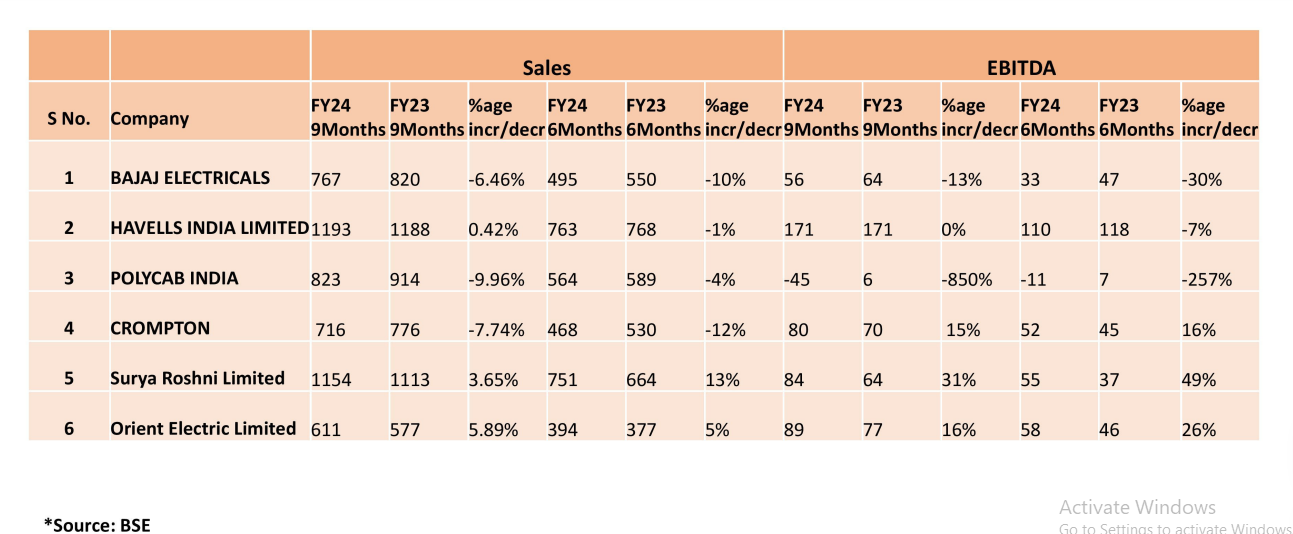

Surya Roshni -

Q4 and FY 25 results and concall highlights -

Q4 outcomes -

Revenues - 2146 vs 2080 cr, up 3 pc

EBITDA - 211 vs 173 cr, up 22 pc ( margins @ 9.85 vs 8.35 pc )

PAT - 130 vs 104 cr, up 25 pc

In steel pipes division, EBITDA / ton improved by 14 pc YoY

Revenues in lighting and consumer durables segment improved by 10 pc. Absolute EBITDA in this segment rose by 6 pc. This division continued to maintain strong double digit margins @ 10.3 pc

FY 25 outcomes -

Revenues - 7436 vs 7809 cr, down 5 pc

EBITDA - 609 vs 586 cr, up 4 pc

PAT - 347 vs 329 cr, up 5 pc

Full year revenue decline is because of decline in HR steel prices

Segmental performance for full FY -

Lighting and consumer durables -

Revenues - 1690 vs 1572 cr, up 8 pc

EBITDA - 162 vs 150 cr ( margins @ 9.61 vs 9.57 pc )

PBT - 125 vs 120 cr

Revenues in this segment increased despite continued price erosions in the lighting segment

Professional lighting grew in strong double digits, Street lighting revenues surged by 2.5X

Consumer lighting witnessed healthy volume growth. Price erosion continued

Company is going to enter house wiring segment in near future. Aim to clock 100 cr of revenues in first yr of operations

Steel Pipes and Strips -

Revenues - 5749 vs 6242 cr, down 8pc ( due fall in HR steel prices ). Volume growth @ 9 pc

EBITDA - 446 vs 436 cr

EBITDA / MT @ Rs 5392 vs Rs 5401

PBT - 341 vs 325 cr

In Q4, EBITDA/MT surged to Rs 6708 vs Rs 5877 cr YoY

Share of VAP in this division now stands @ 43 pc

Company’s Steel pipe facilities are located at - Anjar ( Gujarat ), Hindupur ( AP ), Bahadurgarh ( Haryana )

Their lighting manufacturing plants are located at - Gwalior ( MP ), Kashipur ( Uttarakhand )

Company is now debt free

Cash on books @ 342 cr

Company is No 1 ERW pipe manufacturer in India, No 1 exporter of ERW pipes from India

Expect to ramp up the sales of their wires segment to 500 cr in next 3 yrs

Increased share of VAP in steel pipes division is helping the company expand their overall EBITDA / MT

Capex planned for next 3 yrs @ 500 cr

Hoping to clock EBITDA / MT @ Rs 5800-6000 for FY 26

Volumes and EBITDA / MT wise breakdown of Steel pipes division -

GI Pipes - Rs 6465 @ 26 pc of sales by volume

API and Spiral pipes - Rs 9300 @ 17 pc of sales by volume

Black pipes - Rs 4488 @ 30 pc of sales by volume

Section pipes - Rs 1872 @ 15 pc of sales by volume

CR strips - Rs 1156 @ 12 pc of sales by volume

Guiding for a volume of 11 lakh MT for FY 26 ( they sold 8.8 lakh MT in FY 25 ). As volumes ramp up, EBITDA / MT should start to ramp up. Aiming to expand their capacity to 19 lakh MT in next 3 yrs

Out of this capex of 500 cr that the company has lined up, 400 cr shall be spent towards value added products. Eventually, they aim to derive 60 pc of their revenues from VAP segment vs 45 pc currently

Company exports to 50 + countries across the globe including - US, ME, Australia, Mexico, Africa, EU

Anti dumping duty on company’s exports to US have reduced from 19 pc to 2.5 pc ( recently ). US being a big mkt should help them achieve their aggressive volume guidance of 11 lakh MT for FY 26

Capex for FY 26 should be around 150 cr

Company’s FMEG distribution reach should help them achieve their targets that they have set for their Wires segment

Company expects the lighting industry to stabilise ( wrt price erosion ) in near future. Aim to grow the Lighting and CD division by 10 pc in FY 26 with a 20 pc kind of EBITDA growth

Already seeing good pickup in volumes in their steel pipes division in Q1

Exceptionally high EBITDA / MT in Q4 is due to inventory gains to the tune of 30 cr

Should be able to do an EBITDA of aprox 800 cr ( including both divisions ) for FY 26 vs FY 25’s EBITDA of 609 cr !!!

The wires manufacturing will be done by company in-house. They are not planning to outsource any manufacturing

A demerger of company’s two business segments is under active consideration. Should materialise in not so distant future. Should unlock a lot of value of its shareholders

Gross margins in Steel pipes divion @ 21 pc, Lighting and CD division @ 38 pc

Once the company’s capacity increases from 12 to 19 lakh Mts in steel pipes division, additional revenue potential should be around 3500-4000 cr

Disc: holding, biased, not SEBI registered, not a buy / sell recommendation