Hi,

Comapny announced they’ve 1000 crore order book during last quarter presentation and recently they’ve announced it got 400 crore. These order books are from both domestic and abroad OEM’s. In all their announcments they’ve clearly mentioned these orders are to be executed in the next 5-7 years. From what I understood, from these order book earliest SOP would be FY25. So, on the back of these orders stock has run up a lot. I understand these orders give them a revenue visibility but is there anything special about it?

1.Last year’s total revenue ~650 crore, so total order book is twice this but it is executed over 5 years.

2.Even if we cumulatively count existing customers business without any new orders for a period of 5 years, it is not that difficult to arrive at 1400 crore order book, isn’t it?

I discovered this early but I wasn’t able to answer these questions myself and hence didn’t decide to put my money. Could someone point out how this will affect the company in specific and also in general for any comapny especially when order is spread over long period of time. It’ll be a learning in my investment jouney.

So this is happens when you are trying to correlate current news to stock price rising.

If you go through the last 4 quarters concall and presentation you will see management has been guiding for 20% volume growth CAGR for the coming 3-4 years . At an ROCE of 20 % which in itself is pretty good for any auto ancillary the company should have been at a PE of 20 with these growth forecasts . Earlier due to rate hikes and slowdown in europe the growth did not come last year.

Now with the last quarter sales begin highest quarterly sale with highest operating profit even in a high interest environment. Investors are feeling confident that the company can deliver on their growth forecasts and can grow at 20-25% CAGR at 20% ROCE .

If the quarterly profit for the coming year on average will be around 17.50 Cr, then the yearly net profit will be around 70 cr . At 20 PE for the company should have a market capitalization of 1400, which will put the price target around 1200 for the share .

If you study the company well, they are focusing on very high growth industries and providing material to many EV cars, have developed robust tie ups with various technologically advanced companies to cater to the coming EV adoption for the automobile industry.

Also you will see their operating margins have been highly stable in these times of turmoil signifying pricing power .

All this can give investors confidence to be confident of the growth being stable and even accelerate in the coming years .

If you take into account FY 24-25 profits in account too, the share price can go to 1400-1500 too .

Invested from lower levels.

This is a good explanation. I was thinking why there was atleast 2x more movement in price from previous ( like 2021 ) even though the numbers didn’t change drastically.

Invested ( not so much)

Hi, I studied the company three months prior and invested at those prices. However, my allocation was also influenced by concerns about related party transactions involving their own private limited businesses.

Can anyone tell me whether the transactions are regular or a benefit to the publicly traded firm, or whether management is being smart here?

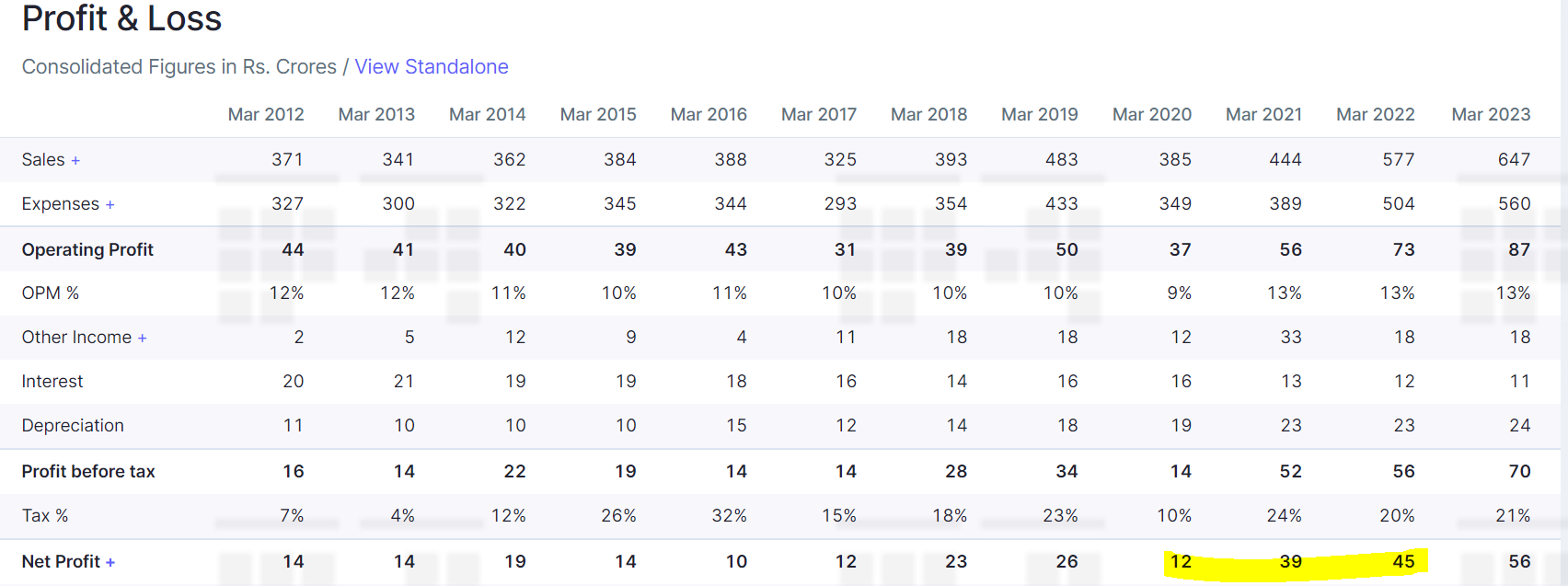

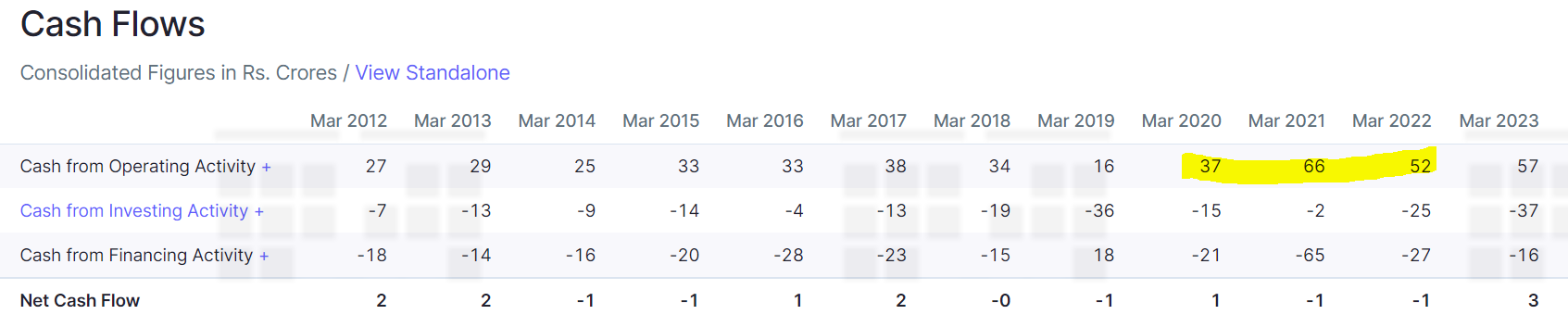

We need to calculate the CFO from PBT not from the PAT. With the indirect method the CFO = PBT+D&A-WC. Look at the inventory days as well, if the inventory increases the CFO gets hit as well, and I see in 2022 & 23 the inventory days have increased which eventually impacted the CFO.

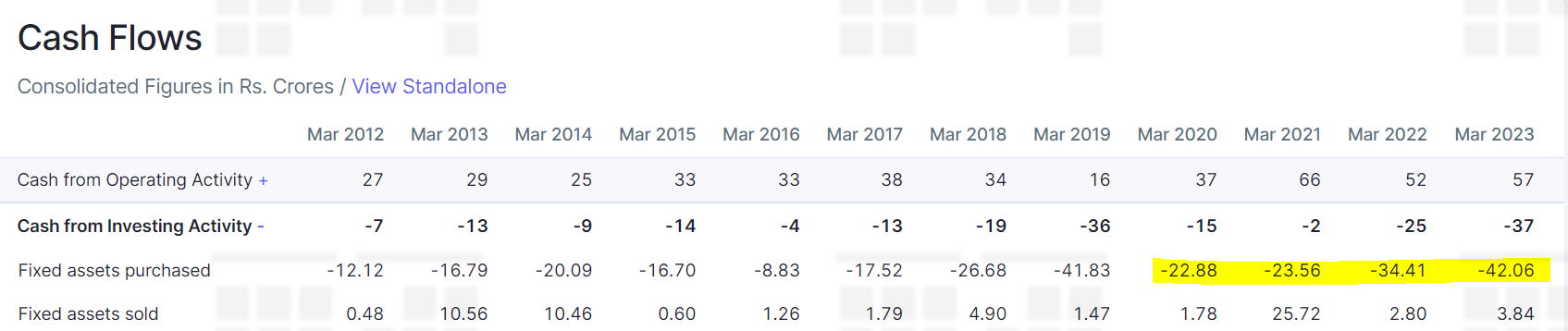

This is the thumb rule, purchase of the investment is covered in investments. Capex will cover the purchase of the property, plant, and equipment of new machinery or any new building. So what I meant with this is when company purchase a fixed asset then it will be reflected in both i.e, balance sheet and cash flow statement

So lets say a company purchased fixed asset of Rs. 100 during an year and out of that comapny paid Rs. 80 to the vendor and remaining is yet to be paid

then in balance sheet fixed asset will be increased 100

In cash flow 80 will be shown in investing activities as purchase of fixed assets as it is actual cash outflow

Thanks and will go through again. But I feel u r talking about the consolidated financials including partner companies, whereas I was mentioning about related party transactions with QH Talbros.

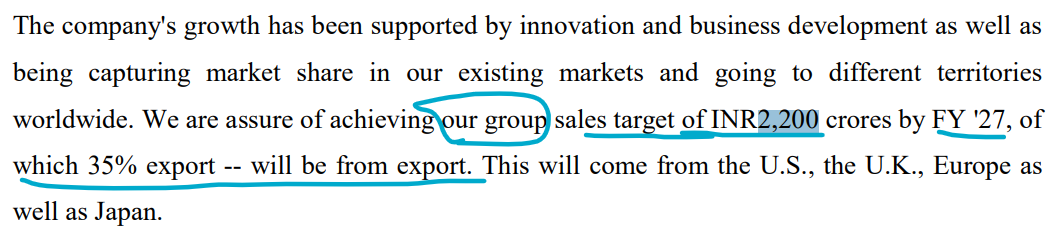

The company aims to achieve a group turnover of INR2,200 crores by FY27, with an export contribution of about 35%

This Rs. 2,200 Cr target for FY27 does not factor in any inorganic growth

Rough distribution of how this Rs.2,200 Cr revenue target will be achieved from different divisions - Forging - INR500 crores plus; Magneti Marelli - around 700; Gasket and heat shield - around INR700 crores; Margo - INR200 crores plus. Even though it does not sum up to 2,200 but closer to it.

More Elaboration on achieving Rs. 2,200 Cr target FY’27 - They have got new orders worth Rs. 1,000 Cr last year; Now the orders are being converted into commercial sales; New orders and new conversions this year, for these orders revenue will be added in next 1-2 years; Economic growth will add to revenue; More customers are added which will contribute going forward; JLR which is the customer added last year, is being converted to commercial sales; Number of Maruti models are increasing which will also help; Company thinks China+1 strategy of global companies helping them; They see opportunity of growth in the US, UK and Germany.

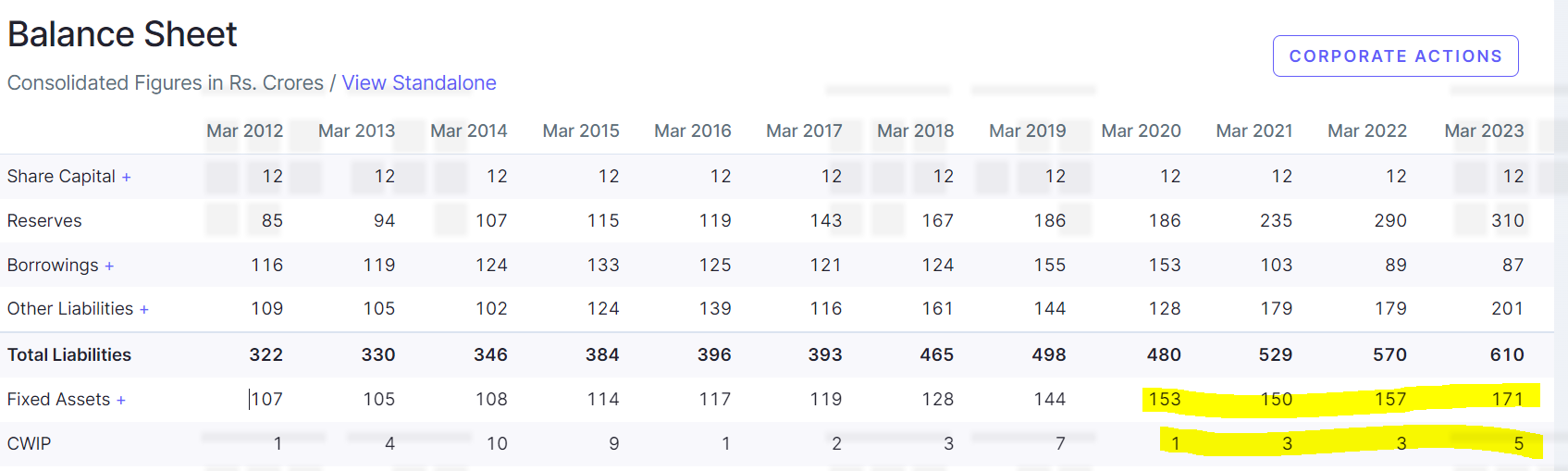

Capacity utilization is in the range of 80-90% at the moment and able to support the revenue of Rs.1,300 Cr. By FY’24 with the additional capex, the capacity will be increased to support the revenue of Rs. 1,500 Cr. Capacity addition happening every quarter. For achieving the target of FY’27- They foresee capex of ~ Rs.200 Cr.

With regards to revenue growth for FY24 and FY25, the management guided for over 20% growth on consolidated revenue, with Ebita margins at 15% for FY24; Whereas for FY25 management guided for 15-20% growth based on current visibility; The analyst, rightfully challenged that - the guidance for FY24 and FY25 does not really align with the target for FY27. Because with Rs. 650 Cr revenue in FY23 - with 20% guidance they can reach to Rs. 940 Cr by FY25. To that management answered that they are confident of reaching that Rs. 2,200 Cr by FY27. Considering they are talking about Rs.1300 Cr possible with current capacity and they are increasing capacity during this year itself, implies they want to be conservative while providing guidance for FY24 and FY25.

Guidance on ROCE for 2025 - Management answered RoCE-40% (FY23 - 20%) & ROE - 25%(FY23 - 17.8%). I presume, they have given number for FY25 and not FY27

On the question of reducing the % of Ebita conversion to cash, Management suggested that due to increase in export the cash conversion cycle elongates.

Net net - Management seem to be seeing good traction in exports. The orders that they have own over past 12-15 months will get commercialized over next 12-18 months. With china+1, they are hopeful for getting more business and that is leading them to believe in achieving the ambitious target of Rs.2,200 Cr. with slight improvement in margins (~15%). If the tailwind remains intact and management executes well, there is a bigger multibagger in the making.

Disc - Invested from lower levels; Not transaction in last 1 month.

Major products Gasket to require less in EVs. Other products will also be obsolote in EV transition.

company is not distributing sufficient divident . Do they get sufficient money in related party transactions through 100 percent owned private companies ? If promoters are honest , why did not they make their pvt. company QH Talbros as subsidary of listed companies ?

NLK - JV wth Nippon making gaskets

89 Cr Income; 35.6 Talbros share

33% PAT margin

MTCS - JV with Marelli, Italy making chassis components like control arms, suspension links etc

210 rev (27% increase), 105 share talbros

11% PAT margin

TMR - Talbros Marugo Rubber makes rubber molded products

Best supplier for Maruti Suzuki

85.3 cr (55% increase), 43 cr Talbros share

6.5% PAT margin

Expect higher margin businesses to increase consol margins further. Moreover, it will be a LONG while before EV growth over ICE will incapacitate core business of gaskets, if at all. Co’s EV product segment expansion should balance it out either way.

“Talbros Automotive Components Limited has received new multi years orders worth~Rs.580crores from both,domestic and overseas customers across its business divisions, product segments and JVs. These orders are to be executed over a period of next 5 years commencing from FY25 onwards covering the company’s product lines– gaskets, heat shields, forgings,chassis and rubber hoses.”

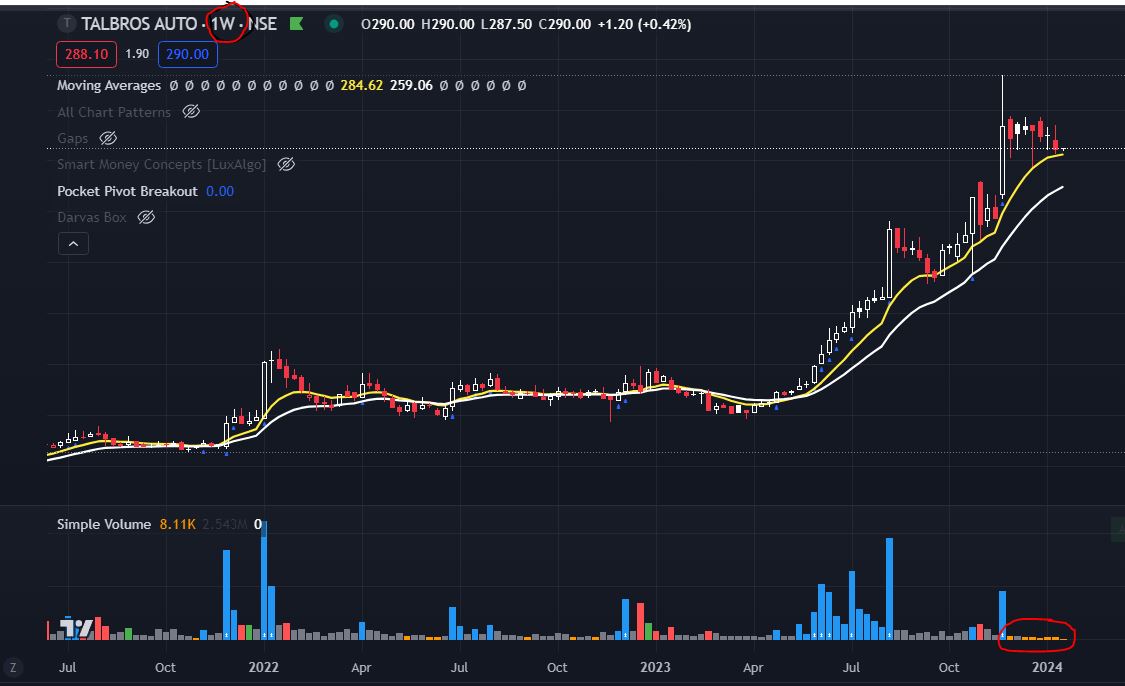

Stock price is up almost 40% over the past 2 days.

I am not sure about the further upside in Talbros. Because if we check the P/E of Talbros it is 27.6 While Bajaj Auto (to whom Talbros is supplying) is at a P/E of 26

I will be grateful if someone can throw some light

I think this alone (comparing PE alone between two companies which are not in same business). We need to understand various other aspects. While you are stating about further upside in Talbros, I am not sure how much duration are you taking into consideration. Irrespective of that, the upside in Talbros will be on account of the growth in next 3 years and improvement in margins. Revenue for FY23 have been about 650 Cr. Whereas management is guiding for 2,200 Cr revenue in FY27. That is more than tripling the revenue in matter of 4 years. With such growth, there is a likelihood of operating leverage playing out. That will help to improve margins. Order wins that Talbros have announced during past 6 months provides a decent indication that the company is likely to achieve the guidance. Having said that - if they show case the guided revenue with consistent margins above 15%, the stock can have decent upside even from here imho.

Disc - Invested with small quantity(less than 1% of current pf)

I think there is some confusion between group revenue and company’s revenue. What they have guided is group revenue of 2200Cr which includes full sales from the JV companies. If you take the Talbros’s share in that JV, company’s revenue will be around 1400Cr. Please correct me if my understanding is wrong.

To be honest I dont know. Below is the snippet from previous concall. I think, its better to be conservative until we see explicit clarification from management about the guidance being for Talbro’s share alone.