Suraj Products Limited was incorporated in the year 1991 as Champion Cement Industries Limited. Subsequently in the year 2000 company changed its name to Suraj Products Limited. Since 2002, the company has discontinued the cement manufacturing plant and diversified into manufacturing metallic products. The company owns and operates only one manufacturing plant in Sundargarh, Odisha. Suraj Products Limited is engaged in the production of sponge iron by direct reduction of iron ore, pig iron, ingots/billet, TMT bars and power generation.

Manufacturing Capability

At present, the company has an installed capacity to produce 36,000 mtpa (metric tonnes per annum) of sponge iron, 36,000 mtpa of pig iron, 72,600 mtpa of billets, 72,600 mtpa of TMT bars and 9 MW captive power generation capacity.

Major Changes in Company:

Suraj Products Ltd has transformed itself into a vertically integrated steel manufacturer from a merchant plant. It is characterised by the presence of a DR kiln (used to manufacture sponge iron), blast furnace (used to manufacture pig iron), induction furnace and continuous steel casting plant to produce billets using captive sponge iron and pig iron. The manufactured billets are then subjected to rolling to produce TMT bars of the desired profile.

Earlier, the company only used to manufacture pig iron and sponge iron but since 2018, the company has undertaken several capex which has resulted in a major turnaround for the company

In FY 2018 - The company commissioned its induction furnace (with a capacity of 25,000 tonnes per annum) in November 2017 for producing ingots, which is a relatively value-added product. The company has a captive power plant (CPP) of 6 megawatts (MW), out of which 3 MW is based on waste-heat-recovery (WHR) technology and the balance 3 MW is based on atmospheric fluidised bed combustion (AFBC) process. The cost structure of the steel melting operation, which is highly power intensive in nature, is positively impacted by the power available from the CPP at a cheap rate.

In FY2019 - SPL doubled its steel melting capacity by 25,000 TPA to 50,000 TPA with the installation of an induction furnace in December 2018. It has also installed another CPP of 3 MW capacity (AFBC), which will be utilised to generate power by using coal and dolochar (a by-product obtained from sponge iron production) as inputs. This is likely to positively impact the company’s turnover and cost structure.

In FY2020, the company added a rolling mill facility of 72,600 tonnes per annum for production of TMT bars and an induction furnace of 22,600 tonnes per annum.

Recently in 2022, the company added a beneficiation plant of 3,00,000 tonnes per annum capacity and further expansion of its captive power generation capacity by 3 MW.

What is beneficiation?

Iron ore is a mineral which is used after extraction and processing for the production of iron and steel. The main ores of iron usually contain Fe2O3 (70 % iron, hematite) or Fe3O4 (72 % iron. magnetite). Ores are normally associated with unwanted gangue material. Grade of iron ore is usually determined by the total Fe content in the ore. Run of mines ores after dry or wet sizing, if it contains normally greater than 62 % of Fe, are known as ‘natural ore’ or ‘direct shipping ore’ (DSO). These ores can be directly used in the production of iron and steel. All other ores need beneficiation and certain processing before they are used in the production of iron and steel.

Low-grade iron ores cannot be used as such for the production of iron and steel and need to be upgraded to reduce their gangue content and increase their Fe content. The process adopted to upgrade the Fe content of iron ore is known as iron ore beneficiation (IOB).

Benefit of beneficiation plant:

With the price differential between high-grade and low-grade iron ore remaining substantially high in the current environment of a domestic iron ore deficit for high-grade ore, the beneficiation plant, once operational will enable significant cost savings.

Effect of recent changes and expansion:

OPM has gone from single digits to double digits from FY2018 and consistently remained in double digits.

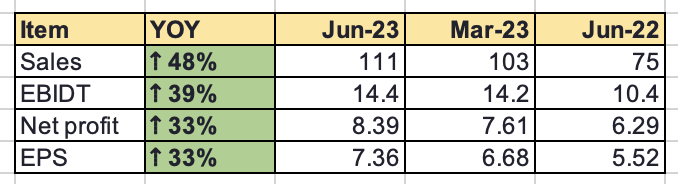

Recently, sales have shot up from 46 cr (Dec 2022) to 102 cr (MAR 2023).

Profit has not increased in the same proportion as OPM has dropped from 24% to 13%. Need to look at what happens in the future on the margin front.

Revenue Distribution (FY 2022 AR):

| Product | % of Revenue | Sale in cr. | Vol. (MT) | Realization per MT |

|---|---|---|---|---|

| TMT Bars | 44 | 103 | 22,420 | 45,944 |

| Sponge Iron | 23 | 54 | 17200 | 31,395 |

| Pig Iron | 23 | 53 | 14638 | 36,207 |

| MS Ingot/Billet | 8 | 20 | 5067 | 39,471 |

Past Financial Performance:

| Compounded Sales Growth | |

|---|---|

| 10 Years: | 14% |

| 5 Years: | 32% |

| 3 Years: | 34% |

| Compounded Profit Growth | |

|---|---|

| 10 Years: | 42% |

| 5 Years: | 49% |

| 3 Years: | 70% |

| Return on Equity | |

|---|---|

| 10 Years: | 18% |

| 5 Years: | 24% |

| 3 Years: | 28% |

Management:

Mr Y.K. Dalmia is 65 years of age and is a Chartered Accountant & Company Secretary. He Promoted the Company in 1992 & managing the same since then. His renumeration is 75 Lac. He holds 13% of the company. His wife Sunita Dalmia holds 6.78% of the company. She is also a director. The promoters hold 73.7% of the company via different companies and family members.

Investment Rationale:

- Vertically integrated nature of operations with the capacity to manufacture sponge iron, pig iron, billets and TMT bars – Billets are manufactured using captive sponge iron and pig iron. The manufactured billets are then subjected to rolling to produce TMT bars of the desired profile. In addition, a significant portion of the company’s total thermal coal requirements for manufacturing sponge iron is met from the linkages obtained through auctions, keeping the landed cost of coal competitive and enhancing raw material security.

- Company has gradually changed the product mix from sponge & pig iron to a rolling mill, which allows the company to sell more TMT bars and value-added products.

- Significant portion of the company’s total thermal coal requirements for manufacturing sponge iron is met from the linkages obtained through auctions, keeping the landed cost of coal competitive and enhancing raw material security.

- Suraj Products Ltd derive major strength from the very favourable location of its plant in terms of proximity to key raw material sources like ore iron, coal and magnesium. Odisha has high-quality iron ore deposits and it has the highest share in the production of iron ore in India.

- Presence of a captive power plant ensures the availability of power at a cheap rate. The steel melting operation is highly power intensive. However, energy generated through captive power plants at a cheap rate meets the major part of its overall power requirement, which positively impacts the cost structure.

- The company is expanding its captive power generation capacity from 6 MW to 9 MW. The additional power generation capacity will meet most of the incremental power demand arising out of the increased scale of operations. In coming quarters it will further strengthen the operating profile of the company and enable sizeable cost savings.

- The entire portion of the recent capex was funded through internal accruals, it is expected to give healthy cash generation in the near future.

- Fantastic past numbers across sales, profit and ROE. OPM have gone from single digits to double digits from FY2018. They are also paying dividends from the last two years.

- Debt peaked in 2020. It has gone consistently down from 87 cr. (FY2020) to 54 cr. (FY2023).

The central government’s call for Aatmanirbar Bharat has given a whole new dimension to the nation. Steel is a vital component of national development. The various sectors that are expected to contribute to the growing demand are infrastructure, smart cities, sagarmala projects, bridges, airports, industrial plants, buildings, automobiles, new roads and highways, railways, cargo terminals, National Ropeways Development Program for hilly areas and housing projects. etc all are expected to create steel demand, which will augur well for the steel industry.

Threats:

- Exposure to volatility in steel prices - The industry is characterised by its inherent cyclicality.

- High working capital intensity of operations can exert pressure on liquidity.

- Intense competitive nature of the secondary steel industry.

- Geographical risk: Single plant located in Odisha.

Market cap: 180cr.

P/E: 6.9

Price: 158