TLDR version:

- Niche clientele: Caters to the domestic & overseas requirements for wind turbine castings for global top 10 OEMs (ex China) like Vestas, GE, Siemens Gamesa and Senvion. Other two leading OEM’s operating in India Nordex & Envision are also in the process of on boarding.

- Recent Rights issue to increase foundry capacity from 30,000 TPA to 45,000 TPA.

[ Old presentations coneys management aspiration to take the foundry capacity to 100,000 in phased manner over next few years.] - Further, in-housing machining capability addition and Renewable power installation will be margin accretive (PBDIT expansion 3%+)

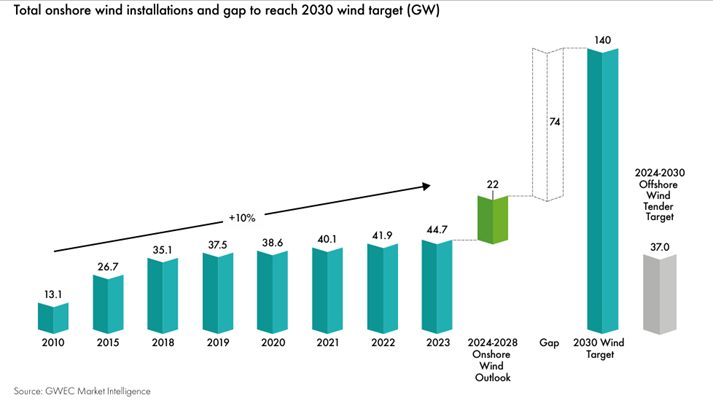

- Strong tailwind for the industry: India wind power installation to go up from 45 GW to 140 GW by 2030.Likewise, global installation to increase from 117 GW in 2023 to at 320 GW of annual installations by 2030.

Global Market Outlook:

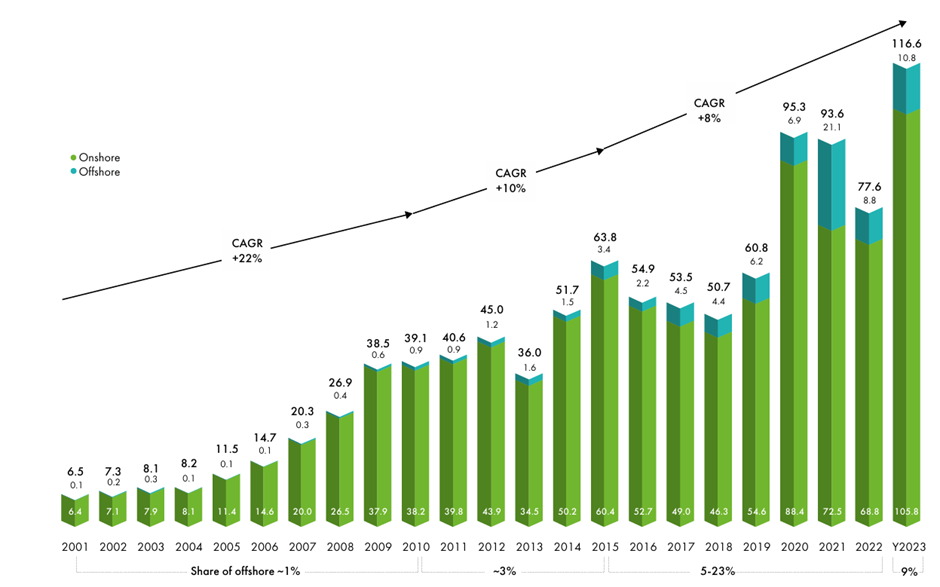

- During the year 2023 global wind installations have gone up by 50% from 78 GW to 117 GW.

- Wind industry is in a pivotal moment with COP28 adoption of a target to triple renewable energy by 2030 and to accelerate the energy transition. Industry needs to accelerate wind energy installations from 117 GW in 2023 to at 320 GW of annual installations by 2030.

- So far, industry growth is powered by key markets like China, the EU, the US, India and Brazil. Other major economies also set up ambitious targets – particularly those with strong offshore resources – such as Japan, South Korea, Australia, Vietnam, the Philippines and Kenya.

Strong renewable Push for domestic market:

-

India ranks fourth in total wind installations, with 46 GW of installed onshore wind as of March 2024. It is the second largest wind market in the Asia Pacific region after China.

-

As per the National Electricity Plan of the central government for the period ending 2032, India’s installed wind capacity is estimated to amount to around 73 GW in 2026-27 and 122 GW in 2031-32.

-

With various policy initiatives from government and institutions, India’s installations have also gone up by 62.5% from 2 GW to 3.25 GW and highest during last 6 years.

-

10 GW annual wind tender per year till 2027 (as per Suzlon presentation)

Synergy Green:

- Caters to the domestic & overseas requirements for wind turbine castings and established long term supply contracts with globally leading OEMs like Vestas, GE, Siemens Gamesa and Senvion.

- Other two leading OEM’s operating in India like Nordex & Envision are also in the process of on boarding. All these OEMs demand includes domestic installations, Turbine assembly export and direct castings export.

- Apart from wind OEMs, company established long-term contracts with leading wind gear box manufacturers like Flender Drives & ZF Wind.

- Company also caters to the non-wind customers like Terex in mining and Milacron for plastic injection castings.

Govt Policy Support:

The step-up in wind demand will accelerate onshore wind growth, with following policy initiatives

- 10 GW of annual onshore wind bids targeted from 2023-2027 through single stage/e-reverse auction bidding;

- Inter-State Transmission System (ISTS) charges waiver up to June 2025

- Wind specific renewable purchase obligations (RPOs) from 2023 to 2030

- Announced firm and dispatchable renewable power supply tenders, as an upgraded version of the round-the-clock tender for renewable and storage projects

- Mandated minimum share of renewable energy consumption for the electricity distribution licensees (DISCOMs) and the ability for consumers to purchase green electricity

- Improvements in the timely disbursal of payments by DISCOMs

- Transmission planning to integrate 48 GW onshore wind capacity by 2030

- A revised ‘National Repowering & Life Extension Policy for Wind Power Projects - 2023’ to facilitate repowering of wind turbines.

The Government of India has approved a viability gap funding (VGF) scheme worth Rs 7,453 crore ($890 million) to promote offshore wind energy projects.

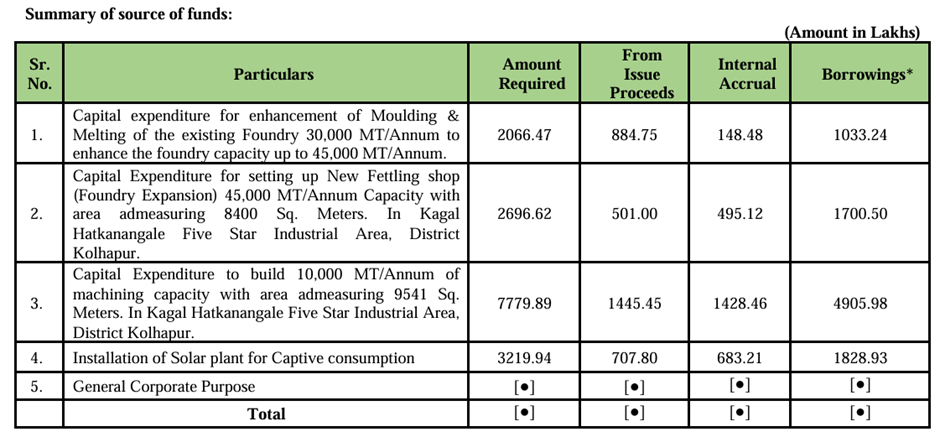

Recent Rights Issue and Capex:

- Present 30,000 TPA foundry capacity is getting peaked with 80% utilization during FY 2023-24 Considering improvement in demand forecasts, it is being planned to complete the brownfield expansion from 30,000 TPA to 45,000 TPA.

[ Old presentations coneys management aspiration to take the foundry capacity to 100,000 in phased manner over next few years.] - It is being initiated to establish 10,000 MT of In-House machining facility to meet increased production capacity. Presently entire machining activity is outsourced and 75% of our supplies are in machined condition. Present spend on machining is 10.4% of our revenues. During last few years business growth is happening with West/North based OEMs like Senvion, GE, Adani & Envision. We are also expanding the foundry capacity and need for machining the larger size turbine up to 5 MW is increasing.

- A Presently we are connected with 8 MW of electricity. We are in the process of enhancing up to 12 MW for meeting the foundry expansion requirement. part of our carbon neutral goal, renewable capacity is being enhanced from 2 MW to 10 MW.

All these initiatives will enable us to achieve revenue growth and margin expansion for the upcoming years. These investments in machining are projected to contribute margin expansion to PBDIT up to 3%

Competition:

- SE Forge Coimbatore: This is a captive foundry of Suzlon Wind OEM demonstrated capacity is 122,000 TPA. Since this company is located in SEZ location, domestic customers need to pay customs duty for using their production with in India. This gives us the competitive edge and becomes preferred supplier. CU of 22%. Suzlone share in business for SE forge 40%

- Baettr India Chennai: This Company became operational in 2022 with a capacity of 30,000 TPA. Their major customer is Vestas. They also have foundries in Europe & China taking significant global demand of Vestas.

- Chinese Imports: This is the biggest competition with ample capacity. Their prices are estimated to be around 20 to 25% cheaper supported by lower commodity prices, power tariff, other input costs and incentives. However this gap is bridged with logistic costs and basic customs duty on imports.

Outlook:

- For F.Y. 2024-25 executable order book is projected to be around Rs 400 Crores and estimated a revenue growth of over 20%.

- Export revenue share is estimated to grow from 11.5% to 25%. Assuming reasonably stable raw material and revenue growth, PBDIT margins are estimated to expand by 150 to 200 bps from the present levels of 12.5%

- Gearing up as an export hub As the second-largest hub for onshore wind turbine assembly and key component production in the Asia Pacific, India is strategically well-placed for wind manufacturing expansion. It can benefit from a “China + 1” approach adopted by many major supply chain actors.

- Domestic manufacturing is sufficient to meet India’s own onshore wind demand through 2030, leaving additional export and trade value ahead if India can significantly scale up manufacturing capacity. India can make additional efforts to reduce imports of a few large components such as castings, generators and pultrusion carbon f ibre. For example, in January 2024 at the Vibrant Gujarat Summit, Reliance announced that it would set up India’s first carbon fibre facility at Hazira, Gujarat, for use in blade manufacturing in the wind sector. Additionally, the successful award of offshore wind tenders is likely to attract investments in domestic offshore wind manufacturing. The attractiveness of financial and non-financial incentives offered by the central and state governments will be a determining factor in this regard.

Disc: in early stage of research. No Investment as on date.