Systango Technologies Ltd

CMP: 280 rs

Market Cap: 410 cr.

ROCE: 33.9%

ROE: 27.4%

Debt: 0.09 cr.

Business Overview:

ISO 27001 & ISO 9001 certified digital engineering services company with 3 offices in the USA, UK, and India.

It provides software solutions that enable companies to design, implement and manage their own Customized Digital Platforms including Web2, Web3 and Mobile applications; with an emphasis on data and analytics

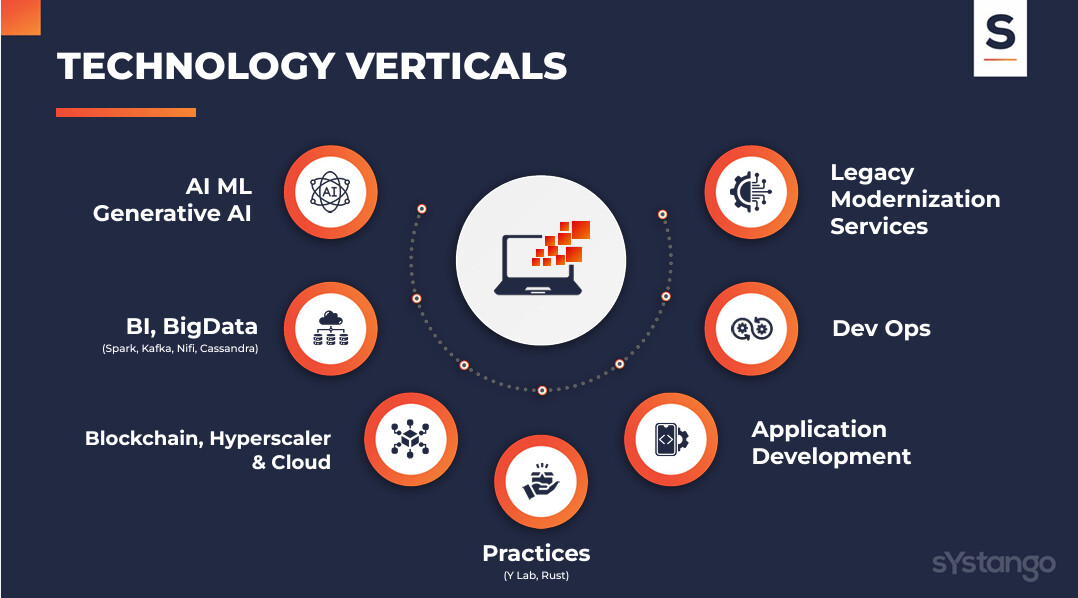

Business Verticals: [3]

a) Full Cycle Development:

Entire web and mobile app development lifecycle- from strategy, design, development, and quality to launch on iOS and Android.

b) Data Engineering, AI & Machine Learning:

Data aggregation, storage, organization, optimization, advanced analytics, and development of custom machine learning algorithms to support data analysis. Also, building recommendation systems, sentiment analysis models, natural language processing solutions, computer vision applications, and AI-driven automation.

c) Web3 and Blockchain Solutions:

Strategy assessment, rapid prototyping, solutions design, complex implementation

to third-party integration, add-ons, and entire ecosystem management. This, along with, specialization in Ethereum, Polygon Binance Smart Chain (BSC), Solana Tran and flow, etc. and building NFTs, DApp DeFi, Metaverse implementations DAOs, Exchange & Wallet integrations, etc.

d) DevOps:

Platform and cloud, Management, Continuous Integration and Delivery (CI/CD), and Continuous Testing and Monitoring. To introduce best practices for security, and deployments, and enable constant monitoring of production environments.

e) Product Architecture & Design:

Company has expertise in user interface,

user experience architecture and development.

f) Cloud Engineering:

Cloud engineering solutions encompass strategic planning, efficient use of managed services, and the transformation of applications and infrastructure

Services Offered:

a) Generative AI & ML:

Custom AI Models, AI/ML Consulting, Custom LLM Development, AI Automation Solutions, Contextual Chatbots

b) Cloud Engineering:

Cloud Consulting, CI/CD Pipeline, Cloud Migration, Cloud Cost Optimisation, DevOps

c) Blockchain:

Enterprise Blockchain Development, dApp

and Web3 Development, NFT Marketplace,

DEX /CEX Integration, DeFi

d) App Development:

Mobile Development, Web Development

e) Data Engineering:

Data Visualisation, Data Analytics, Data Ops, Data Pipeline, Data Lakes & Warehouses

f) Offerings:

Staff Augmentation, Legacy Modernisation, Dedicated Development Teams, Architecture Consultation, Application Modernisation

Solutions Offered:

a) Swotter AI Powered Wealth Management Platform:

Shootih helps small and medium-cap companies (like Systango) smoothen their financial management by enabling them to forecast their future expenses and goals.

b) Shootih Learning Management System:

Its a training platform designed for learner’s growth

User Industries:

Financial Services (FinTech), Hospitality, Fantasy Sports, PropertyTech, Transportation

& Logistics, etc.

International Presence:

USA, Canada, UK, Netherlands,

Switzerland, Qatar, South Africa,

Hong Kong, Australia, etc.

Revenue Breakup - FY23:

Software & Development Charges ~97%, Other Income ~3%

Geographical Revenue Split - FY23:

Overseas ~87%,

Domestic ~13%

Acquisition & Sale:

In FY23, company acquired a 100% stake in Isystango Ltd and formed it as its Wholly Owned Subsidiary Company. It also incorporated a Wholly Owned Subsidiary Company namely SYSTANGO INC, in the USA. Further, company sold its investment in Edsystango Technoeducation Private Limited, hence it is no longer a subsidiary of the company.

New Partnerships: [NGO_18122023185715_INTIMATION.pdf)

On December 18th, 2023, company

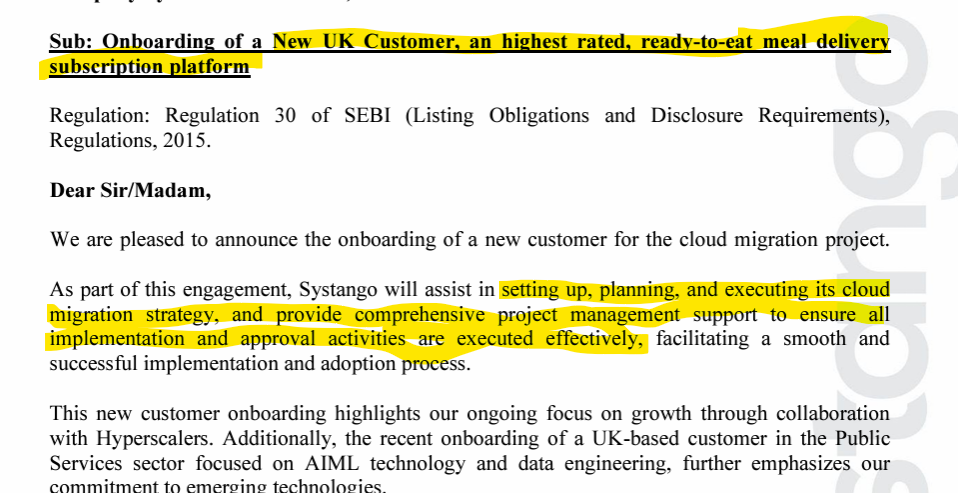

officially became an officially a Google Cloud Partner and AWS (Amazon Web Services) Select Tier Service Partner. It is already an Adobe Solution Partner (Bronze Badge)

Future Outlook:

a) Geography Expansion:

Company is planning to open a New Office and JV In Dubai for the Middle East and Africa, and invest and expand in North America, Europe & UK

b) New Competencies:

New Tech Partnerships (Adobe Bronze, GCP and AI, AWS) Invest and further core competencies in AI-ML, Cloud, and Web3 Rust Engineering Solution-Oriented Sales

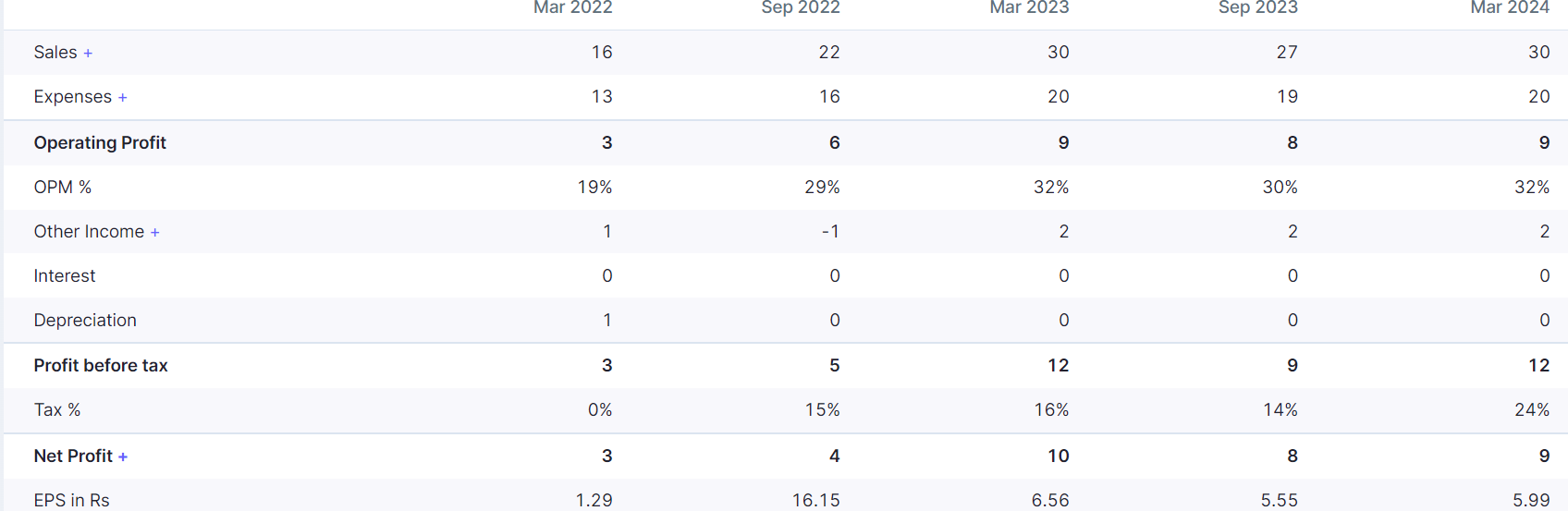

Financial:

Investment Rationale:

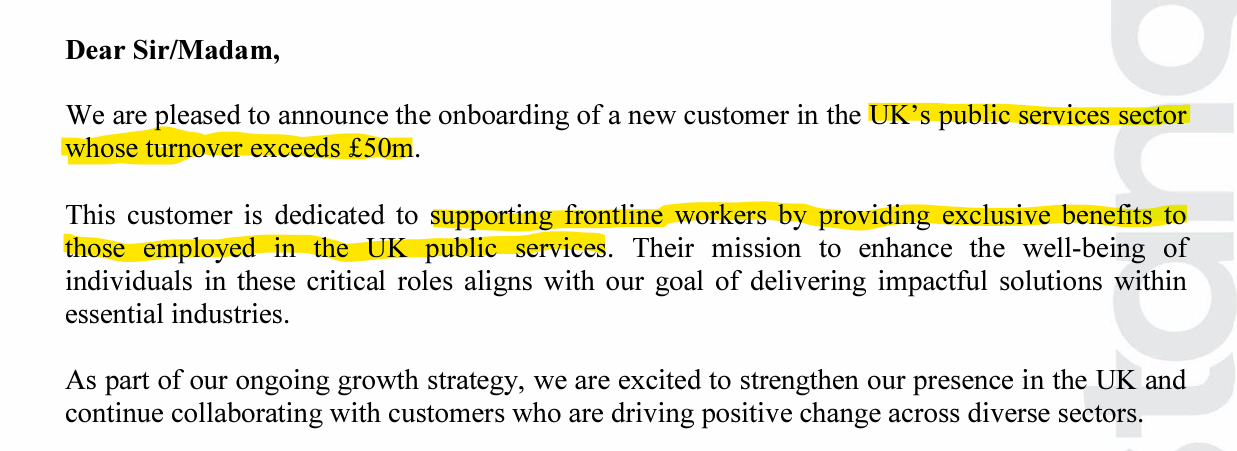

- 300+ employees globally, approved supplier for the UK government platform.

- Recently won awards for designs and recognized by Clutch for generative AI.

- Expertise in AI, ML, business intelligence, Big Data, web3 blockchain, and cloud.

- Recently started focusing on Rust programming language.

- Services include cloud migration, data engineering, machine learning, and blockchain solutions.

- Target to have 500 employees.

- Aiming for a 25 million revenue at the end 25 so three years from October 2023.

- Possibility of In organic expansion from IPO money.

- 52 cr cash.

Risk:

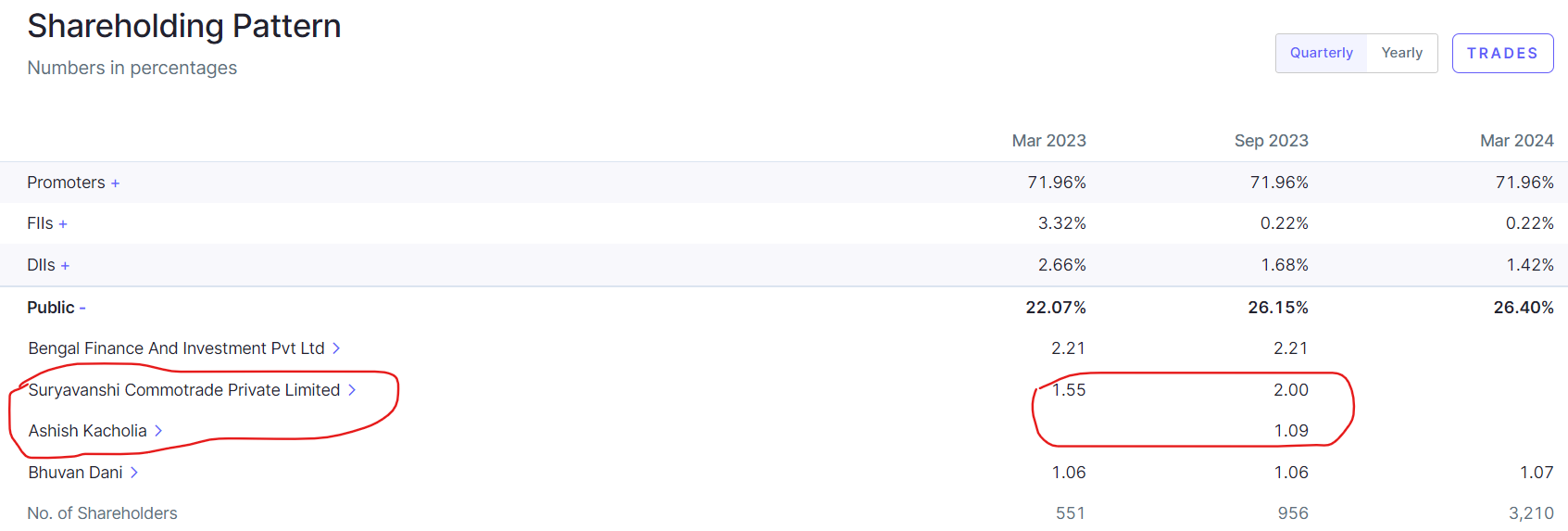

top 10 customer contributes to about 40 to 45% of our Revenue.

Revenue guidance of 65 cr for FY 2024 was not met. It was 57 cr.

Lack of revenue growth as guided by management,

Very small company which has low win rates.

Company not done conference call after H2 FY 2024 results, shows lack of communication to share holders.

Systango-Technologies-Limited-H1FY-23-24-Investors-Presentation.pdf (5.6 MB)

Transcript-of-the-H1FY-23-24-Earnings-Call.pdf (388.8 KB)

Disclosure: Invested