Howdy Value Investors!!

I am very grateful to the knowledge I have been acquiring from this group!

This is my first stock pick please forgive me for any mistakes!

The company I am talking about is the Talwalkars Better value Fitness Ltd is Established in 1932, by late Vishnu Talwalkar, his eldest son - Madhukar Talwalkar, further continued the legacy under the name “Talwalkars Gymnasium” in Bandra, Mumbai in 1962 and the brand has been rapidly growing since then. Today Talwalkars has 80 years of rich experience in health and fitness industry.\

The fundamentals are quite impressive

Profit growth 5 years is 53%

P/E is reasonable around 17

Enterprise Value to EBIT: 11.85

Piotroski score: 7.00 ( I like to know whether the company is financially good.)

Consistent Profit Growth from the past 10 years.

Future prospects are good they joined with the 50:50 joint venture with David Lloyd Leisure Limited for

establishing and managing leisure clubs in India. David Lloyd is famous in UK for their leisure clubs.

(Recently, the share price declined due to the Talwalkars recently raised Rs 107 crore through a Qualified Institutional Placement the company had issued 35 lakh shares at a price of Rs 305 per share)

According to the peter lynch i got this company. I actually used to go to this gym in my town and they are well designed and maintained and crowded in summers(Good student offers). I once talked with the gym manager he said the only concern is the salaries are less but when i questioned about the growth of the business he said it’s pretty good.

I am just trying to start a discussion here on this business. If the seniors or other members can share their views, I’ll be most grateful.

Disclosure :- I don’t hold this stock in my portfolio.

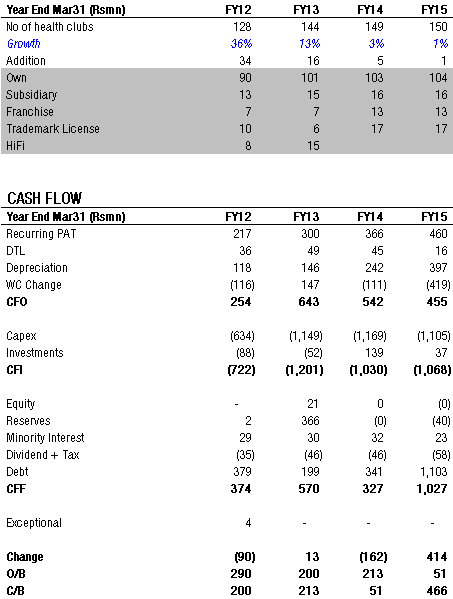

I was a shareholder for the last 3 years. Sold out recently after it gave 100% returns. The sales and PAT growth is very impressive. But there are few things which make me very uncomfortable about this company: The debt/ equity which keeps going up. Very low RoCE. Post tax (tax rate is 30%+) it is 10%. So this company is actually not making its cost of capital

The most worrying part is this. Last year company added 1 gym only and capex was Rs110crs. 110crs for 1 gym is amazingly high. So one should ask following questions: " Where is capex going? To add gyms or …??? Is it possible that company is classifying opex as capex to show higher EPS, RoE and that is why despite decent CFO but FCF is always negative? Read above in conjuction with the fact that promoter shareholding keeps declining every quarter.

I am also unsure how they account for gym fees. If you join a gym you pay an upfront fees for 6 or 12 months. Do they amortize the sales over 6 or 12 months or book lumpsum immediately. I cannot believe the economics of gyms are so poor seeing RoCE and leverage.

Economics of gyms are poor. I don’t have the quantitative numbers, but some scuttlebutt around here in Bangalore shows that for Golds Gym, typical franchisee is either politically connected or are people who don’t worry much about returns (I.e it’s not the primary business and the business returns do not materially affect the franchise holder).

It takes at least 2-3 years to break even on an opex basis, recovering the entire amount plus fair returns is a very long term play indeed. Many gyms are just a real estate play by franchise holders.

In one sense the biz is not different than an upscale restaurant. You need to continuously acquire new customers, one customer can only give you a profit of a few thousand at max and worst, gyms are not a natural draw like movie theaters (most people hate going to gyms). Charging a premium even for Golds Gym is actually hard since most big apartment communities now have basic or better equipment anyway and offer better convenience.

At some point in the distant future these might end up becoming asset plays, but I’m not sure about that either.

Talwalkars - Q4 Concall Update – To maintain SSG growth of 9-10%

Key positives –

• Reported Revenue growth of 20% yoy without adding any new gym this year driven by higher share of value-added biz, increase in memberships and some increase in value growth this year.

• SSG growth registered at 9-10% and management guided that they will continue to post similar numbers going forward

• Contribution of Value Added Service has saw significant improvement from 16% last year to 23-24% this year. Expect Value Added contribution to reach 40% in next couple of years

• Rent negotiation: Company is in constant negotiation with the land lords to either reduce the rentals or prolong the increment in rent rates. Management has seen those rentals coming down with few landlords they have interacted recently.

• Possibility of increasing dividend payout: Management indicated that with opening of the new club in Pune next year company will certainly look for increasing its payout if response for the same is good. Company announced Rs 1.5/sh dividend for FY15.

Key negative -

• Company is now under full tax vs MAT. For FY15, tax expense increased 38% yoy with eff tax rate of 33.6% vs 30% yoy.

• Possibility of increased rentals in few centers will come in as there is 15% escalation every three year. Management did not provide the number of centers which will see increase in rentals as company is re-negotiating the terms with the landlords as mentioned above.

• Higher depreciation on account of refurbishment of equipment and new clubhouse. For FY15, depreciation cost increased 64% yoy to Rs 40cr

Strategy going forward -

• Clubbing opportunity: Company is setting up a club in Pune with capex of Rs 50crs and another one in planning stage in Mumbai. Pune club will be operational and start generating revenue by Q4FY16 and Mumbai one will be operation by Q4FY17. For Pune, Membership entry fees is being fixed at Rs 5 lakh and expect to get 1000 members in 2 yr time which will cover the capex incurred for the club. However, cash flow will be reflected as it comes, the income will be recognized and amortized over the period of membership.

• Premium gym: Company has opened a premium gym in Banjara Hills (Hyderabad) which has given a very good response. Company had the footprint there for last 10years and have upgraded the offering by opening up a big size (biggest in South India) gym with latest equipment. Company already have 1400 members there and is charging Rs 30-33000/pa membership compared to Rs 18-20000/pa membership charged by the competition in Hyd. Success of the same will be replicated in other metros where they have strong footprint.

• Integration of Nuform as part of fitness centres as a value added measure in phased manner. Initially targeting to install equipment in 40-42 locations in Q1FY16 and gradually rampup the integration in all its centres in next couple of years.

• Active marketing of Value added services: Company currently offers Reduce (weight loss program), Transform (Fitness program), Massages (spa program), Zumba and TRX (group exercise program) across its centers. Apart from these, company also offers personal training program to its members. The improvement has been seen this year and expect the growth to continue.

• Re-initiating their expansion plans: Company has delayed its expansion plan witnessing high rental prevailing in the country and has not opened any center this year. However, recent negotiation with landlords saw rentals coming down 20-25% below the quotation of Nov-Dec’14. Company earlier planned to add 250 centers in three year time and will pursue expansion selectively. Company is also looking out for acquisition of local gyms which was not available as an option a year back and transform them into Talwalkars brand which will be more cost effective and less capital intensive

Capex and Debt -

• Capex: For FY15 company did capex of Rs 80-85cr of which Rs 25cr spent on Club and remaining in refurbishments and revamping of existing centers into Nuform equipment. For FY16, company plans to invest Rs 75-85crs.

• Debt: On Consol basis, gross debt stands at Rs 300crs vs Rs 170crs last year. Increase was on account of Debenture they raised at cost of 9.8% which led to blended cost came down 250bps.

@vnktshb - capex portion i think went in clubbing side which mgmt said they spent 25cr there (in call they mentioned 80-85cr capex for refurbishment of existing centers and clubbing capex of 25cr)…company recently tied up with a UK clubbing “Talwalkars and David Lloyd Leisure Limited announce Intention to create 50:50 joint venture to develop leisure clubs in India - BSE Announcement”, this will shift some capex to the JV partner and reduce risk of the venture. On expansion, management clarified that they didnot participated for new gym due to hig hrentals but they started seeing rentals coming down and will pick up their expansion plans in Fy16.

Disclosure - not holding any position, but tracking it nevertheless…hope its useful.

Hi Venkatesh! Thanks for the insight, for the Capex part, is it not possible that the Talwalkars are adding new equipments to their older gyms? ( Its an 80 year old company, so equipments will get replaced ). Obviously I don’t see any accounting shenanigans in the Capex part

I haven’t done in depth research in Talwalkars Gyms, but it won’t surprise me if the company is not making the cut. Customer loyalty always remains a big issue, since a new gym with modern equipments and facilities always springs up in 1 or 2 years in the locality, and the present gym needs immense improvements and maintenance.

I would be more interested in owning a gym catering to clients with lower income/budgets for fitness, since here people would not care about infrastructure.

In my opinion, a gym with high volume-low price is better business than low volume-high price

Hi @vnktshb,

I liked the way you made your point. I also liked the info on number of health clubs and the growth. May I request to know how you got the data neatly tabulated the way you presented it? Was it from a site? Which one? I saw the FY15 annual report and didn’t find the info tabulated there (although the numbers would be strewn across the pages). Thanks in advance.

I used to be a shareholder of the company. When I buy small and mid caps I build a historical model. So all that data is sourced from the historical annual reports and presentations of the company available on the website

In last 6 months, promotors reducing their stake in the company, QIP of 107 Crores (at price of 305 per share) thereby expanding equity by 13.5% brought stock down from Rs 400 to current price of Rs. 250.Their 50:50 JV with David Lloyd Leisure Ltd UK in club business would be a drag for short term.

But I think health club business is a lifestyle play which is long term trend in developing country like India. % of penetrations of health clubs is poor as compared to developed world. With Market cap of 736 Crores, trailing PE value of 17 and 5 years compounded sales growth of 25% and profit growth of 40%, I think this stock is attractively priced.

Please see recent new item in money control

Disclosure : invested from lower levels. No new investment in last 90 days.

There is another privately held company by name of Talwalkars Fitness Solutions Pvt. Ltd. which has no relation with Talwalkars Better Value Fitness Ltd. Their company website is as below http://www.talwalkarsgym.co.in/

Talwalkars Fitness also call them Talwalkar’s Gym and has defrauded many members in various parts of Maharashtra. Some news items are as below

It is really hurting Talwalkars Better Value’s brand image as common man tend to feel that these 2 are same companies. I think as the two families share the same last name, Talwalkar’s better value can’t do much about it.

Talwalkars have decided to expands beyond India. First strategic investment in neighboring Sri Lanka in Power World Gym having similar customer and margin profile. I think good use of QIP proceeds which would help to improve ROE. This is much better fit and use of investment than club JV. This should stock gets it “mojo” back.

Talwalkars is taking acquisition route to grow beyond their strength in Western region. First buying stakes in SriLanka based Gym, them Chennai based Gym and now Chennai based Yoga firm. This will not only increase their footprint but will also add “value added” services to their offering thereby improving “same stores sales” as mentioned in earlier post.

I also expect “wellness” sector getting re-rated once VLCC IPO hits the market later this year, due to paucity of stocks in this growing sector. So all signs pointing at the right direction.

Good Q3 numbers,like all quarters. Sales up 14%, PAT up 21%. Planning to add another 100+ gyms in next 3 years. Sames Stores Sales Growth at 9.7%. Increasing foot print by organic and inorganic route and robust SSSG would help to wake up this stock from long sleep

The rates offered by Talwalkar Gym are expensive for ‘c’ class cities in india. That is why people in small cities are afraid of opening frenchies considering ROI.During discussion with Mr.Talwalakar he clarrified that he is targeting those customers who can affords his gym rates. However it is surprising that considering economy and doller rate to srilakan rupee how Talawalkar will be earn money in srilanka market.

Talwalkars Better Value Fitness Ltd: The company informed BSE regarding “Talwalkars Better Value Fitness Limited spreads holistic wellness across India with 33 Zorba - renaissance studios in 25 cities in the span of 60 days”.