Hi

Can you pls mention which is the second approval they got

(U said two approvals in 2 days)

Thanks

Hi

Can you pls mention which is the second approval they got

(U said two approvals in 2 days)

Thanks

Hi Ganesh,

I have edited my post. The two approvals I was referring to were:

European Marketing Authorization has been mentioned here in this thread:

Link: Syngene International - #277 by Rushabh_Doshi

Amgen got approval for some drug and Syngene worked with them.

link.

Got it from this this tweet.

tweet

Investor presentation for Q1 results

Compared to other business models, in CRO (specifically in pharma) the critical asset is client IP (All the technical know how and the research work of many years ) What kind of black swan event we can anticipate ?

If any of this IP is stolen then the entire client relationship will go for a toss and then huge legal and other costs.

I am coming from the similar risk we have seen where the offshore call centers leaked customer credit card / bank details.

Please share your thoughts.

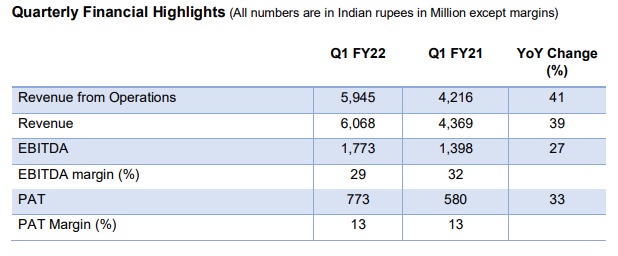

Syngene reports first quarter results

Revenue from operations up 41% to Rs. 5,945 Mn, YOY

PAT increased 33% to Rs. 773 Mn YOY

Topline Rev down by 10.5% Q-O-Q

PBT (Before Exceptional items) down by 39.7% mainly due to RM cost increase Q-O-Q

Did anyone attend the Syngene AGM today? Anything worth reporting from the event pls…

Some notes which i could note down from the Conf. call of yesterday : –(Apologies for the informal note taking & some points missed which i couldn’t note down properly, in advance )

Q1FY22 Syngene International-21st July’21

–Employee cost increased by 22% due to recruitment of additional staff in existing and new started facilities

current employee strength : 5500 ( last year same Qtr =5000)

–Mid teens growth guidance for this FY22 Year which is a bit conservative as in the Q1FY22 itself the topline growth has been 40% but we will take one Qtr at a time due to covid uncertainity

–1st Qtr is always lower for us than the 4th QtrFY21 due to seasonality in our business.

–Revenue per Employee future outlook --is broadly stable, absorbing price pressures ,in future when we have manufacturing also it will show an increase in Revenue per employee than now as in discovery phase which is not assembly line ecosystem we have maintained it as stable and when Mfring starts in a big way --this per employee figure should see an increase.

–ramp up of Mangalore facility mfring , we have 1 project which will take 24 months to complete and by that time the regulatory inspection will take place and once that is cleared we will have new clients getting attracted to a running facility which is Regulatory approved.

–Biologics capex --$50 Mn spent , we continue to invest & adding 2k Ltr capacity over there so another 15/20 % in the year --as part of Capex guidance. This is Biologics mfring.

–Remedisiver contribution – Mid teens contribution of it.

–New Product which partner client co. Albireo – Its a rare diseases , revenue wise its a small opportunity as the prevalence of the diseases is not big , we are API suppliers of this .

–Biologics Mfring contribution --we are seeing good progress in 4 areas (1) Discovery area (2) development similar trend (3) Biologics --global demand due to pandemic

–for Mangalore plant --the next 2 yrs we have a project wherein we are taking a product and developing it so that it triggers a FDA / Europe EMA inspection post which other clients can be show-cased the capability.

–Cellular Gene Therapy —we are doing discovery services with some clients. In general, in drug discovery and drug delivery clients asks us to have some working knowledge of new areas which comes handy ( couldnt note the complete point )

Along with Cellular Gene therapy there is little discussion on the capability and preparedness of crispr cas9 genome editing. Basically, management said that they are ready for any such opportunity but indicated that the technology is at an early stage. More will check when we have the transcript available.

Jonathan Hunt gave very mature answer on Crisper cas9.

Among all the gung ho on crisper this was the most appropriate answer.

Article

Biocon did out of court settlement with Celgen for Revilimid. Celgene is subsidiary of BMS, Syngene recently announced 10 year long term contact with . This Generic business of parent who is always in court to fight patent of innovators and CRO business of Syngene who is in agreement to protect, respect patents, know how of innovators are not conflict of interest ? Any impact on business in long term ? Please give your views.

Excellent article on the whole Indian CRO landscape and Syngene. Hope it adds value to everyone!

Thanks for sharing the article - Although focuses on only CRO , indeed thought provoking - Given lot of paralles drawn between CRAMS as future IT industry of India - it wasn’t clear as to why China is way ahead in CRAMS/CRO compared to India.

A clue lies in below from article.

One of the things that differentiated China from India when research outsourcing took off between 2001 and 2010 was China’s access to government-provided capital, Subramanian says. Without it, Indian companies were unable to scale in the same way. “The science was always there. The talent was always there. What was lacking was financial capital,” he says. “Once you start getting professional investors, I think the doors will open wide for India.”

Carlyle group, being one of largest PE fund in pharma/biotech space- bought stake in Piramal and Sequent etc is a testimony of financial muscles coming in, many more such investment in last few years and coming years as well, more importantly the global landscape and network these investors bring in expedites the scaling curve.

Article hasn’t called out Suven pharma, a good success story of small biotech outsourcing/partnership success model at decent scale. Not to mention Novel molecules investment by Suven life, Biocon - Biacara and many more.

Core CRO space is more sensitive to IP, financial investment for innovation infra, global presence closer to innovators but overall end to end CRAMS space equation works well in coming decade for India. It will be very interesting to see what likes of R&D and proven IP CSM oriented organization such as PI industries do in space( acquired pharma assets).

One disagreement with article is Western leadership in organizations as a must - IT industry has thrived so well without so high dependency on western leadership( it’s part of solution but not solution itself)- both are Knowledge industries- getting Knowledge and continuous Innovation related investments is key IMO.

Although Article fo focused only on CRO, a lot is happening in Broader CRAMS space, those who wants global scale and ambitions- playback will be very different than rest of pack.

Excited about possibilities in this space, not QoQ or YoY game, it’s DoD, 21-30 decade is likely to be inflection point for industry, And emerging Tech( AI etc) will be a key enabler - again something that India is not behind in curve.

Nice Summary @Dev_S

I have slightly different opinion on western leadership. We cannot compare IT outsourcing with Pharma sector. Former doesn’t need any regulatory approvals, Entire IT sector is based on body shopping (only very recently few indian companies are going into the direction of product innovation like Inteellect Design, Post Man , LTTS, Tata Elexsi , KPIT etc… ) where as pharma is purely knowledge industry where we always talk about PHD holders and scientist. The author is trying to highlight the ease of doing business by having western leaders in the organisation which is going to bring the essential depth in terms of having network connections with various innovator companies and regulators.

I see one major risk which is highlighted by Mr Hunt , India’s cost advantage is fading, indeed it is fading. Look at the IT attrition rate and even in few pharma companies it is in higher teens.

But when it comes to pharma it is not easy to find a scientist like IT resource , so India future will depend on bit of cost advantage on labor costs + plus strong chemistry skills , IMHO these are the driving factors . The same message is echoed across the industry now a days. KPIT says I don’t want to do me too business. Mastek ( listen to B&k latest interaction ) said we don’t compete for work based on the low cost bidding (biggies like TCS, INFY and WIPRO) we are niche and we don’t compromise on pricing.

Bit old but good read about India’s CRO industry.