Lately, I’ve been researching the hospitality space after governments focus on boosting consumption — especially companies that aren’t in the spotlight but are quietly executing well.

One name that came up was TajGVK Hotels & Resorts Ltd — a smallcap hotel company with premium assets, a strong brand partner, improving financials, and potential long-term value.

Here’s everything I’ve gathered so far. Would love to hear what others think.

About the Business

TajGVK is a joint venture between the GVK Group (Hyderabad-based infrastructure group) and Indian Hotels Company Ltd (IHCL) — the Tata-owned company behind the Taj brand. IHCL owns about 25.5% and operates all of TajGVK’s properties. GVK remains the majority shareholder (~49.5%), and together they hold about 75% promoter ownership.

TajGVK owns and operates six premium properties under the Taj and Vivanta brands, with a total inventory of ~1,240 rooms. These include:

-

Hyderabad (core market):

- Taj Krishna (flagship property)

- Taj Deccan

- Vivanta, Begumpet

- Combined inventory of ~600 rooms

-

Other cities:

- Taj Club House, Chennai – 220 rooms

- Taj Chandigarh – 149 rooms

- Taj Santacruz, Mumbai – 279 rooms (via JV – Green Woods Palaces & Resorts Pvt Ltd, TajGVK owns 48.99%)

Earlier, Taj Banjara (122 rooms) was part of the portfolio but has been shut since Feb 2023 due to lease expiry and returned to the landowner.

Financial Snapshot (as of March 25, 2025)

- Market Cap: ₹3,055 Cr

- Current Price: ₹487 (52W high/low: ₹530 / ₹275)

- P/E: 33.1

- Book Value: ₹90.2

- ROCE: 18.8%

- ROE: 14.8% (3-year avg: 12.4%)

- Profit growth (TTM): 46.2%

- Sales growth (TTM): 11.4%

- Debt-to-equity: 0.16

- Dividend yield: 0.28%

- Return over 3 years: 53%

Latest Performance (Q3 FY25)

- Standalone Revenue: ₹127 Cr (14.2% YoY growth)

- Standalone Net Profit: ₹34 Cr (up 40% YoY)

- EBITDA Margin: ~40% (highly efficient)

- Consolidated PAT (incl. Mumbai JV): ₹41 Cr

- Roughly ₹7 Cr of PAT comes from the Mumbai JV share

The Mumbai JV (Taj Santacruz) continues to be a strong contributor. In H1 FY25 alone, it posted ₹106 Cr in revenue and ₹18 Cr in PAT — nearly 30–35% of consolidated net profit.

Long-Term Financial Strength

- Debt has come down from ₹214 Cr in FY22 to ₹108 Cr in FY24

- As of Sept 30, 2024, the company is net cash positive

- Interest coverage ~7.7x, and debt/EBITDA down to 1.2x

- EBITDA margins have stayed strong (31%+), with high cash conversion

- Company is funding expansion largely through internal accruals and scheduled debt

Renovation and Portfolio Upgrade

TajGVK has been reinvesting in its core assets:

- Taj Deccan: Recently completed renovation of 24 guest rooms and bar (by Aug 2024). The hotel is now fully operational with a refreshed look and feel.

- Taj Krishna: Already renovated in phases (124 rooms done earlier). Continues to be a marquee property in Hyderabad’s central business district.

- Vivanta, Taj Chandigarh, Taj Club House: Fully operational. No major renovation reported recently.

- Taj Banjara: Closed since Feb 2023. The company hasn’t announced plans yet — possibly awaiting redevelopment or re-leasing.

These upgrades are expected to drive ARR growth in the coming quarters. Occupancy has already bounced back sharply — 78% in FY24 vs 55% in FY22, and ARR grew from ₹4,900 to ₹7,900 during the same period.

Bengaluru Expansion – Big Move Ahead

One of the biggest upcoming developments:

- 253-room Taj Hotel in Yelahanka, Bengaluru

- Land allotted by KIADB, 7.5 acres

- Project cost: ~₹326 Cr

- ~75% of the work is completed

- Target opening: Q4 FY26

- Funding: ₹200 Cr debt tied up with Federal Bank; rest through internal accruals

This property will significantly diversify the portfolio beyond Hyderabad and give TajGVK exposure to one of India’s most premium hospitality markets. Once operational, it could meaningfully boost both revenue and visibility.

Taj Santacruz – A Hidden Gem in the JV

Taj Santacruz, Mumbai, is a key asset — though not consolidated in revenue (since it’s a JV), it adds strong profit.

- TajGVK owns 48.99% via Green Woods Palaces & Resorts Pvt Ltd

- FY25 H1 Revenue: ₹106 Cr

- H1 PAT: ₹18 Cr

- Q3 JV PAT: ₹9.3 Cr

- TajGVK’s share of this adds ₹7–8 Cr to quarterly consolidated profit

This is a high-quality asset — large rooms, ideal location, and strong RevPAR. It gives TajGVK indirect exposure to Mumbai without heavy capex.

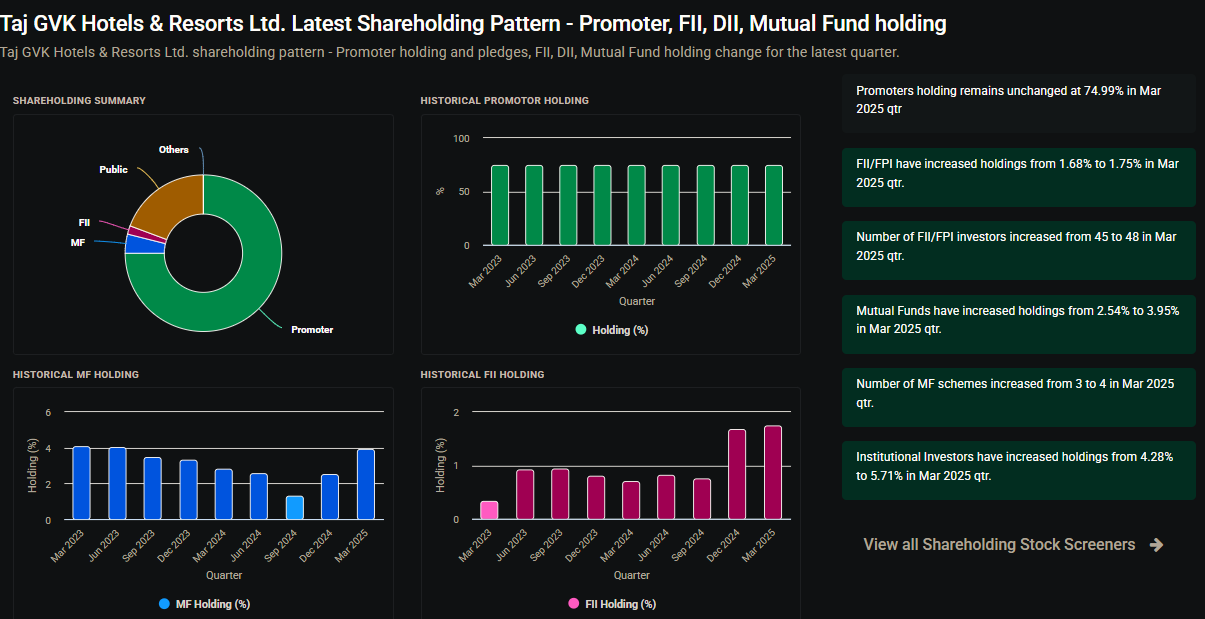

Ownership and Governance

- Promoter holding: 74.99%

- GVK: ~49.5%

- IHCL (Taj): 25.5%

- No promoter pledges

- IHCL is the operator and has two directors on the board

- Institutional holding is rising (FIIs, mutual funds)

- The GVK Group has had legal troubles (airport case), but this hasn’t affected TajGVK directly. The company has no loans, guarantees, or financial exposure to GVK Infra or its group companies.

What I Like

- Backed by IHCL (Tata group) and operated under the Taj brand

- Premium properties in prime locations

- Renovation-led pricing power

- Healthy balance sheet with low debt and strong margins

- Strategic expansion into Bengaluru

- High-margin JV (Taj Santacruz) quietly boosting consolidated earnings

- Minimal institutional coverage, potentially under-owned

Risks & Concerns

- High dependence on Hyderabad (currently ~50% of rooms)

- Capital-intensive, asset-heavy model — slow to scale, lower ROCE than asset-light peers

- GVK Group’s past legal issues could be a sentiment overhang

- Taj Santacruz earnings not visible in top-line; could confuse some investors

- Valuation at P/E ~33 is not cheap, although margins and quality may justify it

What I’m Still Thinking About

- Is this a slow but steady compounder, or just riding some temporary tailwinds?

- Will the Bengaluru hotel meaningfully change the earnings trajectory from FY26 onwards?

- Would this business deserve a re-rating if margins sustain at 30%+?

- Is the market underappreciating the strength of the JV with Taj Santacruz?

- Are there better risk-reward plays in hospitality today?

TajGVK feels like a solid, well-run, premium hospitality business that doesn’t scream for attention but keeps delivering. It’s not the fastest grower, but it has high-quality assets, strong profitability, and a clear expansion path. The Bengaluru hotel could be a big trigger over the next 12–18 months.

The stock has already run up quite a bit in past few months, so valuation isn’t a no-brainer anymore. But the fundamentals are strong, and if it keeps executing — this could turn out to be a quiet compounder over the next few years.

I’d really appreciate any thoughts, counterpoints, or insights — especially from folks with local knowledge of the properties or who’ve tracked the company for longer.

— Sujay Pawar