TAMIL NADU NEWSPRINT AND PAPERS LTD (TNPL)

Brief introduction:

In these digital days, it appears out-of-place to talk about paper and much less about paper companies. What one overlooks is the fact that the e-commerce age has brought in demand for paper boards while continuing the demand for other types of paper save newsprint.

In this context, I thought it is worthwhile, to look at the leader of the paper industry, Tamil Nadu Newsprint and Papers Ltd., Incidentally, the company does not produce newsprint. It produces printing and writing paper and other types of paper including one for playing cards and paper boards. (page 64 of annual report 2016-17)

TNPL has grown from a 90,000 tpa single mill in 1984 to a 6,00,000 tpa two mills by 2017. In the course of this 33 year journey, it has set up

- pulp mills — capacity expanded from 520 tpd in 2007 to 1180 ted by 2017,

- power plants — 26MW capacity in 1984 to 138.62 MW capacity by 2016

- wind farm —capacity moved from 15MW in 1994 to 35.5 MW in 2017),

- cement plant — capacity 900 tpd

- bio-methation plants (to treat waste water),

- Clonal Propgation and Research Centre — for producing and supplying high yield seedlings and clones to farmers.

- plantation schemes to support farmers — 1,20,715 acres of pulpwood plantations involving 23,287 farmers.

All these expansions and auxiliary units were funded through internal resources and borrowings. At no point of time, the company diverted the moneys to far flung areas leave alone to non-synchronised diversifications — it never moved out of it’s core geography in Tamil Nadu for manufacturing purposes.

The following paragraphs contain selected excerpts from the annual report 2016-17 about industry and company interspersed by my comments and statistical table of performance.

INDIAN PAPER industry:

“Indian Paper Industry is highly fragmented with over 750 paper mills of varying sizes spread across the Country. Only 50 mills are of a capacity of 50000 tpa or more. The overall capacity utilization is estimated at 90%.” (page 62)

About Printing & Writing paper:

“During 2010 and 2011, many mills in the country had added capacity. Supplies exceeded demand and prices dropped. Paper Industry faced acute shortage of pulpwood during 2013. Few mills resorted to importing pulpwood at higher prices. With the steep increase in input costs, paper prices rose during 2013. However, with the paper prices softening in the international market and import of paper in large volume under Free Trade Agreements (FTA), paper prices dropped sharply during 2014 and 2015. The Indian paper industry faced unprecedented challenges both on cost front and market front for two consecutive years 2014 & 2015. The market recovered and stabilised during 2016-17 due to consistent growth in demand and sudden drop in supplies. The shortage in supplies was met through imports mainly from Indonesia and China.” (pages 28 & 29)

About Packaging Boards:

“The market for Packaging Board is estimated at 3.00Million tonnes. Grey-Back Board account for 1.35 Million tonnes (45%), White-back and other high-end varieties (FBB, SBS, Cup Stock.) account for the remaining 1.65 million tonnes (55%). The demand growth for packaging boards is estimated at 12% per annum.” (page 29)

Current state:

“Total installed capacity of Indian Paper Industry is approximately 13.5 Million Metric Tonnes and average capacity utilisation is 90%. Overall consumption inclusive of imports and net of exports is about 14.70 million metric tonnes.

The average per capita consumption in India is around 11 kgs against the global average consumption of 56 kgs.

The growth rate of paper across the globe is around 1.5%.

With the consistent economic growth and greater emphasis for education, the demand growth is estimated at 6%, consisting of 4% in Printing and Writing paper, 12% in Industrial and Packaging Board, 3-4 % in newsprint and specialty papers.

Excise duty on paper remains at 6%. Basic Customs duty is levied at 10% for printing and writing paper & Boards.

Imports from countries covered under Free Trade Agreements (FTA), are levied basic customs duty at zero percent.” (page 28)

“At the current estimated demand growth at 6% per annum, the domestic consumption is expected to reach 25.30 million metric tonnes per annum by 2024-25. This offers a good opportunity for capacity addition.” (page 29)

“The per capita consumption is around11 kgs against the Asian average of 40 kgs and World average of 56 kgs. India is considered as the fastest growing market for paper in the world with an average annual growth of 6%. The domestic consumption is expected to rise to 25 million tonnes by 2024-25.” (page 62)

No major expansions are in sight for the next three years (JK Paper annual report). TNPL is planning to enhance the capacity of its Unit II by 1,65,000 tonnes (27.5% of its existing overall capacity and 1.22% of overall India’s capacity) to commence operations by June 2020, subject to approvals from environment ministry.

My views:

The industry, going by the comments in the annual report, is on balance in terms of demand and supply both in India and worldwide. Hence, companies in the sector enjoy limited pricing power though not tremendous due to

-

commodity nature of the product. Branding of paper, though improved in the last few years has not reached even the proportions of cement. And companies other than ITC have not really embarked on a major branding exercise with the customer at retail level.

-

lack of capacity constraints. Pricing power depends upon capacity constraints on the back of a higher growth rate of demand. Yes, there is a 6% estimate of demand growth. But the industry is operating at 90% capacity and companies have the ability to squeeze in a higher operational rate than stated capacities (both TNPL and JK Paper are operating at >100% capacity).

-

fragmented industry

-

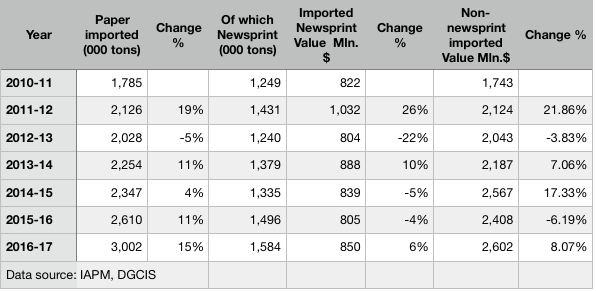

duty-free imports from ASEAN as per trade treaties. These ASEAN nations are at an advantageous position than an average Indian company due to availability of raw material at proximate areas and consequent low cost of transportation. In fact, in JK paper’s AR, management says that the domestic transport bottlenecks weigh against imports. Here is the table of imports into India for the last few years:

While granular data country-wise is available and it could be figured out how much dutiable and non-dutiable imports took place, I thought this broad data is sufficient to draw conclusions. This table shows that in the last three years, the non-newsprint value imported is almost stagnant.

TNPL’s AR states that there was drop in supplies and shortfall was met through imports from China and Indonesia. Perhaps, they were indirectly referring to the drop in sales of BILT by >50% (consolidated revenues fell from ~Rs.4500 Crores to ~ Rs. 2200 Crores — drop of ~50%) and part of that shortfall is being met through imports. If we see the table above, imports rose by ~ 194 Million USD or ~ Rs1,220 Crores from 2015-16 to 2016-17 which is equivalent to, ~ 50% of the drop in revenue of BILT.

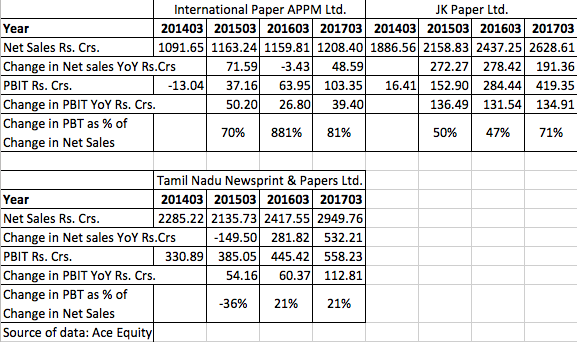

This helped the industry to gain some pricing power as can be seen from the table below.

In Fy17, the rise in PBIT in rupee terms as proportion of rise in sales in rupee terms shows the pricing power of the companies. In case of TNPL, the rise could have been much higher but for production stoppages due to lack of water etc., in Q4 of FY17.

For the pricing power to come into the hands of producers, industry should get defragmented. For that existing large players with strong Balance Sheets should buy out small players. BILT with its over-exposed BS cannot go for acquisitions. While ITC which is one of the largest players has wherewithal to do acquisitions, we have not yet seen it moving in this direction yet. TNPL is judiciously using internal accruals and debt to do brownfield and greenfield expansions besides building some auxiliary capacities in related fields and does not look like thinking about acquisitions. That leaves, JK Paper, Trident group, International APPM, Orient paper etc., in the listed space to make the moves for acquisitions. It may take a while for them to clear the existing debt and take aggressive bets on acquisitions.

The key takeaways for the industry at this moment are

1. currency appreciation/depreciation of ASEAN countries relative to INR could change the fortunes of the companies

2. watch keenly for announcements of acquisitions.

World Paper industry:

Broadly, the industry is classified into four main segments - namely, writing and printing papers, Industrial paper, speciality paper and newsprint. India holds 15th rank among paper producing countries in the world with a total installed capacity of 13.50 million tonnes. The demand is estimated at 14.70 million tonnes. (page 62)

About the company:

TNPL is operating at more than 100% stated capacity in paper. Its paper board plant was commissioned in May 2016 and production was 53% of stated capacity in Fy17.

Raw Material:

“TNPL is the largest producer of paper using bagasse an agricultural residue from the sugar industry as primary raw material. TNPL uses about 1 million tonnes of depithed bagasse for producing 4,00,000 MT of Printing & Writing Paper. TNPL sources bagasse from sugar mills. Long term agreements have been entered into with eight sugar mills in the State for sourcing bagasse in exchange of steam. Shortfall is met through open market purchases and temporary tie-up arrangements with sugar mills.” (page 63)

Cost control:

“The weighted average cost of loans outstanding as on 31.3.2017 is 8.78% (31.03.2016: 9.56%). This was further reduced to 8.55% as on 26.05.2017 through swapping of loans and switching over from base rate to Marginal Cost Lending Rate.” (pages 62 & 63)

Perhaps, this is the only paper company in India which has 100% captive power supply. In 2016, along with commissioning of the paper board mill, the company commissioned second power plant also.

“TNPL has 138.62 MW power generation capacity comprising of four power boilers and four turbo generators with a power generation capacity of 103.62 MW in Unit I and two power boilers and one Turbo generator with a generation capacity of 35 MW in Unit II. TNPL is 100% self-sufficient in power. Surplus power is exported to TANGEDCO.” (page 64)

Company makes best use of the waste also. It manufactures cement also.

Going forward,

The company is planning expansion to enhance the capacity of its Unit II (the board plant) by 1,65,000 tonnes. It is expecting to complete the project by June 2020.

Important statistics:

Promoter: Governor Tamil Nadu — holds 35.3196% of equity

Largest non-promoter shareholder — LIC of India — holds 9.1112% of equity

Total indebtedness : Rs. 2,092.35 Crores — March 2017

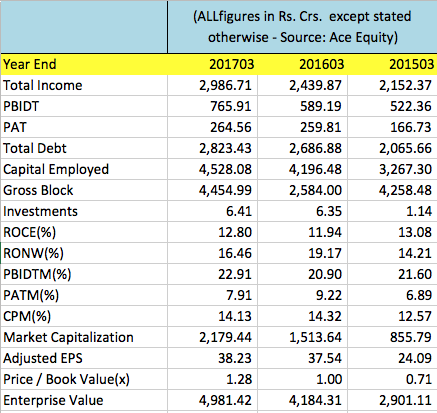

These are the financials of the last three years

In the first quarter of the current year, company incurred loss of Rs. ~89 Crores due to shortage of water. Normal operations resumed from July-end.

Valuation:

If we consider last year’s EPS of Rs.38.23 and price of Rs. ~342/- as of 25th Sept 2017, company is trading at a PE of ~ 8.9x and market cap of ~ Rs.2,400 Crores. Since it is in an industry that is boring for investors, in spite of RONW of 16.46% and a P/B of ~ 1.38 giving an yield of 11.92%, company is trading at such valuations.

Disclosure: I do not own this stock.