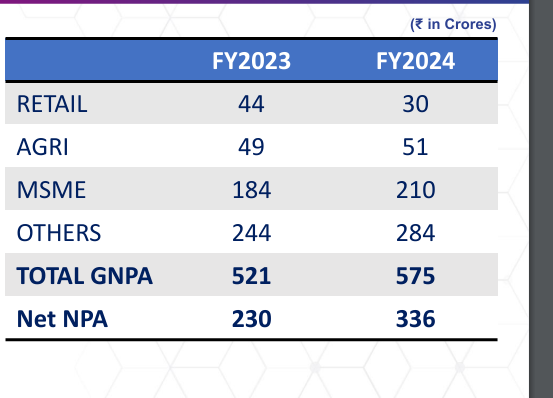

In FY 2018- 2019, The GNPA and NNPA of the bank stood at 4.41% and 2.40% respectively, which was drastically improved to 1.40% and 0.62% in FY 2022-2023. An improvement in their asset quality aided in their profitability growth.

The PCR is great at 90.9%.

The management guides that the bank will try to maintain their GNPA below 2% and NNPA below 1% while having PCR above 85%. They target the loan book to grow at 10 to 12%.

Bank’s Total CRAR stood at 26.26% out of which 24.61% is Tier-1 CRAR. It’s a well-capitalized bank with good asset quality.

It has around 530 branches across India, out of which 386 branches are in Tamil Nadu which creates a concentration risk. Next 6 states with more branches : Andra Pradesh – 27, Maharastra – 23, Gujarat – 22, Karnataka and Kerala – 21 each.

RAM (Retail, Agriculture and MSMEs) segment contributes to almost 88% of the loan book. The rest is Corporate loans. The management aims to keep the loan ratio (RAM-Corporate) at 80-20. In RAM segment, the bank aims for low ticket sized loans.

It’s a conservative lender with very low exposure to corporates and more than 98% of their loans are Secured loans.

Their Yield on advances is at 9.43% and cost of funds is at 4.71%

The slippage ratio is at the lowest in the last 5 years – 0.82%

As of Mar 2023, The CASA stood at 29%, which is considered low for a lender. The management aims to open new branches in areas where they can have a quick break-even. They also aim to achieve CASA of 30 to 35% in the next couple of years.

Let’s move on to the other side of the coin.

The Legacy Issues :

As stated above, the Bank was formed by the Nadar community members and they believe that TMB is a gold mine, built by and for the community. In 1994, due to some internal disputes, a group within the community sold 67% of their stakes to the Essar group for around ₹28 Crores. But RBI opposed the deal.

In the meantime, Mr.C Sivasankaran of Sterling group bought those stakes from Essar group for an undisclosed amount. This stirred a great deal of controversy within the Nadar community. Realizing their mistake of selling their stakes, they decided to join hands and formed a group called ‘The Nadar Mahajana Bank Share Investors Forum’ to buy back those stakes from Mr.Sivasankaran. It was told that Mr.Sivasankaran asked ₹155 Crores for his stake. In 2007, the Nadars managed to buy nearly half of Mr.Siva’s stake but they failed to aggregate the amount to buy back the entire stake.

Again in 2007, a group of 18 foreign investors led by Katra holdings which is owned by Mr.Ramesh Vangal and some other people from the community acquired the rest of the sterling group’s stake. By 2011, Katra holdings sold it’s stake to Standard Chartered Bank, for which the ED released a show-cause notice for contravention of the Foreign Exchange Management Act.

As of today, the bank states that 37.61% of it’s paid-up share capital are subject to legal proceedings.

The Income Tax Department Raid :

On July 2, 2023, the I-T Department conducted a surprise raid on the Bank. According to the I-T Department, the bank has not filed statement of financial transactions (SFTs) pertaining to cash deposits of over ₹2,700 crores involving more than 10,000 accounts and also found discrepancies in specified credit card payments involving total transactions worth ₹110 crores, dividend distribution of more than ₹200 crores, and shares issued for over ₹600 crores.

Source : Mint

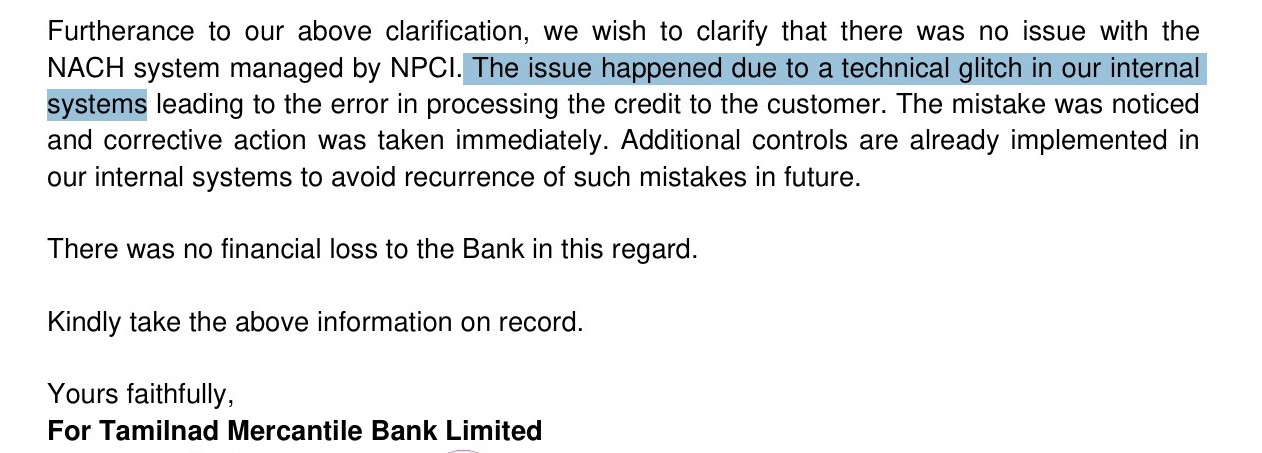

Later the bank stated that this was due to an internal technical glitch and the errors were rectified.

The 30 minutes Billionaire Taxi Driver :

On September 9, 2023 at around 3 pm in the evening, a taxi driver in Chennai received an SMS from his bank stating that his account was credited with ₹9,000 Crores.

With disbelief, he checked his account balance and found out that the amount hadn’t been reflected (It displayed his original balance which is around ₹100). He decided to transfer ₹1,000 to his friend’s bank account to verify the authenticity. To his surprise, the amount got transferred. Now again he tried transfering ₹10,000 and the transaction was successful. He transferred another ₹10,000 after that. Now in total he transferred ₹21,000 from his TMB account to his friend’s bank account. After 30 minutes, he received another SMS from his bank stating that the entire remaining amount has been debited from the account.

According to Mr. Selvaraj, assistant editor, Crime department, Times of India,

The next day, the taxi driver was approached by two anonymous individuals via WhatsApp and SMS demanding that the transferred ₹21,000 should be paid back and threatened him by stating that they would file a police complaint against him if he failed to do so. The driver hired a lawyer and met with the bank’s team in Chennai and said that they would be filing a police complaint against the bank before moving any further. Now, it was said that the bank doesn’t want to file a legal complaint and suggested that the driver doesn’t need to repay that ₹21,000.

Clarifications from the Bank :

Yet another technical glitch at the Bank’s end.

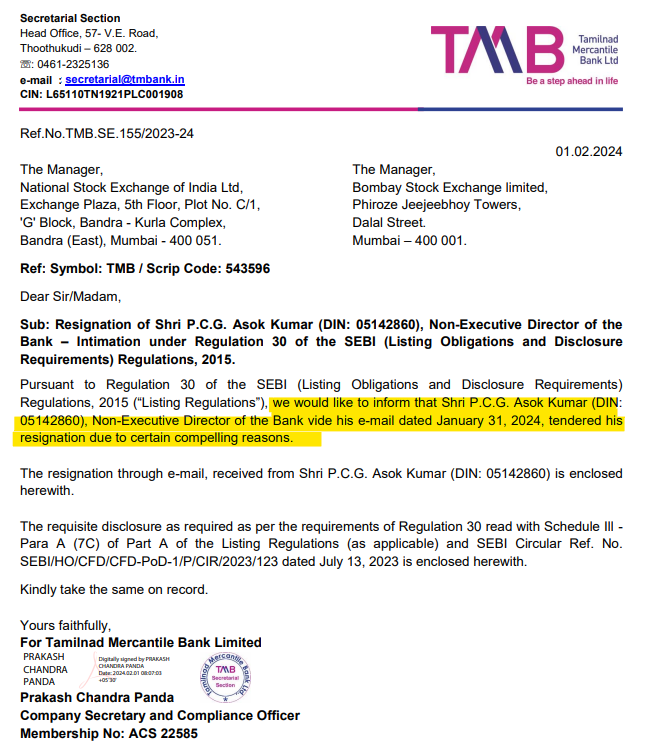

The Resignation of MD/CEO :

Mr. S Krishnan was appointed as the MD and CEO of the bank on September 4, 2022 for a period of three years which was approved by the RBI. On September 28, 2023, Mr. S Krishnan tendered his resignation citing ‘personal reasons’. The Board of Directors of the Bank in their meeting held on September 28, 2023, accepted his resignation and forwarded the same to the Reserve Bank of India (RBI) for their guidance or advice. Till the guidance is received, Mr.S Krishnan shall continue to be the MD and CEO of the Bank.

Some additional points:

• Two RBI nominated directors are present in the board (A possible red-flag).

• Mr.B. Prabakaran, Independent Director of TMB Ltd is also a whole-time director of Sree Ayyanar Spinning And Weaving Mills Private Limited, which is owned by Pioneer Asia Group.

Mr.A. Niranjan Shankar, Director of TMB Ltd is an immediate relative of Mr. S. Annamalai. Mr. S. Annamalai is a director of Sree Ayyanar Spinning And Weaving Mills Private Limited and the MD of Pioneer Asia Group. This raises a question in Mr.B. Prabakaran’s ‘independence’ in the board.

( In March 2016, The FII backed faction led by Pioneer Asia Group’s Mr.Annamalai elected to TMB Board )

• It was said that, in September 2016, The then-company secretary Mr. Deepak S was forced to resign due to the opposition he expressed in the matter of some share transfers and the issuance of bonus shares.

Disc : Having some tracking positions.

Q1 Result Analysis and future growth prospect in Tamil")