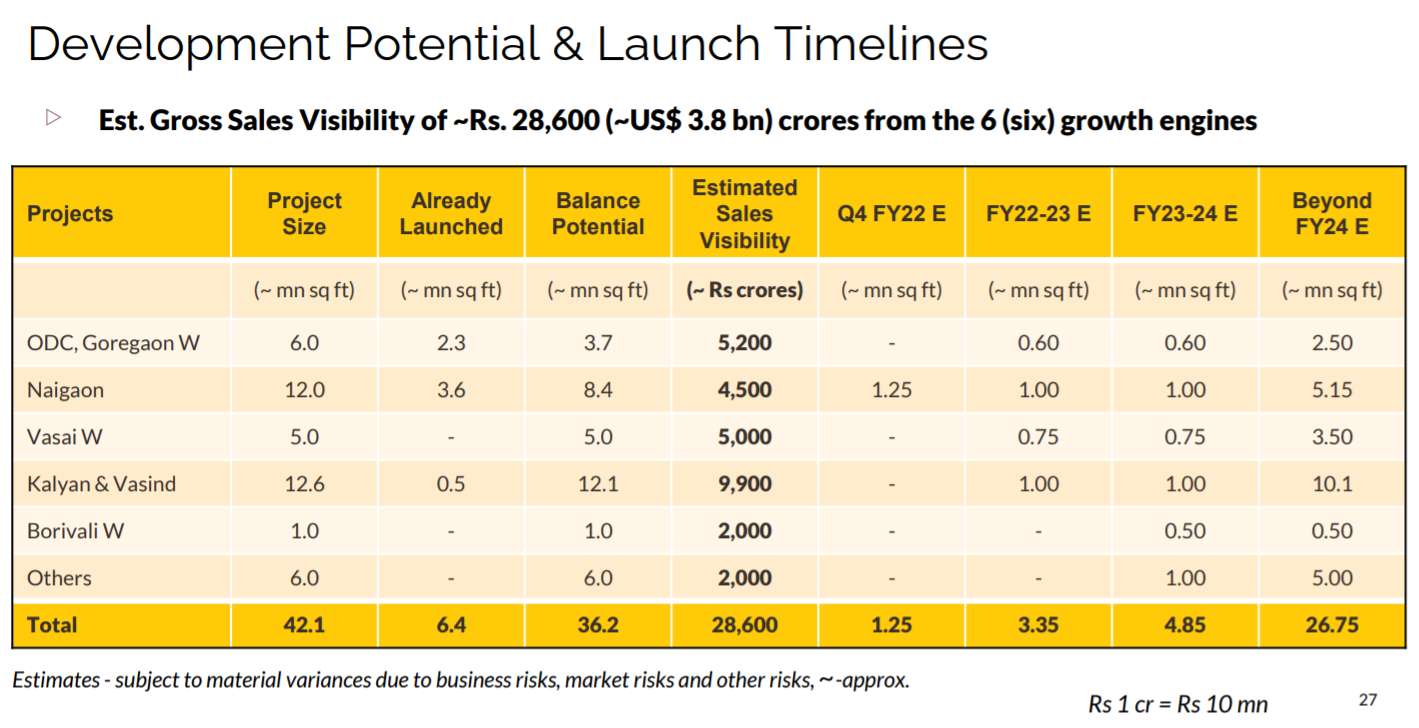

Monetization of upcoming project portfolio to generate ~US$ 3.8 bn (~Rs 28,600 cr) of est. GDV in coming 7-8+ years

Acquired ~23 mn sq ft in 20-21

~36 mn sq ft of projects acquired since 2018

Key Financials

▷ In Q3 FY22, Revenue from operations stood at Rs 128 cr (Rs 1,281 mn) and Rs 357 cr (Rs 3,572 mn) for 9MFY22

▷ EBITDA for the quarter stood at Rs 35 cr (Rs 346 mn) and Rs 92 cr (Rs 917 mn) for 9MFY22

▷ EBITDA margin stood at 27% and 26% for Q3 FY22 and 9M FY22 respectively

Thank you sharing this. My view was that this company had clients like Adani, Uday Kotak, DMART in the past, and those projects got delivered. So, that’s why can’t conclude if it’s CG issue or not, simply based on this video.

Would like to read views of other participants.

Decent operational performance. Still below Q4 22 peaks but improvement YoY and QoQ.

Supply increase in MMR is clearly visible for anyone in the city. I get 3-4 calls a day from different developers trying to sell completed and upcoming projects. Can the Sunteck brand stand differentiated, or is the demand cycle strong enough to absorb the surplus? One of the two must be true for Sunteck to continue to do well. Seems fairly priced at CMP.

Disclosure: Invested from lower levels. Keep trading a bit around volatility.

The latest operational updates show that they’ve crossed Q4FY22 in pre-sales in Q4 FY23. The lack of activity on this thread at a time when the company has posted it’s best ever quarter, when the stock is trading at 1.5 times book which is the trough of the last three years, and when the entire sector is moving on interest rate cut expectations, tells me that the risk-reward is good.

Disclosure: Invested from near 200 levels and adding some more. About 5% of the portfolio at CMP.

The Sunteck Westworld project in Naigaon has led to bad publicity. The residents are not happy with water supplies and construction quality. This might lead to cascading affect on upcoming launches.

Would this lead to an overhang on company?

PS: Sunteck has great business model (JV with landlords), 0.1 debt/equity and 20% cagr pre-sales and collection growth.

What are your views on the current numbers,it has fallen quite a bit but i think for this stock we need to compare YoY rather than QoQ and what is the meaning of pre sales and why are they so elevated compared to topline sales?

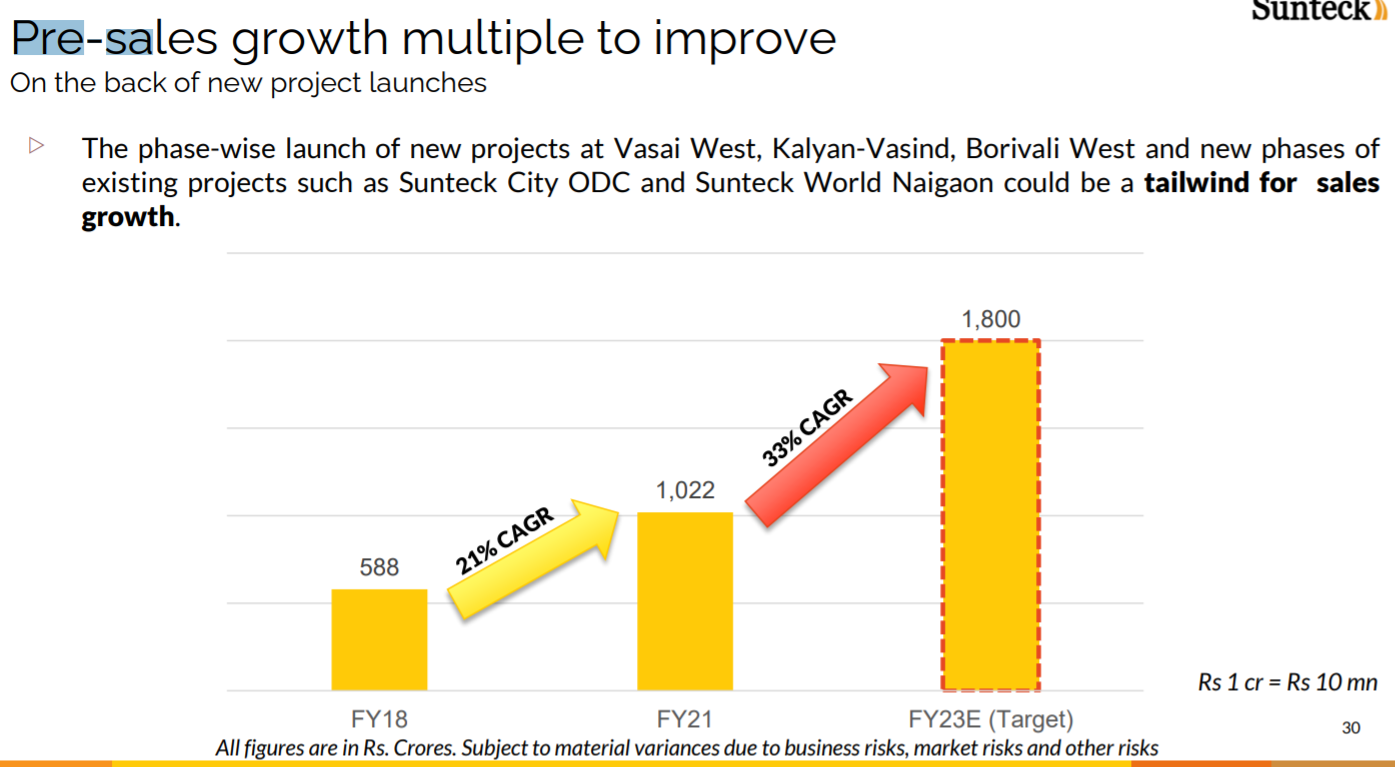

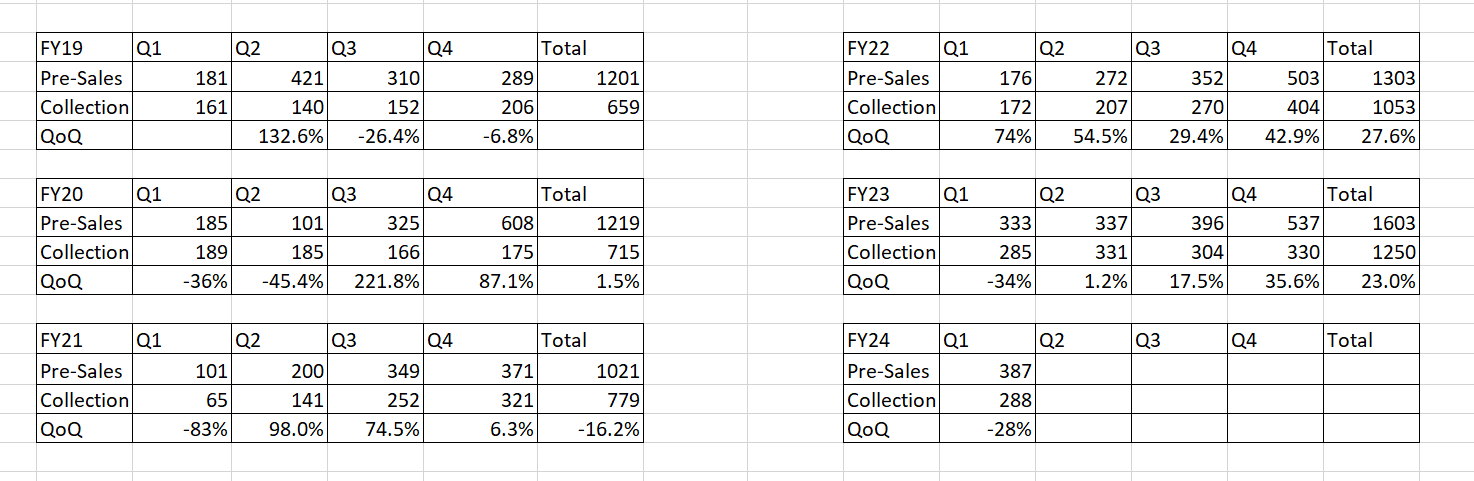

I have compiled Pre-sales & Collection Data since Fy19. The Q1 is mostly weak compared to Q4. As of now Pre-sales are on Good track. They launched Vasai Project last Quarter & will Launch Kalyan Project this Year. If they succeed in launching the Kalyan project this year then Pre-sales numbers will jump higher. If there is any weakness in Pre-sales & delay in the new project Launch then I might exit and look for a better opportunity.

I guess, they lost the sales in Naigon by 70-80 Cr due to ongoing water supply issues in Q1-24.

By sunteck standard current quarter is weak (as they launched 2 news projects-Vasai , Mira Road compared to last year) and other RE companies posting all time high Quarterly pre-sale numbers and those stocks touching 52 week / all time highs. Less hope on current quarter as well due to seasonality…

Possible triggers

1.Sale of Commercial projects(Suteck Crest and Ikon) as they are ready to occupy.

2.Succesful Launching of Kalyan

3.Increasing the monetization rate of BKC projects

4.Addressing issues in Naigon as it might be hitting the sales velocity

5.Increasing the number of live projects (Borivali , Malabar Hill, Pen Khopoli)

As per the latest concall (page 6 & 7), management has provided the following info:

Expected Cash from total unsold inventory (already built) = 1600cr

Expected Cas from already launched projects (Recivables 2100cr - Outflow to complete 1100cr) = 1000cr

Expected Cash flow from upcoming projects (GDV (sale value) = 30,300cr - Outflow to complete 9000cr) = 21,000cr

Apart from the above, 2 commercial projects have a sale value of 1000cr ( 500cr + 500cr - one estimate given by management the other one my assumption)

All of this to be monetized in next 7-8 years.

So you pay 5200cr for a biz today which in 7-8 yrs will get you ~24,600cr (pre-tax) !!

And here is the real killer - GDV of 30,000cr is based on today’s market price. Assuming a very conservative 20% increase in market price, 24,600cr become 30,000cr. And that too ignores any future value creation project acquisitions which will likely take place enhancing the 30,000cr future cash flow value even further.

There might be reasons for lower valuation -

Compare it with Phoenix mills, Oberoi - Sunteck has very low ROE, ROCE, OPM, etc.

Steady cashflow (annuity - rental) and balanced growth plan are real positive points for Phoenix mills and Oberoi - If you believe in retail /consumption growth story in India…these companies can do better!

You can’t value real estate companies on earnings related metrics, especially if they follow project completion method. ROE, ROCE will never reflect the true picture of these businesses. Look at cash flows, present and future.

Indeed, Sunteck follows the project completion method - management mentions that in this quarter’s earnings concall. Expect big jump in reported profits going forward.

You will see ROCE increasing year on year and surpassing 25% in coming 2-3 years (Its obvious from the above cash flow guidance that the management has provided)

Project launches over next 7-8 years doesn’t mean completion.so, it could take another 2-3 years more to realize the entire cash flows.

7-8yrs from now could be end of real estate cycle and there could be project delays as well

while its difficult to calculate today’s NPV as the timing of cash flows is not known. Assuming 25% tax rate, a discount rate of even 15% (should be higher for real estate), and 24,000cr is realized equally in yr 4 & 8 , todays NPV is about 8000cr.

7-8 is the complete monetization timeline not the project launch timeline

A rising cycle for the next 7 yrs will benefit players who have the projects/JDA/landbank in place. Its also good that beyond 7yrs cycle will turn down and smart developers can deploy accumulated cash in new project acquisition for future upturn in cycle.

You assume zero capital appreciation over the next 7 yrs while the cycle is turning up…a very very conservative 25% appreciation in 7yrs in price can be easily expected (although we know the price appreciation can be a lot higher than that)…in which case future cash flows are 30,000cr

You ignore any future project acquisitions and as a consequence you ascribe zero terminal value to the company. Past track record of 20 yrs shows management has repeatedly recycled and redeployed cash flows at high IRR( much greater than 18%-20%)

Even if we ignore point no.4 above ( which is wrong as it implies that the company shuts down after 8 yrs becoz it can no longer generate new business at desired IRRs of >18% as it has done in the past 2 decades):

At current MCap of 6150cr,

With 25% tax rate,

Pre-tax cash flow of 30,000cr at same time interval as you assume above,

IRR works out to be ~26%…

Or in other words, if you use a discount rate of ~26%, you would get the NPV equal to today’s Mcap of 6,150…

26% return p.a. for next 8 yrs !!! ( with super pessimistic assumption of zero terminal value !!!)

Given the above, I feel Sunteck is a great bargain…

As per the latest concall, a strong pipeline of deals under consideration for business development. We can expect announcements about some deals in the coming quarters Considering the past track record of Mr Kamal Khaitan MD , we can expect the business growth to continue in future years adding to the GDV numbers. Presently the management is concentrating in MMR market only. They may think of expanding into other cities. I fully agree with you that Sunteck is a great bargain.