SVP Global Ventures Ltd. (“SVP”) is a diversified yarn manufacturing company, incorporated in 1982, and is listed on the Bombay Stock Exchange. SVP is a professionally managed company, led by a dynamic promoter Mr. Chirag Pittie, who has BSBA degree in Finance and Management from Boston University, USA.The Company has 3 units at Coimbatore, Palani, Madurai in Tamil Nadu for manufacturing Polyester & Cotton Blended Yarn with the Spindle Capacity of 98,000.

Growth Trigger: Recently the company has setup textile manufacturing facilities in the state of Rajasthan, at the RIICO Industrial Area in Dhanodi, District of Jhalawar. These new units will produce high quality compact yarn which are Low on hairiness, higher strength and elongation, less fiber fly, significant advantages.

• Phase 1 Expansion: The Company has recently commissioned the new manufacturing capacity of 100,000 spindles. The project cost for the same was ~450cr which was funded through long term loan of 275cr and rest was funded through equity. The project will get 11% interest subsidy (6% State+3% Special +2% TUF) from the government as a result of which interest cost is negligible for the project (~1-2%)

• Phase 2 Expansion: The company is about to commission the new manufacturing capacity of 2400 rotors.The project cost for the same is ~90cr which was funded through long term loan of 55cr and rest was funded through equity. The project will get 9% interest subsidy (6% State+3% Special) from the government

• Phase 3 Expansion: This phase of the expansion will further increase the spindle capacity by 50,000 and is expected to be completed by the end of 1QFY18. The project cost for the same is ~225cr which was funded through long term loan of 160cr and rest was funded through equity. The project will get 9% interest subsidy (6% State+3% Special) from the government.

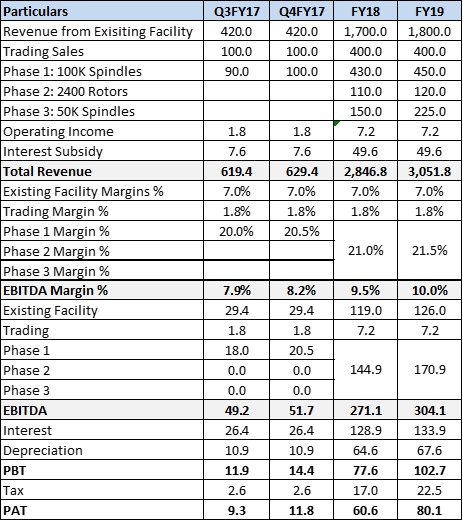

Financial Projections:

The company is optimistic about the demand for the product and confident of selling increased capacity in the market. They have already registered 90% utilisation from the phase 1 of the expansion, which can be seen in the Q3FY17 results of the company. The company expect new projects to add ~800cr annual revenue with the EBITDA margins of 18-20%. Further, as company would be getting interest subsidy from the government, project is expected to boost the profitability of the company. Given below are the rough financial projections for the company:

Note: Amount in the above table is in Cr.

Valuation: The stock is trading at ~4x FY19E Earnings and ~4.5x FY19E EV/EBITDA.

Key Risk: High Leverage, delay in completion of expansion, low capacity utilization etc

.

Views are invited for the discussion.

Disclosure: Invested since lower levels