Equity share capital reduction by way of FV reduction in Supreme Petrochem and adjusted face value is credited as one time payment to the shareholders (Rs. 6 per equity share). I am experiencing this for the first time in any of my holdings and would like to know from boarders, if it is positive or negative for minority shareholders.

Ref: CF NCS/12/AGM_32/2021-2022 March 29, 2022 BSE Limited Phiroze Jeejeebhoy Towers 1 st Floor, Dalal Street Mumbai - 400 001 Script Code- 500405 National Stock Exchange of India Ltd Exchange Plaza, Bandra Kurla Complex Bandra East Mumbai _ 400 051 Scri~Code-SUPPETRO Dear Sir, Sub: Intimation of record date in relation to Scheme of Reduction of Equity Share Capital of Company under the provisions of section 66 of the Companies Act, 2013. Ref: Regulation 42 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 This is to inform you that the Record Date has been fixed at the close of business hours on Friday, 8th April, 2022 for the purpose of giving effect to the Scheme of Reduction of Equity Share Capital of the Company from Rs. 94,02,06,7101- (Rupees Ninety Four Crores Two Lakhs Six Thousand Seven Hundred Ten Only) to Rs. 37,60,82,684/- (Rupees Thirty Seven Crores Sixty Lakhs Eighty Two Thousand Six Hundred Eighty Four Only), by reducing the Face Value of the equity shares of the Company from existing Rs. 10/- (Ten) per share to Rs. 4/- (Four) per share, pursuant to the Order of the Hon'ble National Company Law Tribunal, Mumbai Bench, Mumbai, the certified copy whereof has been issued to the Company by NCLT on 29.03.2022. A synopsis of the Scheme of Reduction of Share Capital of the Company is enclosed herewith vide 'Annexure A' and the copy of said order of NCL T is also attached herewith vide 'Annexure B'. For complete details on the Scheme of Capital Reduction, please refer the documents available on the website of the Company under hUps:llwwW.supremepetrochem.com/reduction_share-capital.htm Kindly take the above on record and acknowledge receipt. Thanking you, Yours faithfully, For SUPREME PETROCHEM LTD D N MISHRA COMPANY SECRETARYI did some self study on my own query and came up with this article which explains the process/benefits in detail. Sharing this for the benefit of boarders if they have similar questions.

Supreme Petrochemicals (SPL) has shown remarkable performance in the last 2 years. Just analysed the probable reasons why… My summary thoughts and analysis… Feedback welcome. Please see attachment for details

Supreme Petro_Valuepickr.docx (108.3 KB)

Supreme Petrochem Ltd (SPL) is the India’s largest producer and exporter of polystyrene polymer (PS), compounds of styrenics etc.

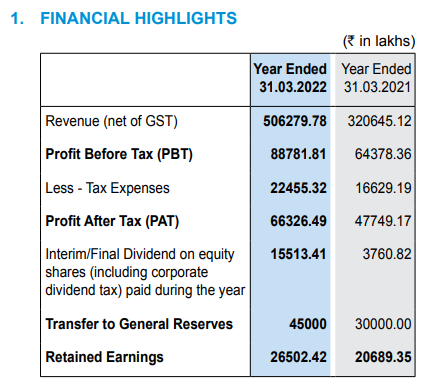

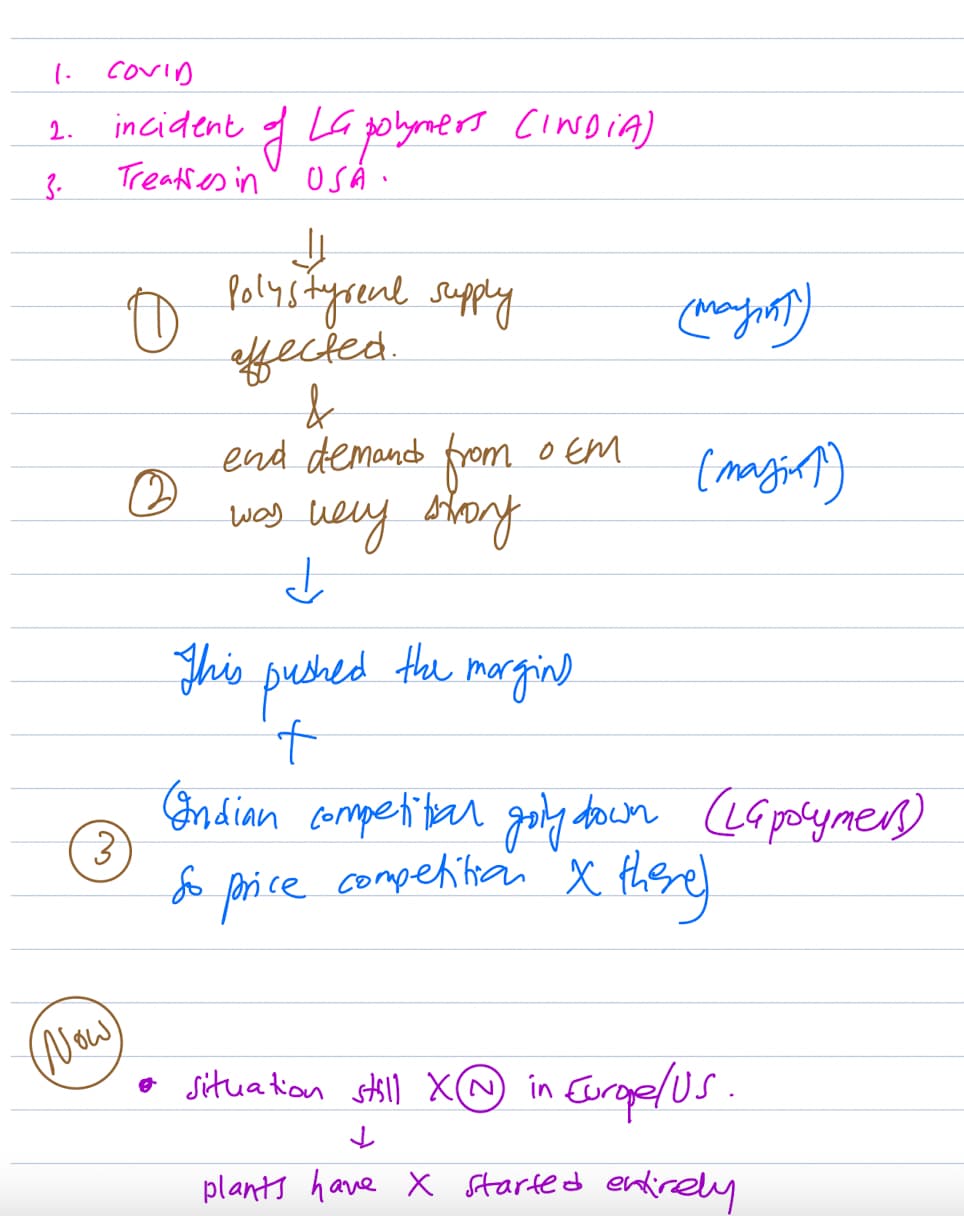

SPL has seen superlative earnings performance: Nearly 4 to 4.5x fold increase in net profits in FY21 – driven by favourable industry structure (closure of LG Polymers in May 2020), shortage of PS domestically, and strong international price delta (due to supply disruptions in global styrene and therefore polystyrene). Price delta is the spread between PS and raw material styrene etc.

Future earnings performance will be driven by volumes; global price delta could soften as supply disruptions in US and Europe ease. Further China, a key player with 25% of global capacity is also adding PS capacities

Environmental risks and risk of government ban on PS for single use packaging remains.

Supreme Petrochem annual report

*Inventory turn over has improved from 8.03 to 12.63 times (positive)

*ROCE declined from 71.89% to 67.46% (marginally down but still a good number)

*Net Debt free

Pollution Board clearance granted for the phase I expansion.

2022-12-31: Pollution Board Clearance

Some Positives:

-

Company has generated extraordinary profits in last two years. (Almost unsustainable at the current bandwidth)

-

Company is utilising almost equal amounts into expansion of PS and EPS capacities and starting a new adjacent vertical of manufacturing ABS.

-

This complete expansion should involve a capex of roughly 1200crs.

-

This is happening on a current fixed asset base of 350cr.

-

So we are looking at a 3x capacity with slight skew towards a better margin commodity business in 3-4 years from now.

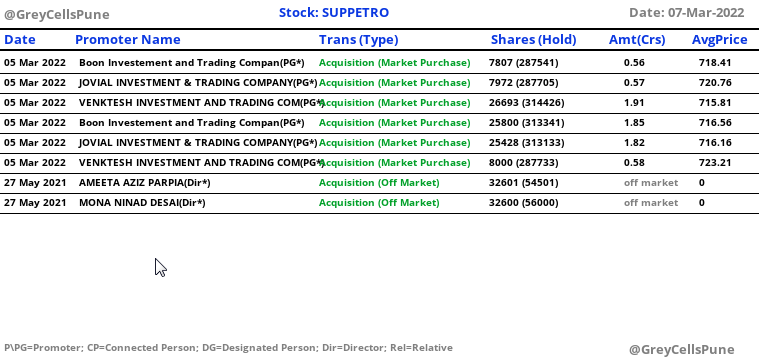

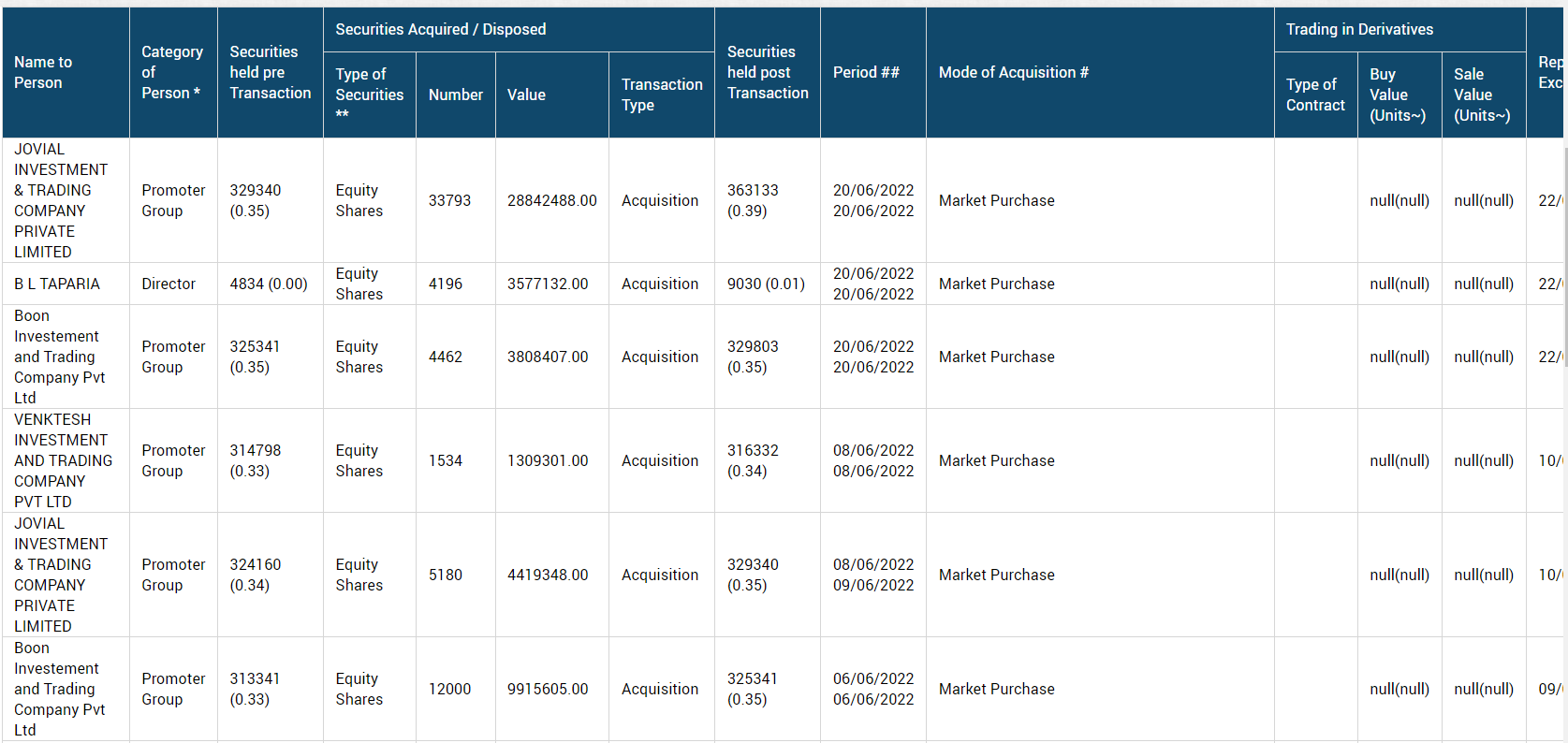

PS: It’s also interesting to note consistent promotor buying happening in this security since around the Russia-Ukraine War broke out

Risks:

- China is also developing more capacities and will have to see how this plays out.

- However, there could be some demand crunch happening in west due to high energy prices.

- Recessionary environments may lead to opposite of the current performance.

- Valuations are fair and not very cheap.

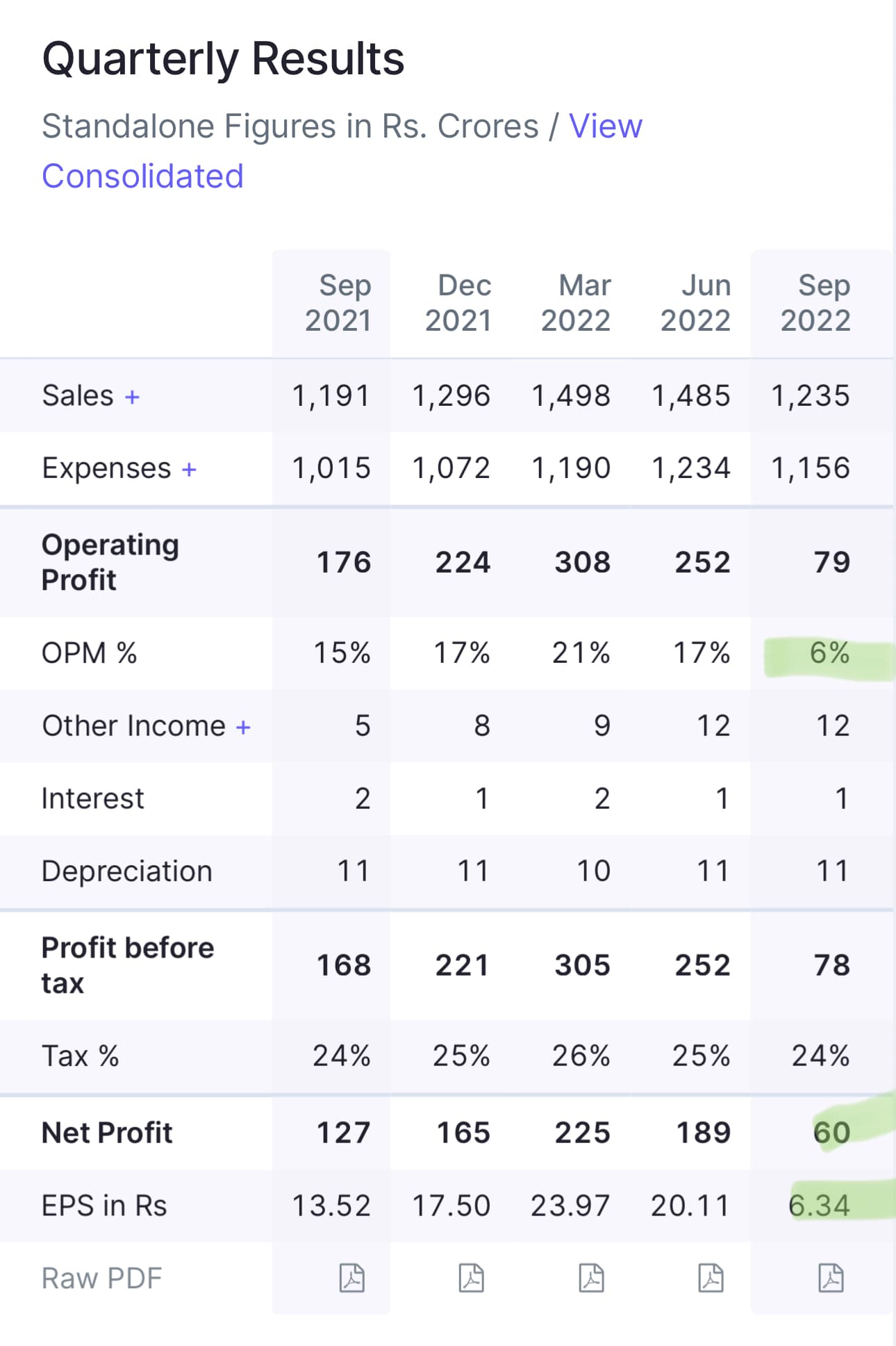

- there has been significant mean reversion in the OPM already in the last quarter.

[Discl: Invested]

Happy to hear thoughts from people tracking this scrip.

few questions!

-

how much of last two years performance is because of void created due to absence of LG ?!

-

can such high margins in such commodities products sustainable ?

-

is there scarcity of ABS currently ? will new capacities by supreme in ABS dent current ABS margin and make it very competitive, low margin resin?

dics: not invested but interested and observing

Concall: Q2FY24 (18th Dec 2023)

- The company’s basic raw material is SM (Styrene Monomer); this is converted to various dowstream profits like Polystyrene (PS), Expandable Polystyrene (EPS), Extruded Polystyrene (XPS). The company made enormous profits in 2021-22 (see the image from screener below) and is now utilising those profits to venture into developing a new product: mass ABS. The company has tied up with an italian company for the same.

The capex details are mentioned below.

To set the context as why the company enjoyed such profits in FY21-22 which is not sustainable historically?

- Current Styrene monomer prices: ~1050$

- There used to be 3 players in this space and now with LG polymers shut there are only two key players.

- The demand for LG Polymers is being substituted by Supreme, Styrenix and imports.

- Capex Plan:

- Making mass ABS plant

- Currently ABS is imported in the range of 130-140,000 tons with total mkt being of 275,000 tons

- Have further land for brownfield expansion if needed

- this is a different way to make ABS than the emulsion ABS; the former is a continouous process while the latter is a batch process. The energy costs are roughly 2x higher for the latter

- This imlies that Supreme will become a cost efficient player in ABS once ready

- 1200 Cr: Completion by March 2026

- 500cr: Already incurred

- Balance 700 cr will be spent between now and march 26

- Once complete this capex at capacity utlisation of 70-80% should lead to additional revenues of 3000cr

- Making mass ABS plant

- On XPS:

- <2% of revenue at present

- No competition as only player

- Highly climate friendly as helps in thermal insulation of buildings hence reduces energy requirements (both hot and cold) and thereby decreases emissions

- Govt and corporates are using it but individuals arent

- Eg in CPWD, possibly this was used in the new parliament building too.

- If you wish to understand this product: InsuBOARD

- On competition expanding

- No worries as enough demand as we still import.

- It ll eventually be import substitute

Near term Forecasts

- PS:

- Expect muted growth as appliance mkt has beem slow

- Expect mas 4-5%

- EPS:

- Expect 8% growth

- XPS:

- Again 8-10%

- Capacity

- PS: 300000 tons (Styrenix ~ 75000 tons); total market is around 315thousand tons

- EPS: 1,10,000 tons

- Use: packaging, insulation food packaging, cold storage, construction

Impressions:

Next 1-2 years appear to be muted and will correspond to global deltas between SM and PS.

The next leg of growth will appear after end of FY25 depending on ramping up of new capacities and growth in white goods/appliance sector. Historically, it has been futile to predict or forecast growth in this commodity company however with this kind of management, company seems to be poised to do well in the long term. The company used to bottom out at p/b of 2 however as the company is becoming stronger and relatively less cyclical the base may increase going ahead.

[Disclosure: Invested]

VAP Will Contribute 35-40% To FY25 Volumes, Q1 Exports Growth To Be Better Vs Q4FY24

Click to view video Interview

25/04/24 : CNBC; Mr. Rakesh Nayyar

-

RM prices going up leads to increase in topline eventually passing on to customer however if RM prices spikes a lot and thereby leading to increase in end product prices could lead to dampening of demand later on

-

Volumes: Q4 is usually domestic dominated as the white goods manufacturers start stocking up for summer season. Q3 is lean but our exports were higher. Exports overall have been +82% this year.

-

For FY25 we see better exports growth

-

3,25000 Tonnes in FY24 but hope that we ll cross 3.5L tonnes FY25

-

Mass abs: should add 900-1000cr to topline with better margin, with asset turns of 2. Hope by FY27 we should be optimally capacity utilisied.

-

Master batches: This capacity wiukd be online by end of this FY25. Demand coming from EV battery, piping, films, appliances sector

-

Hope volume growth of 8-10% this coming year.

Q4 FY25, wld also see first batch of Mass ABS, which as higher margin the traditional products.

So overall with increased prices and increased Volume , overall sales can be up in double digits and with Exports and Mass ABS kicking in, i assume Profits can also go up.

Looks like as per latest announcement, Q1 FY26 is the tmie when they will look at first batch of ABS.