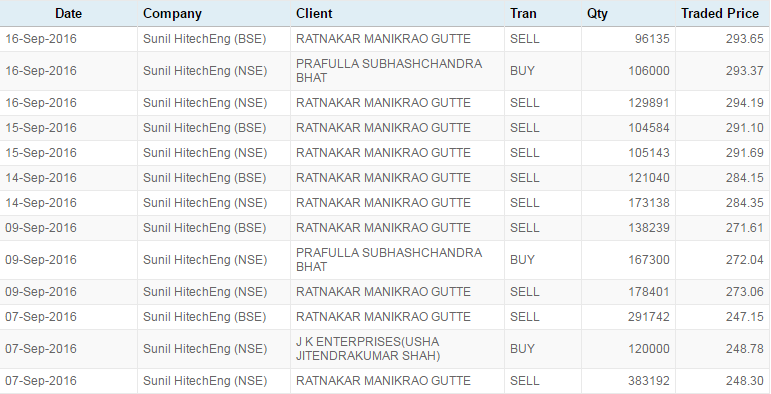

Sunil Hitech Engineers ( SHEL) is a Maharashtra based company .Started by Mr Ratnakar Gutte ,a high school dropout with just Rs 2,000 as capital ,Sunil Hitech now turned as a Rs.1500 Cr turnover company . Now company is professionally managed with the help of his two sons -one a mechanical engineer and the other an MBA.

SHEL specializing in fabrication, erection and commissioning ofpower plants. In addition to power plants ,company executingLump sum turnkey (LSTK) contracts of Transmission & distribution projects, Steel Plants, Sugar Industries, Process & Piping Industries, irrigation projects…etc .Company is one of the few qualified contractors for BOP worksup to 660 MW .Comanyâs marquee clients includes NTPC,BHEL,Alstom Energy Corporation,L &T,JSW Steel,JSW Energy ,BALCO …etc and various state electricity boards.At the end of FY 2013 SHELâs order book position was Rs.2300 Cr .

Furthermore ,Company has entered into the construction & development of luxury homes/flats equipped with all modern amenities and facilities namely ‘‘Water Green Project’’ at Nagpur, Maharashtra and’‘Green Acres Project’’ at GOA. Also due to rapid growth and upcoming opportunities in the construction & development business of roads / highways/bridges/flyover, Company is eyeing to explore opportunities in this sector.

In FY 2013–14 ,on a consolidated basis ,company reported a top line of rs.1598 Cr , a net profit of Rs.30 Cr and an EPS of Rs.18 . During the latest two years promoters hiked their stake from 49 % to 58 % by subscribing shares on preferential basis .In addition to this ,they also subscribed warrants which will be converted into equity shares within 18 months. On full conversion of these warrants promoters stake will again rise to 66 % .Pumping of this additional funds by promoters will help the company to reduce its dependency on debt and some comfort on working capital side.

Last 5 years performance : Itssales have been growing at 19% per annum over the last 5 years. While the Net profits had recorded marginal growth , it has more to do with the overall sectoral performance.

**Current Year Performance:**Current Year Performance has been extremely strong . During the first quarter , it has growth its sales by 28% and Net Profits by 50%. EBIT% had grown by 32% and EPS by 33%.

Cash Flows : What has interested me is that the companyâs strong Cash Flows. The company has generated positive cash flow in 4 out of 5 years. Its enterprise value is only 5.4 times the Free Cash Flow during the year 2013-14.

Reasons for Recommendation : Regular increase in Promoter Stakes year after year, Strong Cash Flows, Low Enterprise Value to Free Cash Flows(5.4 times 2013-14 FCF ), 4 fold improvement in Cash Flows from operating Activities during the last one year and 50% growth in PAT during 1st Quarter.

Disclosure : Not yet invested but will be investing.

Concern Areas : While going through 2013-14 Annual Report , I saw the following Auditors Queries and Management Replies . The company hasn’t added subsidiaries Accounts Statements to AR since they were not yet prepared. I do not think this is the right practise though they account for only 10% of sale and 15% of Net Profits… I am copying them verbatim so that we can get group’s interpretation of these Queries.

Auditors Query:-

In case of PBSPL-SHEL-JV, one of the joint venture of the Company, the audited financial statements are not available. The proportionate share of each of the assets, liabilities, income or expenses of the said Joint Venture has not been incorporated in the consolidated financial statements.

Management Reply:-

Sunil Hitech Engineers Limited (the Parent Company) has entered into a Joint Venture with Phenix Building Solutions Private Limited named as PBSPL-SHEL-JV, a jointly controlled entity where in the Parent company holds 49% interest. The accounts of the said JV are under preparation and therefore, the proportionate share of each of assets, liabilities, income and expenses of the said JV has not been

incorporated in the Consolidated Financial Statements.

Auditors Query:-

In case of MSMC Adkoli Natural Resources Limited, a joint venture of Sunil Hitech Energy Private Limited, one of the subsidiaries of the Company, the audited financial statements are not available. The

proportionate share of each of the assets, liabilities, income or expenses of the said Joint Venture has not been incorporated in the consolidated financial statements.

Management Reply:-

MSMC Adkoli Natural Resources Limited is a JV company of Sunil Hitech Energy Private Limited, one of the subsidiary of the parent company (As per Accounting Standard -21 issued by the Institute of Chartered Accountants of India, New Delhi) and Maharashtra State Mining Corporation Limited. The accounts of the said JV Company are under preparation and therefore, the proportionate share of each of assets, liabilities, income and expenses of the said JV has not been incorporated in the Consolidated Financial Statements.