BACKGROUND

Real estate companies in India are very promoter driven and the evolution of the company mirrors the promoter more often than not. Sunteck has had an interesting evolution since they started in early 2000s. Promoter started off by taking a commercial property in BKC for lease and operating as a business centre. Later in 2006 ventured into real estate development, bought a land parcel in BKC for building residences in the uber luxury segment for corporate executives and business clientele. Ticket sizes are 20-30+ crores. The current occupants include Uday Kotak, Gautam Adani, etc. Exploited the arbitrage in pricing between BKC commercial and residential. Residential was trading at 1/3rd the cost per sqft of commercial. Land purchased at ~10k per sqft. And the apartments are being sold now at ~90k per sqft.

This was the company’s only growth engine until they acquired a second piece of land in Oshiwara District Centre, Goregaon. 5-10 min drive from Lokhandwala. 5-10 min drive from Oberoi Garden City, NESCO etc. They’ve been constructing mid-income houses here with ticket sizes of 1-3.5 crores. This has been planned and being developed in multiple phases. This also includes Avenue 5 which is their planned commercial project for retail and commercial use with potential annual rental income of 400+ crores. The third growth engine they’ve now built through the JDA model is in Naigaon, near Vasai under a ~25% share revenue sharing arrangement. They’ve had good success in two phases that have been launched with strong sales velocity ~4k apartments sold out of 4.4k total units.

MAIN PRODUCTS/SEGMENTS

The company operates in the MMR region where typically land is the significant chunk of costs. ~75-80%. The company operates 4 different brands each catered to a different segment of customers.

Signature - Uber Luxury - Op margins ~45-50%

Signia - Luxury - Op margins ~40-45%

City - Mid Income - 30-35%

World - Affordable/Aspirational - 20-25% (although Naigaon seems to have been close to 30%)

CURRENT MARKET/INDUSTRY TRENDS

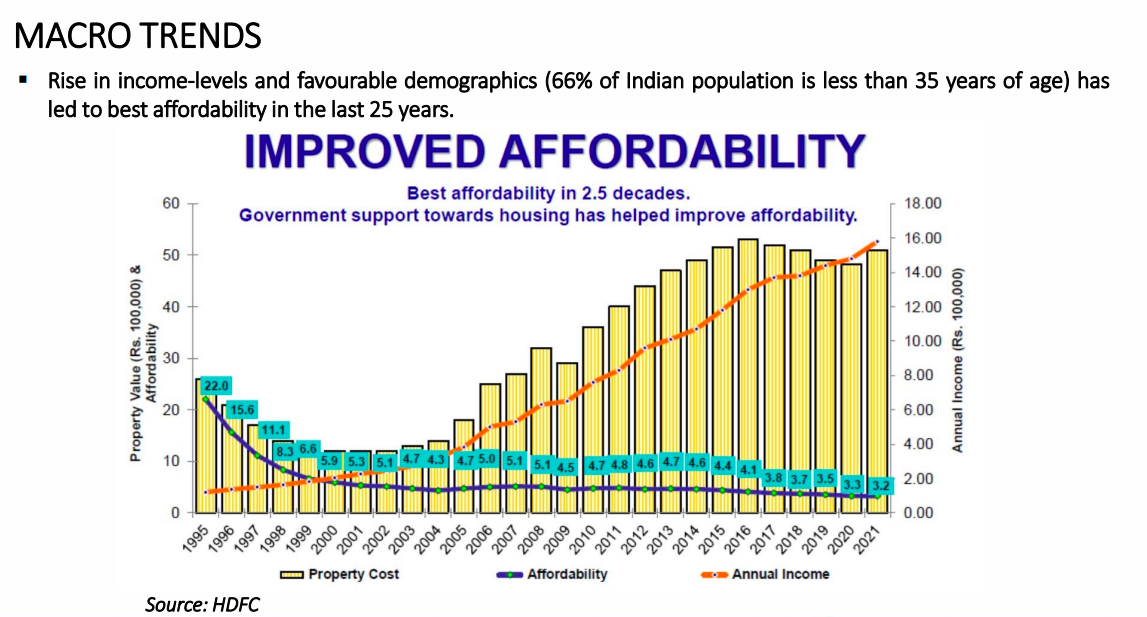

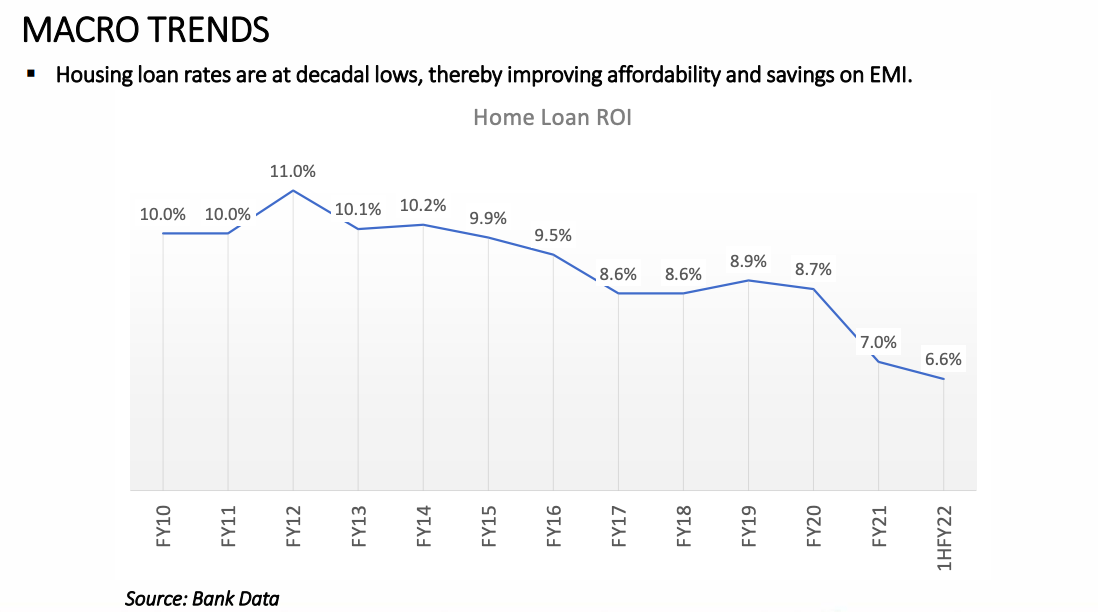

The real estate sector has had a difficult decade in the past and there are indications of some revival driven by end use consumption and better affordability levels. Mumbai, in particular, has seen better demand revival. Affordability is at good levels due to stagnant price levels and rising incomes and low interest rates helping demand for housing after a long lull.

BULLISH VIEWPOINTS

• The company has made a string of acquisitions for development under the JDA model recently in Vasai, Vasind, Borivali, Kalyan, Vashi to act as additional growth engines to BKC, ODC, Naigaon projects.

Vasai - Mid Income housing - margins close to City brand. Location overlooking the beach and premium properties. Vasind and Kalyan - Aspirational segment project - close to World brand margins. Borivali - Signia project - Luxury project. Previously SK resorts. 40-45% margins. Vashi - holiday homes and second homes. Plotted developments along pen-khoppoli. Scarce non agricultural land. Revenue share ~80%. The company has further acquisitions under pipeline under the JDA route for FY22.

• Pre-Sales Mix

- Current pre-sales mix of ~1k crores being driven only by two projects - ODC and Naigaon. Last 1 year, BKC projects have not had much contribution, which used to be about 250 crores. BKC, Naigaon, ODC could contribute about 1250 crores of annual pre-sales mix for the coming 5 years.

- Addition 1 - Vasai 4.5 mn sqft project - to be developed over 5-6 phases. 1 phase will be 7-8 lakh sq ft at 7-8000 Rs. per sqft. Sunteck potential share is about 350 crores annual pre sales.

- Addition 2 - Borivali W - phased over 5 years. Sunteck potential share is about 200 crores annual pre sales per year.

- Addition 3 - Kalyan - phased over 5 years. Sunteck potential share is about 500 crores annual pre sales per year.

- Addition 4 - Vasind and Vashi - Sunteck potential share is about 200 crores annual pre sales per year.

With further launches and deals, the management commentary is very strong for growth in the coming few years with 700 crs PAT annually albeit on a lumpy basis.

• JDA

- A key asset to the company is the reputation they have built among landowners with the JDA route. The JDA route stands beneficial to the company as they are able to enter projects with minimal costs upfront and minimise their entry costs and maximise the exit opportunity in a region like MMR where land costs end up being a significant chunk of project cost.

- Oberoi and Godrej are still in the asset heavy land bank model. Lodha has made some announcements to move into the JDA model. The success of Sunteck Naigaon acts as a great pull for other landlords. From just the first two launched phases (25-30% of total area) of Naigaon project, the landlord will get 400 crores of cash flow as opposed to having to sell the whole land parcel outright for 700-800 crores.

- Accessibility: Sunteck moves faster and being focussed only on MMR, and with direct promoter involvement with landowners, they are able to focus better and get good terms.

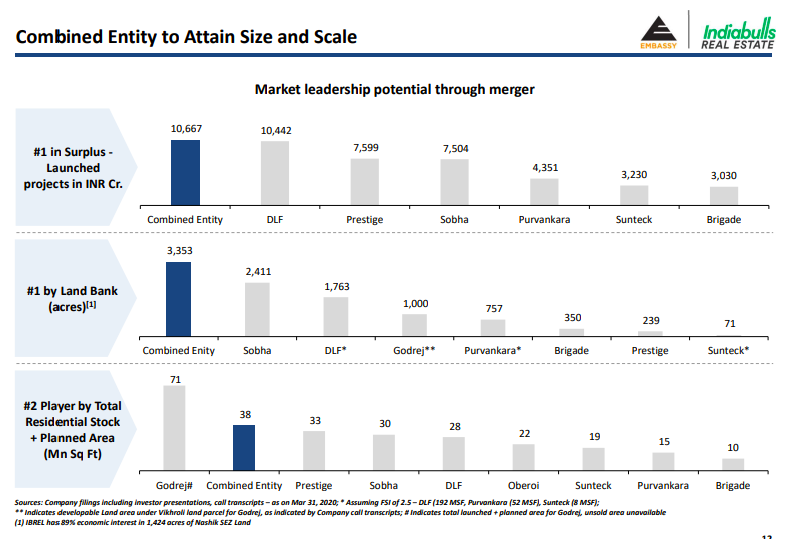

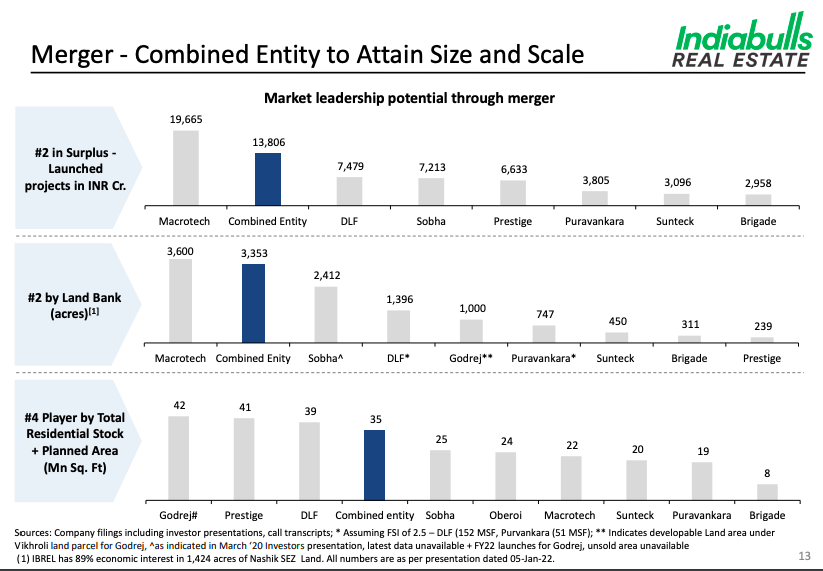

- They have been able to showcase the money to the landowner has helped a great amount in attracting these deals. The IBREAL presentation from Aug 2020 to Jan 2022 shows how active Sunteck has been in doing land deals over the last 2 years with a sharp move from 71 acres to 450 acres. While they are at 20 mnsqft as of Jan 2022, the acquisitions at Vasai, Vasind, Borivali W, Kalyan, Pen-Khoppoli will add another 23 mnsqft of development potential.

Aug 2020

Jan 2022

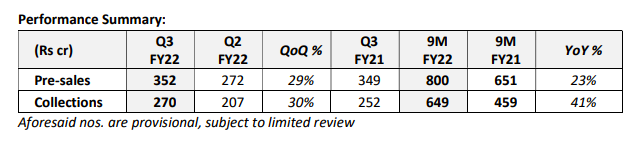

• Collection Efficiency:

- The company has been tracking good collection efficiency metrics. 81% in 9MFY22 vs 70% in 9MFY21.

INTERESTING VIEWPOINTS

• Demand and Supply in the micro markets of MMR:

- There has been good absorption in the region of ODC Goregaon and Naigaon. BKC resi has been slow for the company due to the ticket size involved and would take time to clear the inventory.

- Vasai has the lowest inventory in the entire MMR. 12 months inventory in Vasai as opposed to 24 months in MMR. Vasai has no organised developer presently. And the land location is right on the beach to be built as sea facing property.

- Borivali W - only one other developer with a luxury project. Wadhwa Group Club Aquaria. Total absorption in this micro market last year was 1500 crores. The company will be bringing 1.2 years of last year sales with this project. And will be further launching it only in phases. It’s one of the more robust suburbs in MMR.

- Kalyan - very well chosen project in the eastern suburbs which could see good absorption.

• Commercial Side:

- In ODC Goregaon, the company is looking at annuity income. In ODC, they have used 2.5 msqft. Left with another 4.5 msqft. Out of 4.5 msqft, 3 msqft is commercial. MMRDA gives the flexibility to use 1.5 msqft out of the 3 msqft as residential. So if the commercial market doesn’t revive they have the flexibility to use it as residential. But if they see greenshots in the commercial segment, they have the option to partner with a PE fund and develop the entire 3 mn sqft for commercial without destroying the balance sheet.

• In House Construction: All projects are constructed in-house by Sunteck. Only the labour component is outsourced. For all projects across all the product segments.

BEARISH VIEWPOINTS/RISKS

• The company has ~1800 crores of inventory left from BKC projects. Out of a total of 220 units, 180 units have been sold and the balance is expected to be liquidated only over the next 3-4 years. The super luxury segment has seen low absorption in BKC with BKC projects contributing very minimal amount to sales in current year.

• There is major dependency on Naigaon and ODC projects right now. ODC handover has been delayed further by a few months as the company is now constructing additional floors with additional FSI they have obtained. Possible delays in new launches could extend this dependency further.

• A lot hinges on the company’s ability to choose the right projects at the right locations with the right customer segment and product. The Naigaon success has led to good credibility among landowners for Sunteck, mismatched projects which sees a very slow response from customers could spoil that sentiment.

• Geographic Concentration: The company is 100% fully focussed in MMR region. Any dampening in the revival of MMR real estate demand could spoil the party for the company.

• RE sector is very micro market driven and the individual projects need to be tracked for the demand and supply in that particular micro market and the competition from other credible branded developers.

• The narrative around consolidation in the RE sector, post RERA and the slump over the past few years could very well be reversed with the tide turning around for the sector. Considering MMR is a redevelopment driven market, it remains to be seen how transient or structural the consolidation of players narrative will be.

BARRIERS TO ENTRY

• The company operates in an industry with very low barriers to entry. Although RERA has made it difficult for fly by night operators and large landowners developing the land themselves due to requirements of approvals and certain level of progress before the project can be marketed to customers increasing the upfront investment required, the barriers to entry are low with many South based developers entering the lucrative MMR market as well.

VALUATION MODEL

The company trades roughly at a FY22 EV/Pre-Sales of 5 times which seems largely inline with the multiples of peers.

CORPORATE GOVERNANCE SCAN

- The promoter family holds 67% stake in the company and the daughter of the promoter is also involved in the operations of the company now.

- Corporate governance history has been relatively clean. No known political linkages.

- There has been some capital allocation issues in the past with the Dubai and Jaipur projects. Issues in Goa commercial project due to approvals.

- Company feedback on product quality and delivery timelines have largely been positive.

- The senior leadership team has been together now for more than a decade without significant churn.

DISCLOSURE: Invested