First thanks all members to provide their view on thread. Certain members seek my opinion on some aspect. I try to address those point to the best of my understanding and ability

@babu44b

As per my understanding, the company has agreement with M&M. The RM change is passed on every quarter. So while there might be quarterly change in contribution margin, over a year or so, things get streamlined. I do not know how does price of end engine happen? It is based on ROCE or provide fixed margin on cost of production? Nearly 95% of sales of the company is to M&M (Swaraj Tractor division).

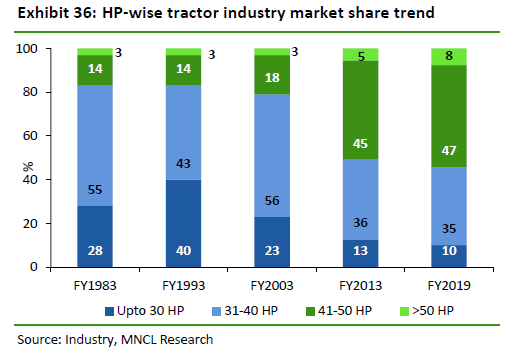

However, over a period, average HP Tractor sold has increased consistently over decade for the industry. Same shall also be applicable to Swaraj Tractor and Swaraj Engine. Hence, despite increased in average HP of tractor increased, we do not find corresponding major increase in realisation. Average realisation as per my calculation has increased at CAGR of 1.6% from Rs 73224 per engine in FY2010 to Rs 87100 per engine in FY2021. This is despite increase in average HP from 38.9 HP (my calculation from Monarch enclosed graph for everyone reference) in FY2013 to 40.3 HP in FY2019. So broadly, 1.5 HP increase in average HP capacity over 6 years can explain 1.6% increae in CAGR. Hence, the gain in profit has mainly came from only operating leverage (higher scale ) in my opinion. I would assume same to continue to future.

During FY21, average contribution per engine sold increased from Rs 85600 per engine in FY19 to Rs 87,100 in FY20 as per my calculation.

Last year lower dividend was more to conserve resource for Covid related uncertainity then normal practice of the company. We also need to understand benefit of DDT not being paid by company from last year, passed on the investor now in my view.

On EV, management has not publicly disclosed any plan. Further, with Kirloskar group also being large investor, I suspect Swaraj Engine would be prefered company for M&M group for EV related investment. This is my

@Rohit_Kadam

Till Sep 2020, M&M was buying in cash which has increase now to 30 days in my understanding, if I back calculate figures. Hence, working capital increase and I expect same to be new normal now.

@ORION

While there is no public announcement of capacity, in past, the company has increased capacity by greenfield expansion at very negligible capex and 12-15 months period. I see same can be expected to cotninue.

Due to Kirloskar group being also large stakeholder (which also interest in Engine business) and supply just being able to meet M&M demand for engine, I doubt that company would add new client in near future. They contnue to supply some component to SML Isuzu although, but that is very nominal (1-2% of sales) if my memory is correct.