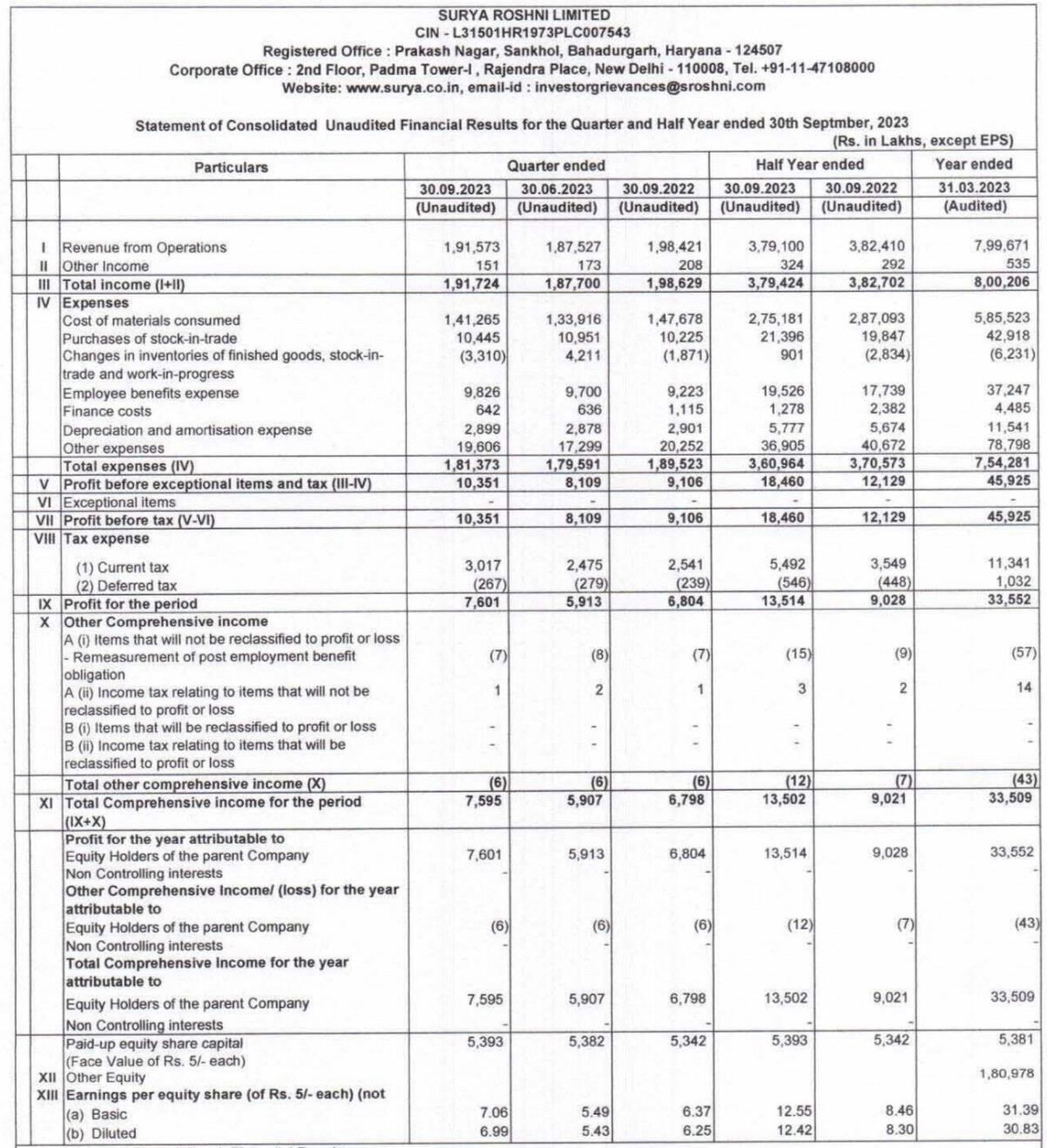

Surya Roshni Business Summary Q4FY23:

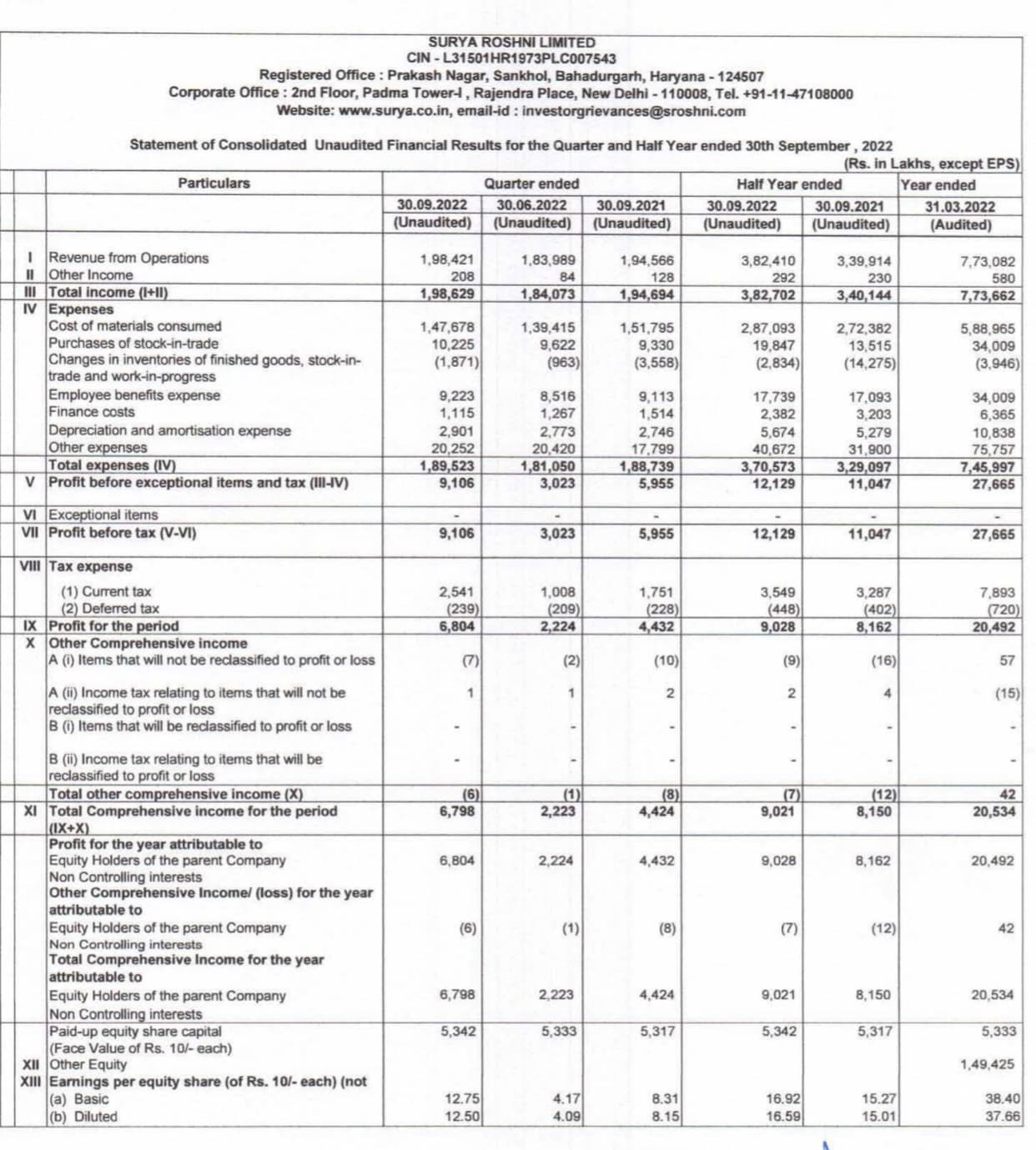

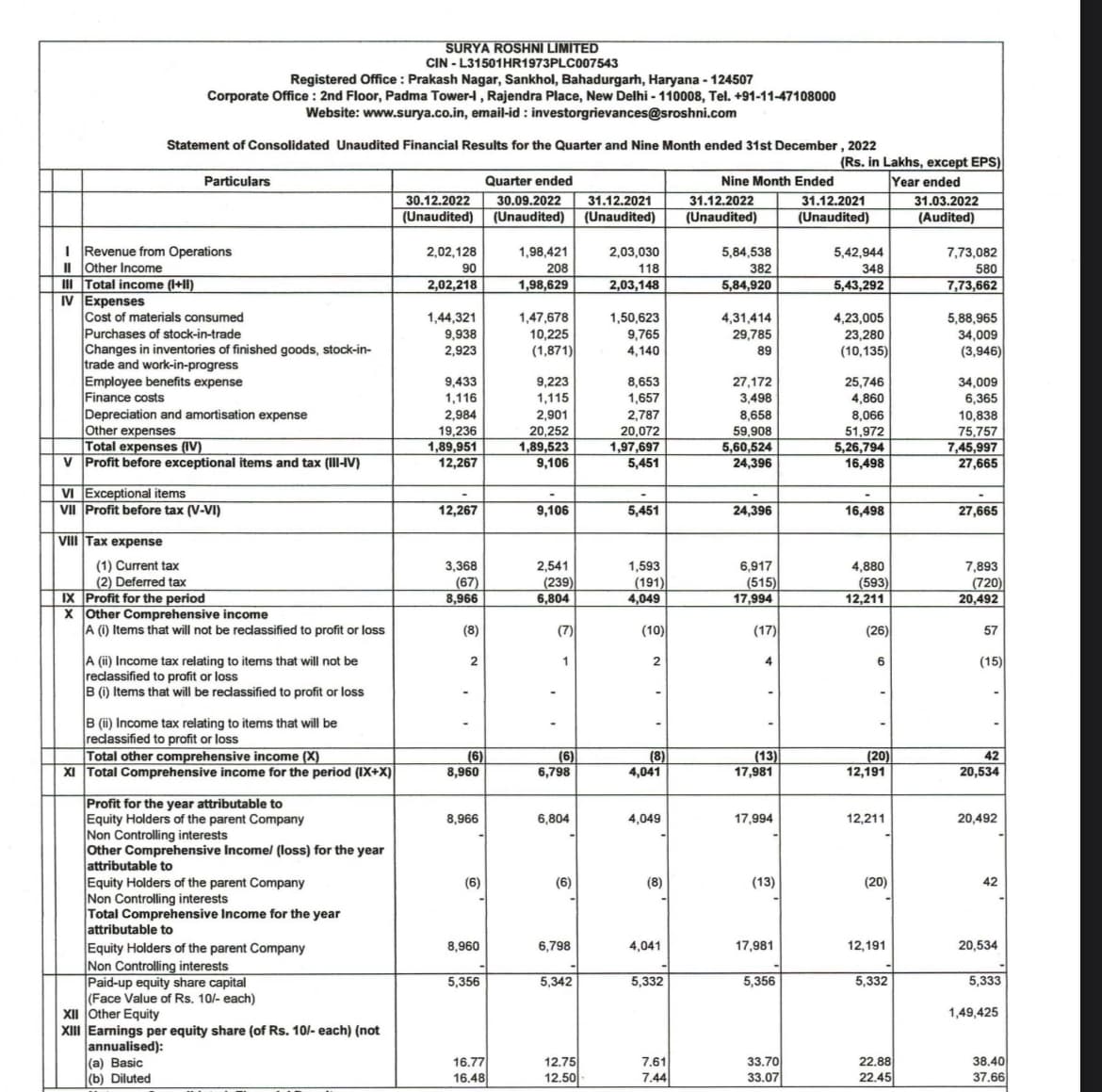

Surya Roshni Limited reported a record top-line and profitability for FY23, with revenue reaching nearly INR 8,000 crores. The company has focused on innovation, efficiency, technology, talent, and infrastructure to stay ahead of the curve. It has maintained a lean and healthy balance sheet and aims for sustainable growth with a comfortable working capital cycle. The company has repaid all long-term borrowings and plans to become debt-free within the next one-and-a-half to two years.

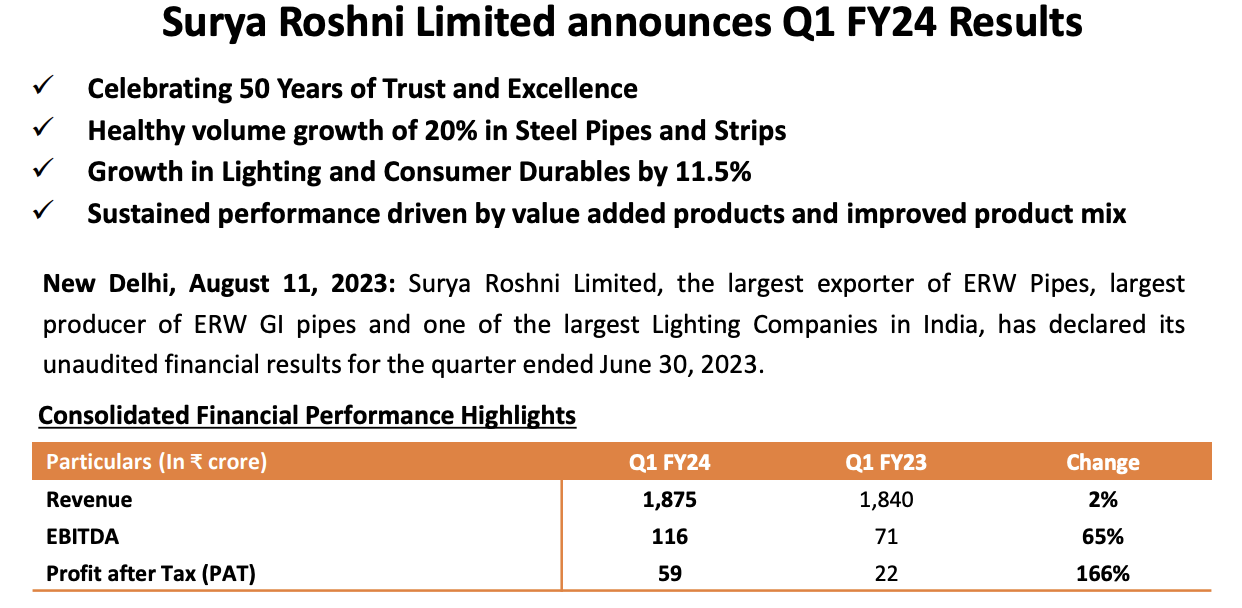

In the lighting and consumer durable segment, there has been revenue growth of 7% in Q4 and 16% year-on-year. LED lighting and professional lighting have shown healthy growth rates, with professional lighting expected to benefit from improvements in the capex cycle. The company is investing in visibility enhancement, advertisement, and strengthening its distribution network to support the growth of consumer durables.

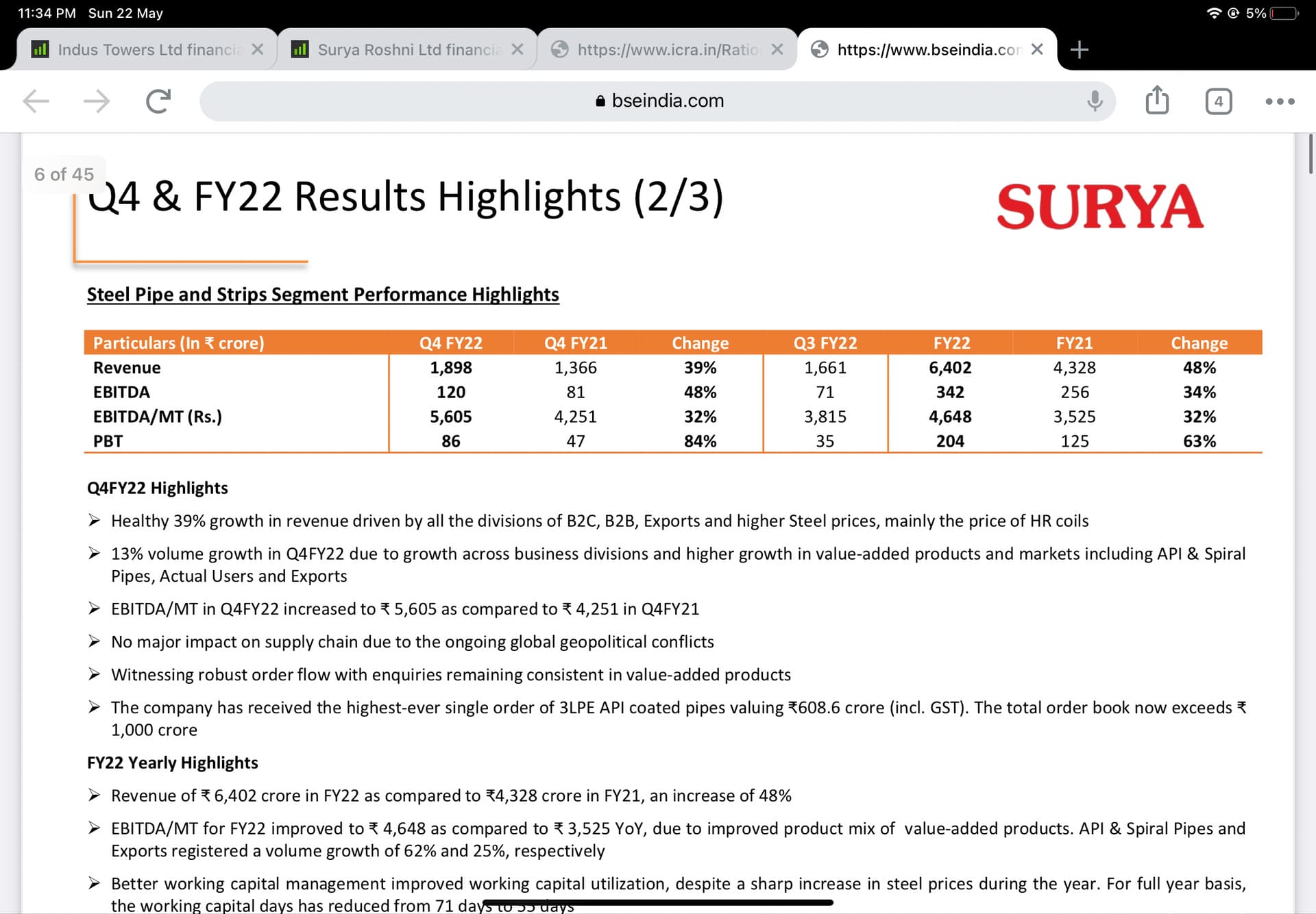

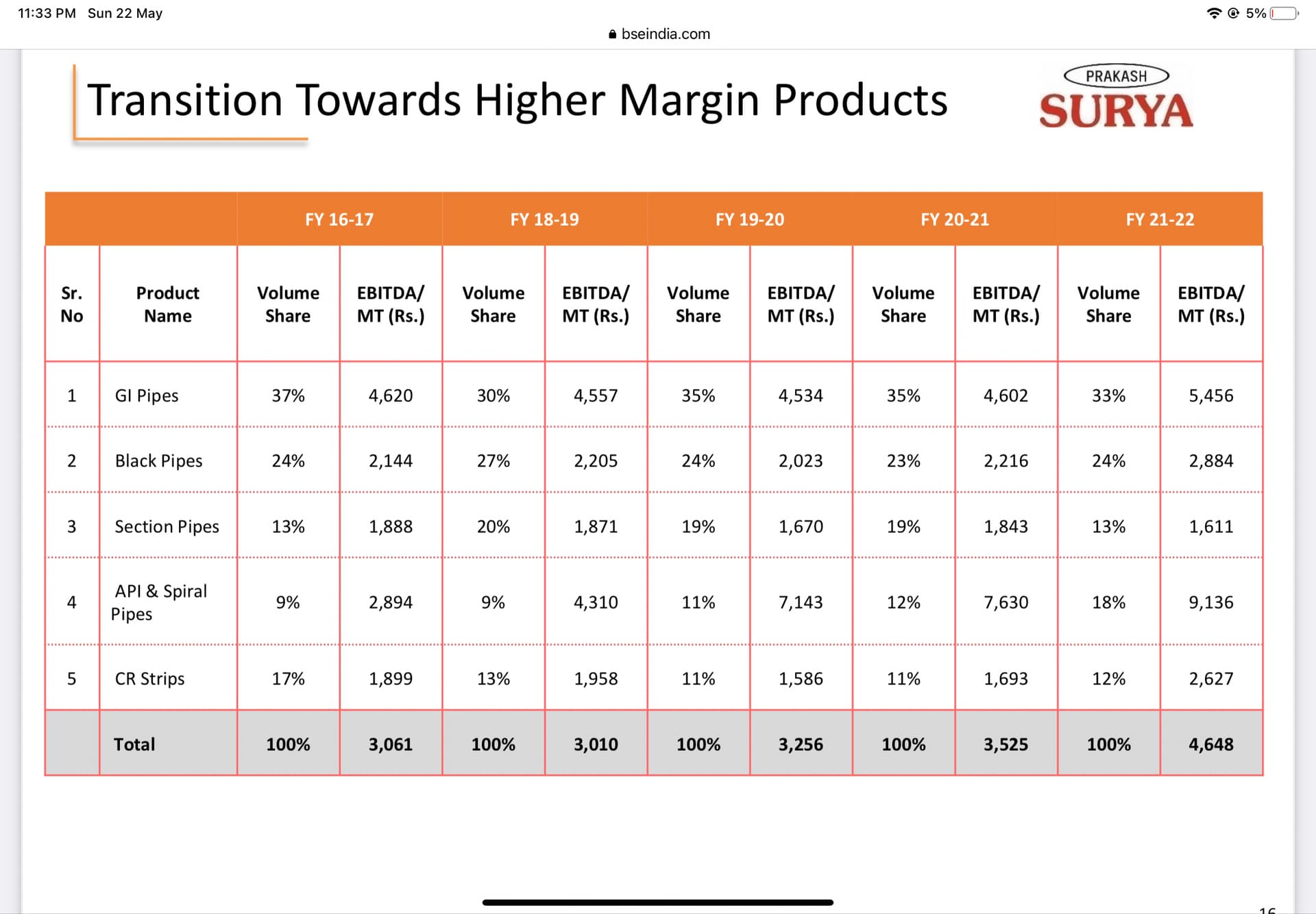

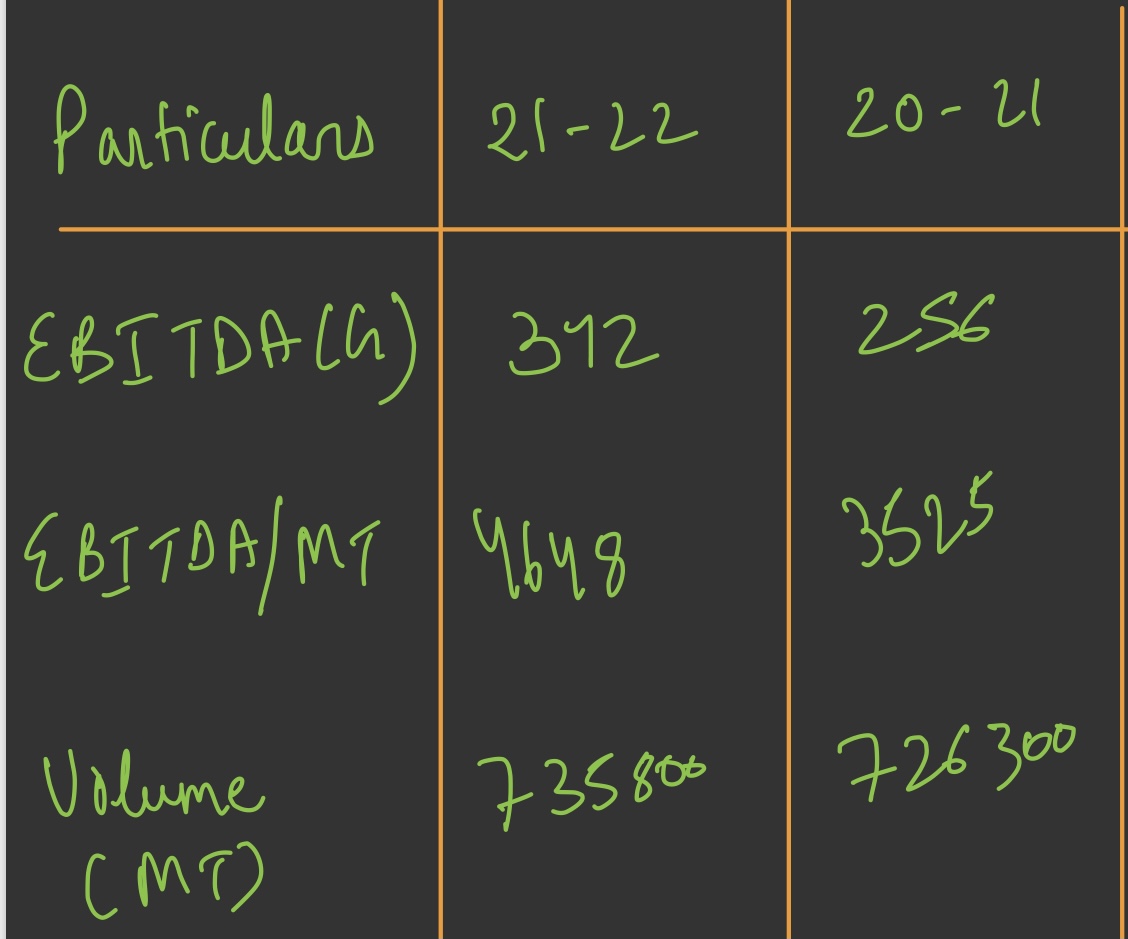

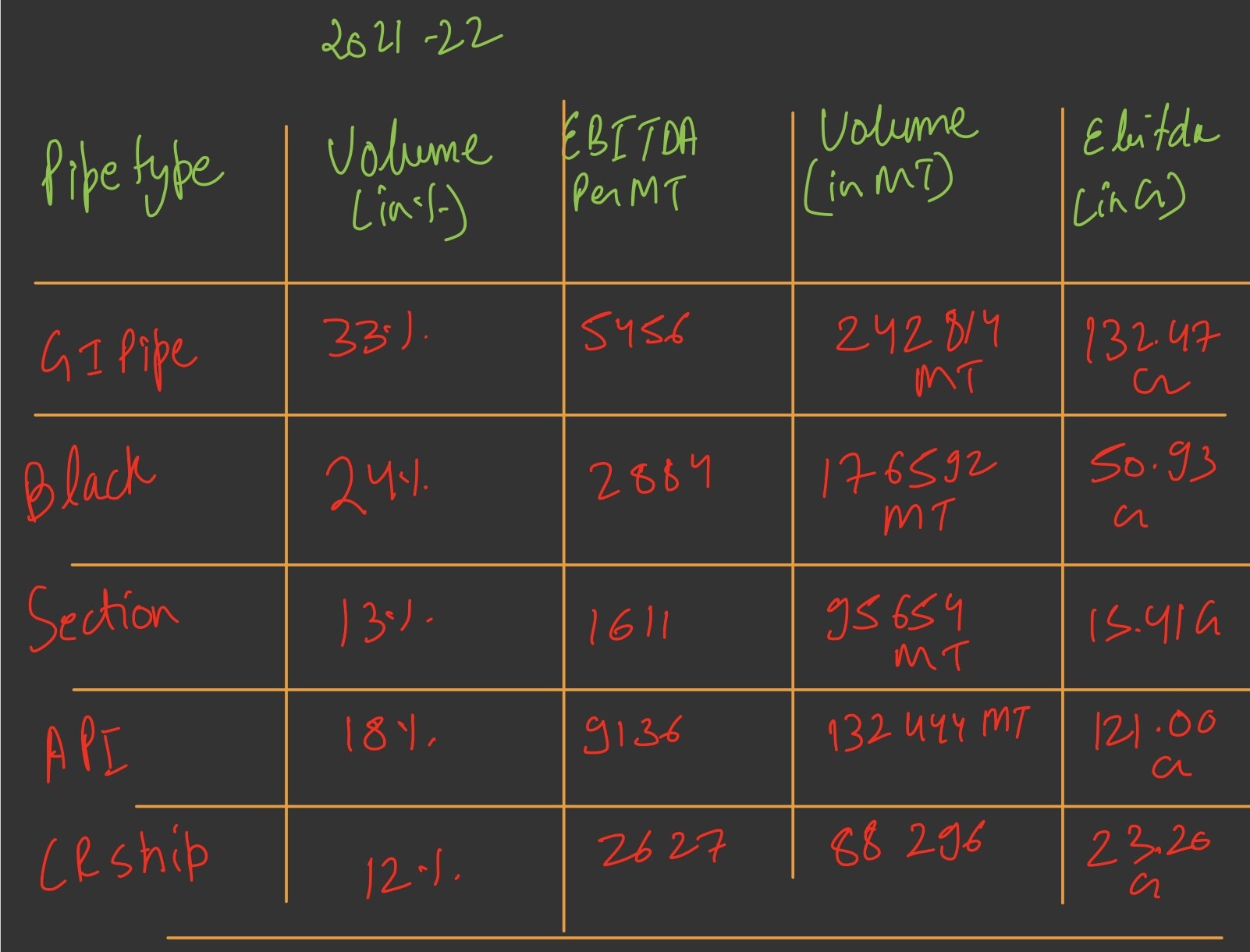

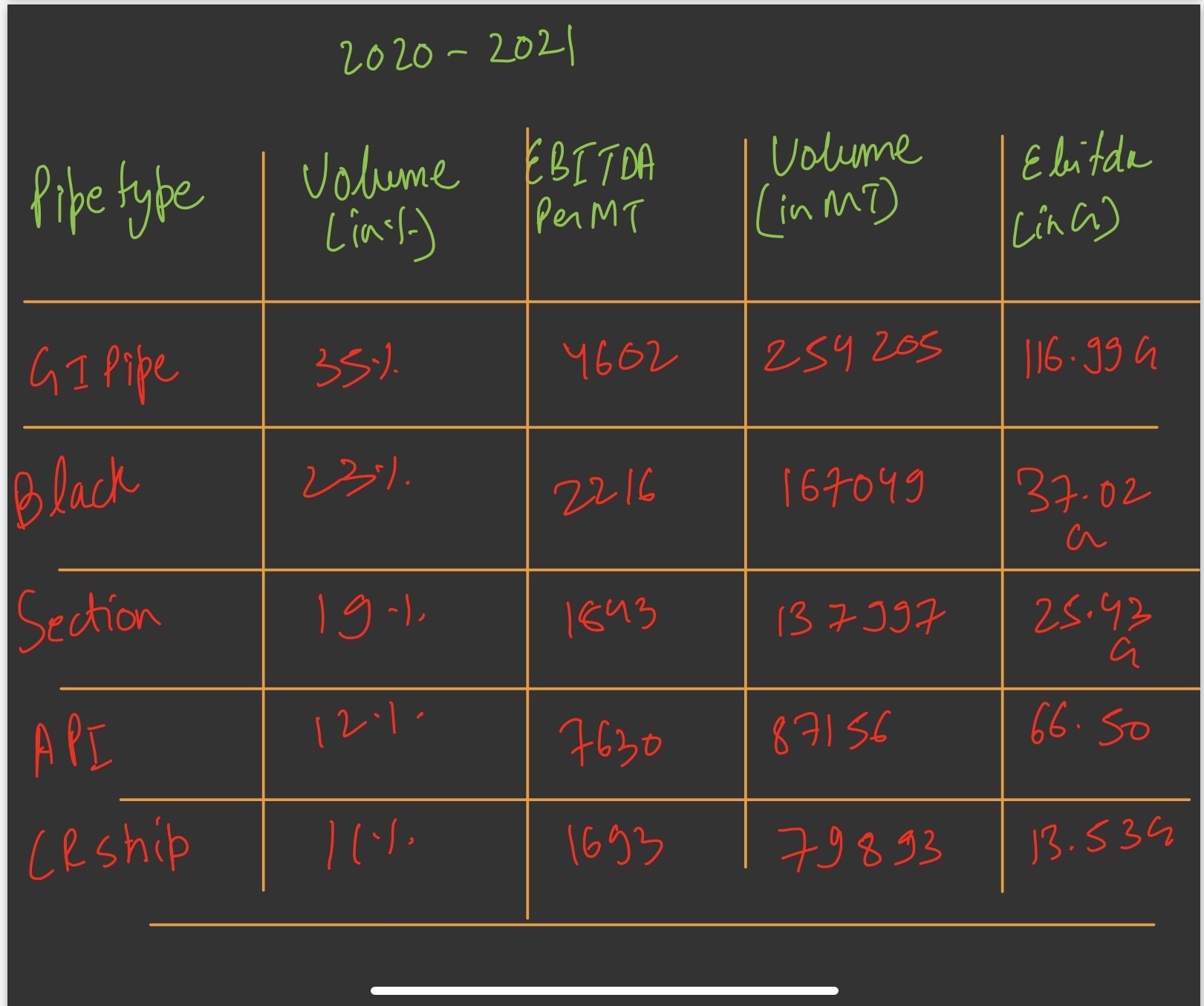

In the steel pipe and strip segment, the company faced a decline in global steel prices during the quarter but achieved its highest-ever realization per ton. It exceeded its EBITDA guidance and reported robust growth in profitability. The company has reduced debt, improved its debt-equity ratio, and maintained a positive cash conversion cycle.

The company remains confident about future opportunities and continues to focus on geographical expansion, innovation, efficiency enhancement, infrastructure, and capital to provide the best solutions to customers.

Tailwinds/Positives:

- Record top-line and profitability in FY23.

- Investments in innovation, efficiency, technology, talent, and infrastructure.

- Growth in LED lighting and professional lighting segments.

- Improvement in the capex cycle.

- Visibility enhancement, advertising, and strengthening of distribution network.

- Debt reduction and improved debt-equity ratio.

Headwinds:

- Decline in global steel prices.

- Competition in the lighting and consumer durable market.

- Market pressures on prices and margins in the steel pipe and strip segment.

When asked on the potential demerger- The CEO mentioned that it is the golden jubilee year for Surya Roshni and that the company has aspirations for growth. Serious discussions have taken place regarding the demerger, but the CEO cannot communicate any details until it receives board approval.

When asked regarding the sustainability of the margins, particularly in the API spiral and black pipe segments, the CEO explains that several factors have contributed to the improvement in EBITDA margins, **including the start of API exports to America, reduced shipping costs, and overall market realization improvement in the steel pipe segment.**The CEO believes these improvements are sustainable and expects a growth rate of 12-15% CAGR over the next 2-3 years. The company aims to eliminate working capital debt within the next 1.5 years. When asked about volume growth, the CEO states that the target for the next year is around 900,000 tons, representing a 13-13.5% growth rate. The focus is on improving EBITDA margins rather than solely increasing volumes. The CEO acknowledges the slower volume growth compared to competitors and attributes it to a decline in exports and API supply in India. However, the CEO expects improvements in these areas and anticipates better growth in export and API segments, while maintaining a minimum volume growth of 12-14% for the next year.

Lighting Division

The lighting division has not performed well in the past three years. however there is still growth potential in the market, with a significant share held by the unorganized sector. The company aims to capture a larger market share and improve its EBITDA margin by focusing on the LED segment, where market maturity and price stability are observed. There is a target of achieving a 10% EBITDA margin and ₹160 crores of EBITDA. The implementation of ATL (Above the Line) and BTL (Below the Line) strategies, along with efforts to expand the product portfolio, will contribute to this growth.

Through the Production Linked Incentive (PLI) scheme, the company plans to invest ₹25 crores over five years. These investments will drive innovation and contribute to the development of smart lighting solutions.

Regarding the vision for the lighting and electrical business, the CEO revises the target to ₹3,250 crores in sales within the next three years, with an EBITDA of ₹450 crores. The company plans to introduce a new product and strengthen its sales team to improve efficiency and expand into new markets. Despite the setbacks caused by the COVID-19 pandemic and industry cycles, the CEO remains optimistic about achieving the revised sales target by 2026.

Overall, the key opportunities lie in capturing market share from the unorganized sector, leveraging market maturity and price stability in the LED segment, and capitalizing on the PLI scheme for innovation. Steps taken to improve performance include implementing ATL and BTL strategies, expanding the product portfolio, investing in smart lighting solutions, and strengthening the sales team.